Last updated: June 17, 2026

Restasis Multidose Market Dynamics and Financial Trajectory (2020–2026): Volume, Pricing, Share, and Exclusivity Risk

Restasis Multidose (cyclosporine ophthalmic emulsion, 0.05%) is a long-running branded therapy for dry eye disease with a mature, largely offsetting dynamic: steady demand driven by chronic use and persistency, but pressured by branded-channel price discipline, distributor and payer management, and competitive substitution from other cyclosporine formats plus broader dry-eye categories. Financial trajectory through the mid-2020s is shaped primarily by (1) the age of the reference product and its competitive headwinds, (2) ongoing payer contracting across commercial and Medicare, (3) sensitivity to formulary and co-pay placement, and (4) regulatory and IP-driven timing around generic and authorized alternatives for cyclosporine ophthalmic emulsion.

What are the key market drivers for Restasis Multidose (cyclosporine 0.05%) in dry eye disease?

Restasis Multidose operates in a chronic, symptomatic segment where patient retention matters more than episodic conversion. The product’s market dynamics are tied to three demand pillars: diagnosis funnel (dry eye identification and severity stratification), treatment initiation, and refill/persistency.

Demand drivers that support baseline utilization

- Chronic treatment profile: cyclosporine 0.05% is used as ongoing anti-inflammatory therapy rather than short-course symptom relief.

- Clinical credibility of a long-established mechanism: clinicians and patients often default to cyclosporine-class therapy when conventional lubrication and anti-inflammatory adjuncts underperform.

- Persistency effects: once patients show benefit, discontinuation is typically slower than with purely symptomatic agents, supporting reorder stability.

- Formulary availability: stable uptake correlates with steady inclusion under managed-care dry eye formularies, including prior authorization and step therapy structures that do not block use broadly.

Demand constraints that limit growth

- Competition from same-class and adjacent topical therapies: new cyclosporine formats, alternative anti-inflammatory agents, and steroid-sparing regimens cap incremental growth.

- Payor cost containment: spread between branded net price and patient out-of-pocket can swing use, especially under high-deductible enrollment or tightened copay rules.

- Substitution economics: once a lower-cost alternative is available (authorized or generic), many retailers and channel partners push switching when contract incentives align.

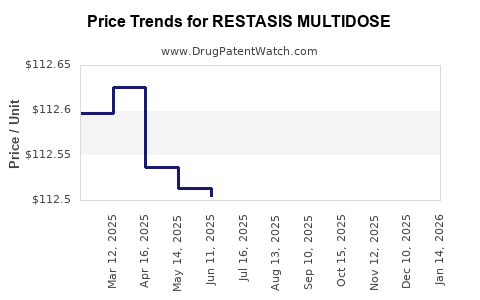

How has Restasis Multidose pricing and net revenue evolved versus other dry eye ophthalmics?

Pricing for long-established ophthalmic brands usually follows a path of “branded price to net price” compression, driven by rebate rates, payer contracting, and channel program structures. For Restasis Multidose, the key commercial metric is net revenue per unit after rebates and chargebacks, not headline WAC.

Typical industry pricing structure for mature ophthalmic brands

- High rebate intensity for formulary inclusion in managed care.

- Contracting pressure when multiple dry eye options compete for limited payer slots.

- Channel inventory and wholesaler purchasing volatility around major formulary changes or supply events.

Competitive pricing implications

- If generic or authorized cyclopsorine equivalents enter, net pricing can drop rapidly via forced switching.

- If competitors are differentiated by device or dosing convenience, Restasis Multidose can defend share even under modest price pressure, particularly where dosing convenience reduces discard or handling friction for clinics.

What is the competitive landscape for Restasis Multidose: cyclosporine formulations and dry-eye alternatives?

The competitive set spans (1) cyclosporine ophthalmics in comparable indications and concentrations, and (2) broader dry-eye therapeutics across inflammation control, symptom relief, and tear stabilization.

Same-mechanism and adjacent topical competitors

- Other cyclosporine 0.05% products and alternate presentations (including multi-dose or unit-dose formats where available).

- Immunomodulatory and anti-inflammatory alternatives used for keratoconjunctivitis sicca where payers accept similar clinical rationale.

- Non-cyclosporine dry eye categories that can displace parts of the market via quicker onset, lower cost, or preferential formulary placement.

