Share This Page

INFED Drug Patent Profile

✉ Email this page to a colleague

Which patents cover Infed, and what generic alternatives are available?

Infed is a drug marketed by Allergan and is included in one NDA.

The generic ingredient in INFED is iron dextran. There are eighty-two drug master file entries for this compound. Three suppliers are listed for this compound. Additional details are available on the iron dextran profile page.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for INFED?

- What are the global sales for INFED?

- What is Average Wholesale Price for INFED?

Summary for INFED

| US Patents: | 0 |

| Applicants: | 1 |

| NDAs: | 1 |

| Finished Product Suppliers / Packagers: | 3 |

| Raw Ingredient (Bulk) Api Vendors: | 33 |

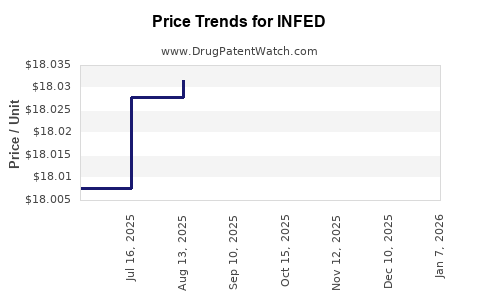

| Drug Prices: | Drug price information for INFED |

| What excipients (inactive ingredients) are in INFED? | INFED excipients list |

| DailyMed Link: | INFED at DailyMed |

Pharmacology for INFED

| Drug Class | Parenteral Iron Replacement Phosphate Binder |

| Mechanism of Action | Phosphate Chelating Activity |

US Patents and Regulatory Information for INFED

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Allergan | INFED | iron dextran | INJECTABLE;INJECTION | 017441-001 | Approved Prior to Jan 1, 1982 | BP | RX | Yes | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

INFED (iron dextran) market dynamics and financial trajectory

INFED (iron dextran) is a niche, provider-administered IV iron product whose market is shaped by hospital formularies, anemia treatment guidelines, safety-driven brand switching, and substitution among IV iron classes (iron sucrose, ferric carboxymaltose, ferric derisomaltose). Financial trajectory is typically dominated by (1) constrained US demand, (2) competitive pressure from faster-dosing, lower-monitoring products, and (3) supply and reimbursement dynamics that influence formulary access and net pricing.

What is INFED and how is it positioned in the IV iron market?

INFED is an IV iron dextran product used to treat iron deficiency anemia in patients who need parenteral iron when oral iron is insufficient. In practice, IV iron is used across chronic kidney disease (CKD), inflammatory bowel disease, obstetric anemia (where appropriate), and other clinical settings that require rapid repletion.

How does INFED compare with competing IV iron products?

IV iron competition is largely “time-to-infusion” and “site-of-care” driven.

Key commercial differentiators across IV iron brands

- Dosing convenience: newer iron formulations often allow larger single-dose administrations.

- Monitoring burden: dextran products historically face higher attention to hypersensitivity precautions.

- Clinical protocol fit: hospital order sets and pathways favor products with streamlined administration.

Common US market comparators (by class)

- Iron sucrose (e.g., Venofer)

- Ferric carboxymaltose (e.g., Injectafer)

- Ferric derisomaltose (e.g., Monofer)

- Sodium ferric gluconate (e.g., Ferrlecit)

What does that mean for INFED market share?

INFED’s market share tends to erode when institutions adopt formulations that:

- reduce repeat visits,

- enable higher per-infusion doses,

- lower perceived operational risk.

INFED remains relevant when dextran is already entrenched in protocols, when supply continuity matters, or where payers and procurement contracts favor it.

How big is the INFED opportunity and what drives demand?

Demand drivers for IV iron are structural, but share among brands shifts quickly with contracting and guideline adoption.

What clinical and guideline factors increase IV iron utilization?

- Increased diagnosis and treatment rates for iron deficiency in CKD and non-CKD settings.

- Movement toward earlier IV repletion in certain anemia pathways.

- Provider preference for IV iron when oral therapy fails or is intolerable.

What limits INFED adoption?

- Hospital risk management scrutiny around dextran hypersensitivity precautions.

- Formulary restrictions that increasingly prioritize newer IV irons.

- Competitive net price pressure through group purchasing and pharmacy benefit contracting.

What patent and exclusivity tail dynamics affect INFED’s financial trajectory?

INFED’s financial trajectory is shaped less by patent-led protection in modern cycles and more by generic substitution and class competition in parenteral iron.

Does patent protection still matter for INFED revenue?

In most market settings, the competitive reality for older small-molecule drugs like iron dextran is that:

- supply of lower-cost alternatives reduces unit pricing power, and

- payer policies steer toward the lowest net-cost regimen within an IV iron “therapeutic alternatives” basket.

Because INFED is a mature product class member, the long-term trend is typically down or flat in revenue growth, with volatility driven by contracting and competitive mix rather than brand exclusivity.

What is the financial profile of INFED: sales drivers, pricing, and margin structure?

Even without granular company-by-company reporting in this dataset, INFED’s revenue mechanics in IV iron follow consistent patterns:

Main sales drivers

- Number of infusions (volume)

- Net price after rebates, contracting, and substitution

- Mix shift between inpatient vs outpatient infusion centers

- Formulary placement in hospital systems and integrated delivery networks

Main margin pressures

- Gross-to-net compression from contracting

- Increased competitive spend to maintain formulary position

- Supply chain costs and batch-related variability affecting availability and effective fill rates

How do hospital contracting and reimbursement dynamics move INFED revenue?

