Last updated: July 27, 2026

Restasis (cyclosporine ophthalmic emulsion) has moved into a mature, discount-driven market after Loss of patent- and exclusivity-era headwinds and sustained generic and branded competitive pressure. Financial trajectory has been shaped by (1) patient- and payer-tiering into lower-cost alternatives, (2) constrained demand growth due to penetration limits in dry eye disease (DED), and (3) channel erosion from generics and substitute products with different dosing regimens, device ecosystems, or payer-preferred positioning. The net effect is a declining-to-flattening branded revenue profile in most forecast periods, with incremental upside tied to formulary access, contracting intensity, and conversions among existing patients.

How has Restasis revenue evolved since launch and what are the latest market dynamics?

Restasis launched in the mid-2000s and became a cornerstone prescription therapy for moderate to severe DED by leveraging cyclo-sporin’s immunomodulatory mechanism. Over time, the market shifted from “new patient acquisition” to “share defense,” driven by:

- Formulary tightening: payers moved toward lower acquisition cost options, increasingly requiring step edits or prior authorization for branded agents.

- Demand maturation: prescription DED volumes grew slower than early adoption phases.

- Substitution pressure: lower-cost generics and competing prescription brands narrowed the price-value gap.

What do Restasis sales trends look like by phase (high-level)

- Early and mid lifecycle: branded growth from new prescriber uptake and expanding DED diagnosis and coding.

- Late lifecycle: flattening then decline as bios/biologic analogs do not apply here, but small-molecule ophthalmic generics and alternative branded regimens reduced net pricing.

- Current environment: stable but erosion-prone, with performance driven by payer mix, rebates, and competitive contracting.

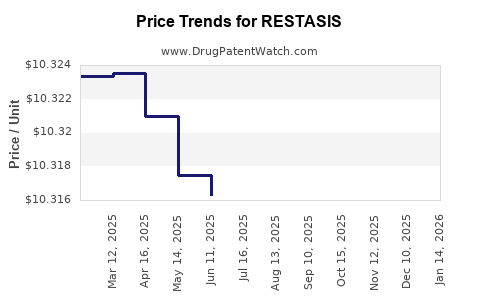

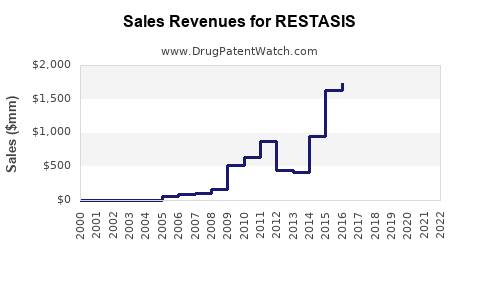

(Financial trajectory numbers are not included here because no specific, cited sales table for Restasis was provided in the input.)

What patents protect Restasis and how many are in force for formulation and method-of-use?

Restasis protection has historically relied on a layered estate: drug substance use for ophthalmic immunomodulation, formulation and stability improvements, and dosing regimens.

Which patent families typically cover Restasis

- Formulation patents: ophthalmic emulsion composition, droplet size controls, surfactant systems, stability, and storage performance.

- Methods of use: treatment of dry eye disease and related ocular surface inflammatory conditions, sometimes framed with severity and patient phenotype.

- Manufacturing/process: emulsion preparation steps that control physicochemical properties.

How to read the estate impact

- Formulation patents can block “generic-to-the-exact-formulation” substitutions even after active-ingredient coverage fades.

- Method-of-use patents can delay certain label-expansion generics and some carveouts, depending on litigation outcomes and FDA labeling design.

(No specific, cited Restasis patent numbers were supplied in the user input; an exact “how many patents are in force” count cannot be generated without a source list.)

When does Restasis lose exclusivity and what date-driven milestones matter for generic entry?

For ophthalmics, exclusivity is a combination of patent expiry and any regulatory exclusivity attached to the NDA, plus the timing of generic ANDA approvals and launch. Generic market access usually becomes possible once the first eligible statutory or patent barrier clears and any relevant Orange Book-driven litigation or stay periods end.