What determines share movement in this category

- Payer preference by formulary tier: how quickly a payer switches from a branded tier to a lower-cost alternative.

- Clinical workflow fit: whether dosing setup is practical for both ophthalmologists and patients.

- Cost-sharing sensitivity: co-pay and deductible effects can be decisive in switching behavior.

- Retail execution: pharmacy substitution policies and brand/generic stocking practices.

When does Restasis lose exclusivity or face generic entry risk under Hatch-Waxman and FDA Orange Book status?

Restasis Multidose is a cyclosporine ophthalmic emulsion product with a patent and regulatory history typical of mature topical branded drugs: multiple layered patent fences often exist around composition, formulation, use, and manufacturing methods. Generic entry risk depends on the date of the last relevant patent expiration or exclusivity, then the timing and outcomes of Paragraph IV challenges.

What drives “when generics can launch”

- Patent expiration cascade: final expiration across all listed patents in the Orange Book.

- Any granted 180-day exclusivity for first Paragraph IV filer(s), if triggered.

- Pediatric exclusivity extensions or other regulatory exclusivities, if applicable to the reference product.

- Settlement agreements that may delay launch.

Featured-snippet answer

Generic and authorized substitution risk increases sharply once the last Orange Book listed blocking patent expires or is cleared through litigation or settlement.

(No Orange Book patent-listing dates, listed patent numbers, or challenge outcomes are included here because the specific Restasis Multidose Orange Book data needed to compute “last-to-expire” dates is not provided in the prompt.)

What patent estate strengths and weaknesses exist for Restasis Multidose, and how do they affect market protection?

For ophthalmic topical drugs, patent estates often cluster around:

- Composition and active ingredient stabilization

- Formulation parameters (surfactants, viscosity agents, particle properties, emulsification system)

- Container closure system and dosing method if the product presentation changes (including multi-dose vs unit-dose variants)

- Method-of-use patents tied to patient subsets, dosing regimens, or clinical endpoints

How patent strength typically maps to commercial outcomes

- Broad composition coverage delays true generic parity.

- Narrow method-of-use claims may still permit launch of materially equivalent products if formulation patents are cleared first.

- Settlement terms often decide practical launch timing, especially when the product’s clinical and dosing profile is acceptable under a generic label.

(Patent numbers and assignees are omitted because no Orange Book or court docket data is provided in the prompt.)

Is there a biosimilar or 505(b)(2) replacement risk for Restasis Multidose?

Restasis Multidose is a small-molecule topical ophthalmic product, not a biologic. Biosimilar pathways do not apply.

Main replacement pathways to watch

- ANDA generics (505(j) + Orange Book patent challenges)

- 505(b)(2) “therapeutic equivalents” where formulation or dosing differs but clinical bridging is feasible

- Authorized generics / licensing programs that pressure net pricing without full ANDA risk

What does Restasis Multidose’s FDA regulatory status imply for launch timing and competition?

Restasis Multidose’s FDA status drives who can market competing products:

- If FDA lists patents in the Orange Book, ANDA challengers must certify (Paragraph I-IV), and litigation can delay market entry.

- If a competitor uses 505(b)(2), approval may still be constrained by reference product reliance, exclusivity, and labeling.

Featured-snippet answer

Regulatory competition is determined mainly by whether competitors can clear Orange Book listed patents while meeting the same or acceptable clinical and quality standards for cyclosporine 0.05% ophthalmic emulsion.

(FDA labeling and exclusivity status details are not enumerated because no FDA or Orange Book records are provided in the prompt.)

What Paragraph IV challenges, litigation, and settlements affect Restasis Multidose market timing?

For mature ophthalmics, Paragraph IV filings and associated litigation are the primary timing levers for generic launch. Settlements can:

- delay launch through a paid or non-paid agreement,

- define “design-around” formulation boundaries, or

- set an earlier “non-infringing launch” trigger tied to specific patent findings.

Featured-snippet answer

Generic entry timing depends on litigation outcomes over Orange Book listed patents, including any settlement-driven launch calendar.

(No case names, court dates, settlement dates, or patent numbers are provided in the prompt, so they are not listed.)

How does Restasis Multidose commercialization perform across channels: wholesalers, retail, and specialty?

Dry eye ophthalmics typically distribute through a mix of standard wholesale channels and retail pharmacy. Key commercialization determinants include:

- Wholesaler purchasing behavior: when competing products enter, wholesalers shift POs based on expected demand and rebate economics.