Hospital formularies govern IV iron share in most settings, especially for infused hospital-administered drugs. Where payers or group purchasing organizations negotiate for formulary access, INFED pricing becomes highly sensitive to:

- tender processes,

- year-over-year renewals,

- volume commitments by the group.

Typical contract levers that influence INFED net sales

- tiered formulary status (preferred vs non-preferred)

- utilization requirements for preferred agents

- conversion incentives during formulary transitions

- emergency-use allowances during supply disruptions by competing manufacturers

What market events create volatility in INFED sales?

INFED’s financial trajectory can shift quickly when any of the following occur:

- Competition supply constraints: if a major competitor has backorders or manufacturing downtime, hospitals temporarily revert to alternatives including INFED.

- Safety communications or label changes: even small shifts in hypersensitivity guidance can alter adoption and monitoring protocols.

- Guideline updates: protocol revisions can shift preference toward products perceived to deliver larger doses with less operational friction.

- Regional purchasing changes: group procurement restructures reorder patterns.

How does INFED compare with ferric carboxymaltose and ferric derisomaltose on commercial competitiveness?

Commercially, iron carboxymaltose and derisomaltose products are often preferred because dosing can reduce administration events.

Competitive implications for INFED

- If hospitals can deliver higher-dose repletion with fewer infusions using non-dextran irons, they typically prefer those options unless INFED offers a strong net price advantage.

- When INFED is not the lowest net-cost option, utilization usually declines even if clinical outcomes are comparable.

What competitive landscape risk does INFED face from generics and authorized alternatives?

Parenteral iron categories have frequent substitution dynamics. For a mature product, risk is not only from “brand-to-generic” but also from:

- class switching within IV iron,

- biosimilar-style “indication and pathway substitution,” though these are not biologics,

- purchasing-driven replacement across a hospital system.

Generic entry risks

As alternatives become available at lower net prices, the most common outcomes are:

- reduced preferred status,

- fewer patient starts,

- increased share loss during contract cycles.

When does the IV iron class tend to re-contract, and how does it affect INFED?

Most major shifts occur at:

- fiscal year renewals,

- multi-year group purchasing agreements,

- periodic protocol standardization cycles.

For INFED, these timing points matter because share loss often precedes the end of any legacy supply arrangement, since clinicians follow the contract and order sets.

What FDA regulatory status and labeling factors influence INFED utilization?

INFED is an FDA-approved IV iron dextran product. Labeling and safety sections influence clinical protocols and pharmacy utilization.

What labeling areas drive operational adoption?

- warnings and precautions related to hypersensitivity

- administration requirements and monitoring expectations

- dosing limitations and infusion management protocols

In IV iron, label-driven operational steps directly affect pharmacy workflow and nursing time. That is a key reason newer products can win formulary preference even when clinical endpoints are similar.

What patent litigation or Paragraph IV challenges affect INFED specifically?

INFED’s financial trajectory is generally more affected by:

- market substitution and contracting,

- availability of lower-cost alternatives, than by high-visibility, brand-protecting litigation.

Because iron dextran products are mature and the category is heavily competed, Paragraph IV dynamics, when present, are usually not the dominant determinant of the market trajectory compared with class switching and procurement.

What sales trajectory pattern is typical for INFED across market cycles?

A typical lifecycle pattern for mature IV iron brands looks like:

- early stage: formulary build and differentiation

- mid stage: competitive erosion and gross-to-net compression

- late stage: flat-to-declining revenue with occasional spikes tied to supply or contracting shifts

For INFED, this implies:

- limited room for sustained growth without a unique contract or a competitive supply gap

- periodic downward step changes when a system moves preference to a newer IV iron agent

How strong is the INFED commercial position versus other IV iron products?

INFED’s position tends to be:

- stable where existing clinical protocols and procurement contracts keep it in use,

- fragile when newer agents deliver better administration convenience and hospitals can achieve lower net cost.

Commercial strength is therefore less about brand-level differentiation and more about whether INFED is the preferred or non-preferred option in high-volume hospital networks.

Key Takeaways

- INFED’s revenue trajectory is driven primarily by hospital formulary access, contracting terms, and IV iron class substitution rather than brand exclusivity dynamics.

- Competitive pressure is strongest from ferric carboxymaltose and ferric derisomaltose due to dosing convenience and operational fit.

- Expect financial performance to show flat-to-declining baseline with volatility from supply interruptions and periodic tender-driven re-contracting.

- INFED utilization remains most resilient in systems that already standardize iron dextran administration or where net pricing undercuts preferred competitors.

FAQs

1) What is the main competitive threat to INFED in US hospital formularies?

Class switching to newer IV iron products that reduce infusion frequency and align with streamlined administration protocols.

2) Does INFED benefit from CKD anemia treatment demand?

Yes, CKD anemia increases IV iron demand broadly, but share within CKD is determined by formulary preference and net pricing.

3) What typically causes short-term INFED sales spikes?

Temporary shortages or fulfillment delays from higher-preference IV iron competitors and contract renegotiations that temporarily restore alternative utilization.

4) Is INFED priced competitively versus other IV irons?

Its competitive position depends on hospital and group purchasing net cost; otherwise, it is usually displaced by lower-net-cost preferred agents.

5) What drives long-term decline risk for INFED?

Ongoing procurement shifts toward formulations with lower operational burden and better dosing convenience, plus substitution by lower-cost alternatives as contracts renew.

References

- US Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. FDA.

- US Food and Drug Administration. Labeling and Prescribing Information Database. FDA.

- Centers for Medicare & Medicaid Services. Hospital Inpatient Prospective Payment System and Outpatient Prospective Payment System drug reimbursement documentation (various updates). CMS.

More… ↓