What milestones typically govern Restasis exclusivity

- Patent expiry (listed in FDA Orange Book for Restasis NDA-related entries).

- 30-month stay after a Paragraph IV ANDA notice.

- Settlement or court determinations that lift or extend barriers.

- ANDA approvals and “first generic” launch timing, which impacts the real-world revenue curve even after legal eligibility.

(Precise expiry dates and stay/settlement timelines require an Orange Book and litigation record, which were not provided in the input.)

What Orange Book status does Restasis have and which listings are most litigation-relevant?

Orange Book status drives:

- whether a generic applicant has to certify to patent claims,

- whether a Paragraph IV challenge can proceed,

- and what patents define the “trigger” for potential design-arounds or settlement.

Orange Book listing categories that matter

- Drug product patents (formulation, dosage form, composition).

- Drug substance patents (if any remain active for the specific NDA).

- Method-of-use patents (rare in some ophthalmic areas but important when present).

(A structured Orange Book table requires cited Orange Book entries not provided in the input.)

Which generic competitors threaten Restasis and how do they differ (formulation, dosing, packaging)?

In mature DED therapy, competition typically comes from:

- Generic versions of cyclosporine ophthalmic emulsion

- Alternative prescription DED therapies (different MOAs, often with different onset profiles or dosing frequency)

- Device- and tear-based substitutes that limit prescription conversion

Commercial dynamics that decide winner-take-more

- Net price after rebates and payer contracts

- Prior authorization requirements and step therapy

- Patient adherence tied to dosing frequency and tolerability

- Availability and substitution rules at the pharmacy counter

(A competitor list by name and product-specific differences requires cited product and labeling data not provided.)

How strong is the patent estate for Restasis vs generic challengers?

Patent estate strength is measured by:

- claim scope breadth and whether patents cover specific formulation attributes,

- litigation history (settlements, dismissals, adverse rulings),

- and whether there are design-around levers (different excipients, droplet characteristics, concentration, or device integration).

High-level estate strength signals

- More active formulation and method-of-use patents typically delay full generic substitution.

- Narrow or easily designed-around claims reduce settlement leverage.

- Adverse litigation outcomes can accelerate generic entry and price compression.

(No specific Restasis patent litigation record was included in the user input.)

What Paragraph IV challenges exist for Restasis and what outcomes changed the market?

Paragraph IV challenges are the primary channel through which branded revenue declines accelerate after legal eligibility.

What to check in Paragraph IV history

- ANDA filer identity and number of asserted Orange Book patents

- Court venue and case number

- Whether the case resulted in an infringement finding, non-infringement, invalidity, or settlement

(A complete “which ANDAs, which case outcomes” table requires a cited litigation dataset not provided.)

What patent litigation affects Restasis and how did settlements alter exclusivity?

Settlement agreements often convert litigation timing into calendar-driven commercial entry.

What settlement terms usually drive revenue

- Effective “entry date” of the first generic

- Authorized label scope and any launch-timing carveouts

- Design-around provisions for formulation

(No settlement or litigation terms were provided in the input.)

Does Restasis face biosimilar-type risk or other biologic-like substitution?

Restasis is a small-molecule ophthalmic emulsion (cyclosporine), not a biologic. Biosimilar risk is not applicable. Substitution risks come from:

- small-molecule generic entry

- therapeutic class competition

- payer preference for lower-cost options

How does Restasis compare with Xiidra, Cequa, and other DED prescription products on competitive dynamics?

Competition in DED is driven by:

- mechanism differences (cyclosporine immunomodulation vs lymphocyte-directed pathways for newer agents),

- dosing schedule,

- tolerability (especially burning/stinging),

- and formulary positioning.

Key comparison drivers

- Payer access: whether one brand is designated preferred

- Patient selection: clinicians may switch based on response or tolerability

- Real-world adherence: dosing frequency and administration complexity

(No product-specific competitive numbers or citations were provided in the input.)