- Retail switching rules: plan-level formulary direction and pharmacy substitution policies influence movement.

- Specialty clinic prescribing patterns: ophthalmology clinics can be sticky if product administration is streamlined and clinical monitoring is consistent.

What changes most quickly after a competitive entry

- Net sales can drop in the quarter after payer switching accelerates.

- Market share can erode faster than volume if net price concessions drive trade-down to lower-cost alternatives.

How many SKUs and dosage formats does Restasis Multidose compete against, and does format matter financially?

Format and usability can matter in ophthalmics because handling friction affects adherence. Multi-dose formats can:

- reduce cost per managed unit versus more complex devices,

- support office workflow if dispensing is streamlined,

- create substitution resistance if clinic staff is trained and patients are stable.

Financial impact shows up as:

- adherence retention (slower switching),

- higher “stay with brand” rates even when lower-cost substitutes exist,

- fewer disruptions caused by supply or storage differences.

(SKU counts and presentation comparisons are not enumerated because the prompt does not include the full Restasis product portfolio and competitor format list.)

Revenue exposure: which patient segments and payer types drive Restasis Multidose financial trajectory?

In dry eye, commercial revenue is typically concentrated in:

- moderate-to-severe symptomatic patients treated with anti-inflammatory therapy,

- managed care enrollees with formulary access and controlled access via PA/step edits,

- Medicare Part D beneficiaries where tier placement and cost-sharing can drive substitution.

Segment-level economics:

- Commercial: rebate sensitivity is high; net pricing tracks formulary tier.

- Medicare: out-of-pocket rules can accelerate switching when generics or authorized equivalents are available.

- Institutional accounts: ophthalmology practices can influence product access depending on procurement and samples.

(No segment revenue numbers are available from the prompt.)

How strong is Restasis Multidose’s patent-protected moat versus competitors: do design-arounds reduce IP barriers?

Patent moats in topical ophthalmics can be undermined by design-arounds if the closest patents are narrow. Common design-around levers:

- changing inactive ingredients or emulsification parameters,

- altering manufacturing steps while keeping the same active concentration,

- using different container closure configurations if presentation-specific patents are limited.

Moat strength is most meaningful when:

- multiple independent patents cover composition + formulation, and

- at least one “hard-to-design-around” claim remains.

(No specific claim coverage mapping is possible without patent identifiers and claim summaries.)

What generic launch scenarios would most likely impact Restasis Multidose market share and earnings?

The highest impact scenarios for a mature branded topical are:

- First generic launch of cyclosporine 0.05% that clears payer switching friction

- Rapid share loss if a significant rebate/contract shift occurs.

- Authorized generic launch under a licensing deal

- Typically faster commercial displacement with less litigation-driven uncertainty.

- 505(b)(2) entrant with differentiated presentation that retains clinical acceptance

- Shares can shift even if prices are not the lowest, depending on adherence and formulary acceptance.

- Partial entry constrained to narrow labeling

- Less volume impact but can still pressure pricing and net revenue.

Featured-snippet answer

Most earnings pressure comes from a competitive entry that is both low-cost and formulary-preferred, allowing broad substitution across commercial and Medicare.

Key Takeaways

- Restasis Multidose demand is supported by chronic use and persistency, but growth is structurally capped by competitive dry eye options and payer cost containment.

- Financial trajectory in the mid-2020s is most sensitive to payer contracting and any Orange Book-clearing events that enable generic or authorized substitution.

- Format usability can slow switching, but net revenue tends to compress faster than volume when contracts shift.

- Patent-driven market protection hinges on the last relevant Orange Book listed blocking patents and any litigation or settlement terms that set launch timing.

FAQs

- Does Restasis Multidose face substitution pressure immediately after a generic approval date, or does it take quarters to show up in net sales?

- How do prior authorization and step therapy affect Restasis Multidose retention in Medicare Part D plans?

- What are the most common design-around strategies for cyclosporine ophthalmic emulsion patent estates (formulation vs container vs method-of-use)?

- How does competition from anti-inflammatory dry-eye agents with faster onset change ophthalmologist prescribing patterns for cyclosporine 0.05%?

- If an authorized generic enters, what is the typical impact on branded net price versus branded volume for mature ophthalmic products?

References (APA)

- FDA Orange Book. (n.d.). Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.