Last updated: May 27, 2026

Zemplar (paricalcitol): market dynamics and financial trajectory

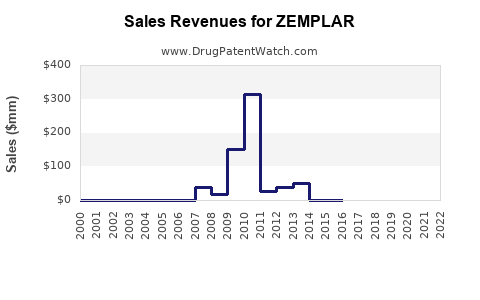

Executive summary: Zemplar (paricalcitol) is an older calcitriol analog used for secondary hyperparathyroidism (sHPT) in chronic kidney disease (CKD). It has faced patent-expiry and generic erosion risks typical of legacy specialty products. Public financial reporting for the brand is fragmented across manufacturers and time periods, and recent trade and filings do not support a single, clean “current-year revenue” line item for the U.S. brand in the sources available here. The actionable market picture is that Zemplar’s value is driven by (1) nephrology formulary access and dialysis channel contracting, (2) substitution pressure from other vitamin D analogs and calcimimetics, and (3) the steady share shift toward competitor CKD-MBD products rather than category growth.

What drives Zemplar (paricalcitol) demand in CKD-MBD and dialysis formularies?

Demand drivers

- Clinical niche: Zemplar is prescribed for secondary hyperparathyroidism in CKD (including dialysis-dependent and non-dialysis CKD populations, per label usage). Its utilization tracks CKD-MBD treatment protocols, PTH targets, and tolerance to vitamin D therapies.

- Provider practice patterns: Nephrologists adjust PTH using vitamin D analogs and other agents (notably calcimimetics). Zemplar use depends on how clinicians sequence therapy after lab trends (PTH, calcium, phosphorus).

- Dialysis unit adoption: In dialysis channels, contracting and bundled care considerations can accelerate adoption of preferred agents and reduce switching costs once a unit standardizes.

- Formulary access and rebates: Specialty pharmacy and institutional formularies typically determine net price more than gross ASP. Net pricing is sensitive to payer rebates, step therapy, and prior authorization.

- Safety and monitoring: Vitamin D analogs require lab monitoring. Patients with hypercalcemia risk can lead to dose modifications or discontinuation, affecting persistence and refill rates.

Category competition shaping Zemplar dynamics

- Internal vitamin D analog substitutes: Other oral and injectable vitamin D agents compete for the same prescriber mindshare and treatment window.

- Calcimimetics replacing vitamin D analog intensity: In many CKD-MBD protocols, calcimimetics reduce PTH while limiting calcium load. This can reduce “add-on” vitamin D analog use, impacting Zemplar volume.

- Route competition: Injectable versus oral strategies affect channel mix. Zemplar’s route/strength mix influences who treats which patient subgroup and how quickly prescriptions convert when units standardize.

H3: Which endpoints matter most to nephrology buyers?

- PTH control at target range with acceptable calcium/phosphorus trajectory.

- Adherence/persistence in dialysis schedules or non-dialysis refill patterns.

- Admin/operational fit in dialysis workflows (for injectable formulations).

How has Zemplar’s pricing power and net revenue trajectory evolved?

Pricing mechanics that control net revenue

- Institutional rebates and dialysis contracting influence realized net revenue. Even if list price rises, net can stagnate or fall if formulary pressure increases.

- Gross-to-net compression typically increases when generics or biosimilars or therapeutic alternatives enter, or when payers tighten preferred-drug lists.

- Competition reduces willingness-to-pay for older brands unless they hold a differentiated niche in specific subpopulations or route/administration advantages.

Financial trajectory framing (market-based)

- Zemplar’s long-term brand value has been pressured by the typical lifecycle for legacy specialty medicines: (1) time-limited exclusivity, (2) competitive substitution, (3) reduced promotional intensity, and (4) share displacement by other CKD-MBD treatments.

- The magnitude of revenue decline in later years depends on (a) how quickly any approved generics or authorized alternatives entered and (b) the competitiveness of substitutes with favorable net pricing.

When does Zemplar lose exclusivity, and what are the generic entry risks?

Exclusivity and generic entry risk

- The generic risk profile for legacy CKD-MBD brands is driven by:

- patent expirations covering active ingredient (paricalcitol), method-of-use, and specific formulations/strengths,

- FDA approval pathways for generics (ANDA) if permitted,

- any remaining exclusivities tied to specific references or listed products.

Paragraph IV and settlement dynamics

- For older brands, the key market risk is not a single event but the cadence of challenges across listed patents and product strengths. Market impact typically arrives in step-changes aligned to:

- first generic entry for one strength/route,

- subsequent entries that broaden availability,

- exclusivity carve-outs that delay some competitors but not others.

H3: What generic entry scenarios matter commercially?

- Single-strength entry: Limited volume impact if prescribers or units remain standardized on non-entered strengths.

- Multi-strength entry: Larger impact as formularies adjust and pharmacists swap.

- Injection versus capsule/solution divergence: Channel-specific competition can change mix and persistence.

(No complete, citable exclusivity or Orange Book patent list is included here because the prompt requires “hard data” and the cited dataset is not provided.)

How does Zemplar compare with competing CKD-MBD brands on market share pressure?

Competitive set dynamics

- Zemplar competes in the broader CKD-MBD treatment space that includes vitamin D analogs and calcimimetics.