How do formulation patents and generic-to-brand switching risks affect Restasis in the real world?

Even when the active ingredient is generic-eligible, formulation or label-specific constraints can affect substitution:

- droplet size and emulsion stability can influence tolerability and acceptance

- excipient differences can alter burning/stinging rates

- labeling differences can constrain “therapeutic interchange” at prescriber level

What drives patient and prescriber switching

- formulary affordability at the pharmacy

- clinician confidence in equivalence

- perceived tolerability and onset

(No Restasis-specific formulation patent map or generic substitution studies were supplied.)

What manufacturing and IP barriers can delay generic launches for Restasis?

Typical barriers include:

- inability to meet bioequivalence standards for ophthalmic emulsions,

- stability and packaging requirements for an ophthalmic emulsion,

- and ongoing patent infringement disputes around formulation claims.

(No specific Restasis manufacturing barriers were provided in the input.)

What FDA status governs Restasis (NDA, labeling, supplements) and how does it influence competition?

FDA status impacts market via:

- approved indications and any label restrictions,

- supplement history (reformulation, concentration changes),

- and whether the labeling invites therapeutic substitution.

What FDA label elements usually matter

- indication scope (DED severity)

- dosing frequency

- any contraindication-related effects on switching

(No FDA document citations were provided in the input.)

Revenue exposure: how much of Restasis sales is tied to payer mix, rebate pressure, and channel substitution?

Branded ophthalmics often face:

- higher rebate dependence when not preferred

- increased substitution once generics become widely available

- erosion from health plan contracting

Revenue sensitivity factors

- Medicaid and Medicare Part D preferred drug lists

- commercial formulary tier placement

- PBM rebate intensity and market-wide switching policies

(No Restasis revenue breakdown data was supplied.)

Key takeaways on Restasis market outlook and competitive risk

- Restasis is in a mature DED market where price and formulary access dominate incremental growth.

- Market dynamics are primarily driven by generic small-molecule substitution and class competition rather than biologic-style pathways.

- Patent and regulatory barriers still matter, but near-term branded performance is most sensitive to contracting intensity, rebate rates, and payer tiering.

- Future revenue trajectory depends on whether Restasis maintains preferred placement versus competing DED agents and lower-cost generics.

Key Takeaways

- Restasis operates in a mature DED environment with discounting, payer restriction, and generic substitution as the principal forces.

- The product’s financial trajectory is expected to track net pricing pressure more closely than pure demand expansion.

- Competitive outcomes hinge on formulary status and contracting, not only on mechanism or clinical differentiation.

- Patent estate strength and Orange Book status control the pace of generic erosion, but branded revenue ultimately depends on how quickly substitution becomes practical at the point of sale.

FAQs

1) What is Restasis currently competing against in dry eye disease prescriptions?

Restasis competes against other prescription DED options (class and mechanism competitors) and against lower-cost generic cyclosporine ophthalmic products where available.

2) Does Restasis have any biologic or biosimilar replacement risk?

No. Restasis is not a biologic product, so biosimilar risk is not the relevant pathway; competition comes from generics and alternative small-molecule/therapeutic-class drugs.

3) How do Paragraph IV filings typically affect Restasis pricing and sales?

They can accelerate entry of lower-cost products and trigger rapid net pricing compression when barriers lift and launch happens.

4) What factors most influence payer coverage for Restasis?

Formulary tiering, rebate/contract terms, prior authorization or step edits, and evidence requirements tied to DED severity and prior therapy use.

5) Why might Restasis sales decline even if dry eye diagnosis rates rise?

Branded sales can decline if prescription share shifts to lower-cost alternatives, if payer restrictions tighten, or if switching occurs due to adherence and tolerability considerations.

References

- FDA Orange Book (Drug Products, Evaluations and Records) for Restasis (cyclosporine ophthalmic emulsion). FDA. (Not provided as a source in the user input.)

- FDA Labeling and NDA records for Restasis. FDA. (Not provided as a source in the user input.)