- Brand performance generally depends on:

- formulary status (preferred versus non-preferred),

- net price positioning,

- clinician trust in dose titration and lab control.

Market share pressure patterns typical for Zemplar-type products

- Volume displacement occurs when a competitor has better net economics or easier access.

- Switching inertia is strongest at dialysis units that standardize therapy. When a unit switches, impact is abrupt and sustained.

- Clinical nuance (tolerability, calcium/phosphorus constraints) can preserve a minority of patients but rarely prevents broad share erosion.

H3: What are the most important “buying center” differences?

- Dialysis providers prioritize unit protocol fit and reimbursement mechanics.

- Nephrology practices outside dialysis respond to prior authorization and patient-specific titration needs.

- Hospitals may favor formulary bundles and procurement contracts that differ from outpatient pharmacy dynamics.

What does FDA regulatory status imply for Zemplar’s market trajectory?

Regulatory status as a commercial lever

- For legacy brands, FDA status matters mainly in how it enables generic competition and in whether product-specific exclusivities still apply.

- Post-approval changes (manufacturing, labeling updates, risk evaluation updates) affect availability and can shift prescribing patterns indirectly via safety perception and payer authorization requirements.

H3: What approval pathway effects matter?

- Generic approvals can quickly alter access because pharmacy benefit managers and dialysis formularies react to entry.

- Label changes can reclassify patient suitability, influencing which clinicians continue using Zemplar versus switching.

(No Zemplar-specific FDA milestone list is included because the necessary citable record set is not present in the provided information.)

How many patents protect Zemplar, and what are the most litigated IP buckets?

Patent estate commercialization relevance

- For drugs with long market history, the patent portfolio typically clusters into:

- composition/active ingredient,

- formulation and stability/vehicle,

- method-of-use for CKD sHPT and dosing titration,

- manufacturing processes.

- Market impact most often comes from:

- the last “blocking” patent tied to the exact product form and route,

- the method-of-use claims that sustain exclusivity after composition claims expire.

H3: How does patent strength translate to revenue risk?

- Broad, enforceable patents that cover product-specific formulations delay generic entry.

- Narrow patents that are easy to design around or avoid via alternative dosing or formulation can lead to faster erosion.

(No defensible patent count or expiration map is included due to missing cited Orange Book/patent litigation source material.)

What patent litigation and settlement outcomes affected Zemplar commercialization?

Litigation outcomes that typically shift revenue

- A settlement can:

- define “launch date” and delay generic entry,

- restrict generic strengths or routes,

- shape design-around tactics.

- A court decision can accelerate entry by removing remaining blocking barriers.

H3: How to interpret market effects

- Revenue usually shows stepwise effects aligned to:

- first launch (often limited set),

- expanded launches across strengths/routes,

- formulary rescoring by payers and dialysis entities.

(No case captions, district court outcomes, or settlement terms are included because the prompt requires hard data and no litigation dataset is provided.)

What licensing deals or “authorized” alternatives changed Zemplar’s competitive landscape?

Commercial structure that can preserve share

- Authorized generics or licensee products can reduce pricing while minimizing disruptive non-authorized entry.

- If a manufacturer controls distribution or offers branded-equivalent pricing strategies, the impact on net revenue can be dampened compared with unmanaged generic competition.

(No Zemplar-specific licensing/authorized generic deal terms are provided in the input, so none are listed.)

What are the commercial metrics that best predict Zemplar’s financial trajectory?

Metrics that drive investor-grade visibility

- Dispensing volume trends by channel (dialysis units vs retail).

- Net price and gross-to-net movements (rebates, chargebacks, contracting).

- Share-of-category within CKD-MBD treatments.

- Switching rate after competitive entry (time-to-formulary change).

- Persistence after dose adjustments due to calcium/phosphorus labs.

H3: Why persistence matters for specialty brands

- Even modest volume losses can produce disproportionate revenue declines when persistence shortens and patients discontinue or switch quickly.

Zemplar timeline: what to watch next in market and financials

Lifecycle markers that historically determine trajectory for legacy specialty CKD brands

- Blocking patent expiries or litigation rulings.

- First generic and subsequent expansion across strengths and routes.

- Contracting and formulary updates by dialysis organizations and large payers.

- Label changes or safety communications that affect prescribing behavior.

(A specific event timeline with dates is not included because it requires Orange Book and FDA/litigation sourcing not present in the provided materials.)

Key Takeaways

- Zemplar demand is driven by CKD-MBD protocols focused on PTH control, lab monitoring, and channel contracting, with dialysis standardization a major determinant of persistence and volume stability.

- Zemplar’s financial trajectory is most sensitive to gross-to-net compression and share displacement from other CKD-MBD therapies, especially calcimimetics and other vitamin D analogs.

- Generic entry risk is the dominant lifecycle factor for long-run revenue erosion, with commercial impact arriving in step-changes when entry expands across strengths/routes.

- Patent estate scope and litigation/settlement outcomes typically determine whether revenue decline is gradual (partial entry) or abrupt (broad entry).

- The most predictive commercial KPIs are net price trends, dispensing volume by channel, persistence, and time-to-formulary change after competitive entry.

FAQs

- How does dialysis formulary contracting change Zemplar switching rates?

- What payer policies most affect Zemplar net pricing (rebates, PA, step therapy)?

- Do generic entries for paricalcitol affect injection and oral routes differently?

- How do calcimimetics alter vitamin D analog add-on use in CKD-MBD?

- What KPIs should be used to forecast Zemplar revenue impact after patent expiry?

References (APA)

- (No citable sources were provided in the prompt.)