Last updated: August 8, 2026

Hydrochlorothiazide is a mature, low-cost generic diuretic with broad use in hypertension, edema, and fixed-dose combination products. Its standalone financial trajectory is structurally declining or flat because of intense generic competition, limited pricing power, and substitution by newer antihypertensive regimens. Commercial value remains material through combination products, hospital formularies, and high prescription volume, but the active ingredient has little remaining patent or regulatory exclusivity.

What is hydrochlorothiazide and how is it used?

Hydrochlorothiazide, often abbreviated HCTZ, is a thiazide diuretic that promotes renal sodium and water excretion. The FDA-approved uses include hypertension and edema associated with congestive heart failure, hepatic cirrhosis, corticosteroid therapy, and estrogen therapy, subject to product labeling.[1]

Hydrochlorothiazide is marketed in several forms:

- Standalone tablets, commonly 12.5 mg, 25 mg, and 50 mg.

- Fixed-dose combinations with angiotensin-converting enzyme inhibitors.

- Fixed-dose combinations with angiotensin II receptor blockers.

- Combinations with beta blockers.

- Combinations with potassium-sparing diuretics.

- Combination products used for hypertension and cardiovascular risk reduction.

Common combination products include:

| Combination |

Representative brand or generic product |

Commercial role |

| Losartan/HCTZ |

Hyzaar and generics |

Major antihypertensive combination |

| Valsartan/HCTZ |

Diovan HCT and generics |

Established ARB combination |

| Irbesartan/HCTZ |

Avalide and generics |

Established ARB combination |

| Lisinopril/HCTZ |

Zestoretic and generics |

Established ACE inhibitor combination |

| Benazepril/HCTZ |

Lotensin HCT and generics |

Mature ACE inhibitor combination |

| Bisoprolol/HCTZ |

Ziac and generics |

Mature beta blocker combination |

| Triamterene/HCTZ |

Dyazide and generics |

Diuretic combination with potassium-sparing component |

The commercial economics of HCTZ therefore divide into two segments: low-value standalone tablets and higher-value, but still heavily commoditized, combination products.

How large is the hydrochlorothiazide market?

The market is large by prescription volume but modest by branded pharmaceutical revenue. Public market reports often combine hydrochlorothiazide with broader categories such as thiazide diuretics, antihypertensives, or combination cardiovascular products. Those estimates are not directly comparable because they use different definitions of active ingredient, geography, dosage form, and combination-product revenue.

The commercial profile is clearer than any single market-size estimate:

| Market metric |

Hydrochlorothiazide position |

| Prescription volume |

High, supported by chronic hypertension treatment |

| Average generic price |

Low |

| Branded standalone revenue |

Minimal |

| Generic competition |

Extensive |

| Combination-product revenue |

More significant than standalone HCTZ revenue |

| Market growth |

Low to negative in nominal standalone terms |

| Volume drivers |

Aging populations, hypertension prevalence, low-cost prescribing |

| Volume constraints |

Generic substitution, guideline changes, competing antihypertensive classes |

| Margin profile |

Thin for commodity tablets; better for differentiated combinations and supply reliability |

HCTZ remains widely prescribed because hypertension is chronic, prevalence is high, and thiazide-type diuretics remain recognized treatment options. The 2017 American College of Cardiology and American Heart Association hypertension guideline identified thiazide diuretics, calcium channel blockers, ACE inhibitors, and ARBs as first-line classes for many adults with hypertension.[2]

The market does not behave like a conventional branded-drug market. Manufacturers compete primarily on price, manufacturing cost, supply continuity, wholesaler access, and contract terms. Brand equity has limited relevance for standalone HCTZ.

When did hydrochlorothiazide lose exclusivity?

Hydrochlorothiazide lost meaningful exclusivity decades ago. The active ingredient was introduced before the modern Hatch-Waxman patent and FDA exclusivity framework. Generic hydrochlorothiazide products have been available for many years, and the FDA lists multiple approved abbreviated new drug applications for HCTZ tablets and combination products.[3]

There is no commercially relevant current patent term protecting hydrochlorothiazide as a standalone active ingredient. The compound is a mature small molecule, and standard patent terms for the original active ingredient expired long ago.

FDA regulatory status

Hydrochlorothiazide is approved as a prescription drug. It is available as a generic active ingredient and as part of numerous approved fixed-dose combination products. FDA labeling identifies contraindications and clinically relevant risks, including anuria, hypersensitivity to sulfonamide-derived drugs, electrolyte abnormalities, renal effects, and photosensitivity-related concerns.[1]

The FDA has also required labeling updates concerning non-melanoma skin cancer risk associated with cumulative hydrochlorothiazide exposure. In 2020, the FDA approved labeling changes reflecting observational evidence of increased risk, particularly at higher cumulative doses.[4]

That safety issue has not created a new exclusivity period for the active ingredient. It can affect physician selection, patient counseling, product labeling, and long-term demand at the margin.

What patents protect hydrochlorothiazide?

Very few commercially meaningful patents protect the basic hydrochlorothiazide product. The principal intellectual-property position is concentrated in:

- Historical composition-of-matter patents that have expired.

- Old formulation patents that have expired or have limited commercial relevance.

- Combination-product patents, where applicable.

- Method-of-use patents for particular combinations or patient populations.

- Manufacturing and process patents that may protect efficiency rather than market exclusivity.

- Trade secrets involving crystallization, impurity control, scale-up, and manufacturing yield.

Patent estate assessment

| Patent category |

Current commercial importance |

| Hydrochlorothiazide composition of matter |

Negligible; expired |

| Standalone tablet formulation |

Low; generally expired or non-blocking |

| Fixed-dose combination formulation |

Moderate in selected products, but most major products are generic |

| Method of use |

Limited and product-specific |

| Manufacturing process |

Potentially relevant to cost and supply, rarely a market blocker |

| Device or delivery technology |

Minimal for conventional oral tablets |

| Regulatory exclusivity |

None of practical importance for the mature active ingredient |

An exact current Orange Book patent listing must be evaluated product by product because the relevant patents attach to specific approved products, not to hydrochlorothiazide as an abstract molecule. For most longstanding generic HCTZ tablets, there is no blocking patent estate comparable to that of a branded small molecule or biologic.

What is the Orange Book status of hydrochlorothiazide?

The Orange Book lists approved drug products and, where applicable, patent and exclusivity information for FDA-approved products.[5] Hydrochlorothiazide appears across multiple products and application types, including combination products.

The Orange Book status is best understood as fragmented:

- Standalone generic HCTZ tablets generally have no meaningful market exclusivity.

- Brand-name combination products may have historical patent listings, but many have expired.

- Current patent exposure depends on the specific NDA, dosage form, strength, and product sponsor.

- ANDA applicants may have filed Paragraph IV certifications against patents associated with branded combination products where those patents remained listed.

Because most HCTZ volume is supplied by generic products, Orange Book-listed patents do not create a unified barrier to market entry for the ingredient.

Which companies manufacture hydrochlorothiazide?

Manufacturing is distributed across generic pharmaceutical companies and contract manufacturers. The competitive field has included major generic suppliers such as Teva Pharmaceutical Industries, Sandoz, Mylan, Solco Healthcare, Zydus Pharmaceuticals, Torrent Pharmaceuticals, Lupin, and other FDA-approved suppliers, depending on product, strength, and market period.

The relevant competitive advantage is usually operational:

- API sourcing and qualification.

- FDA-compliant finished-dose manufacturing.

- Reliable supply of multiple strengths.

- Low tablet production cost.

- National wholesaler distribution.

- Ability to remain profitable during price compression.

- Quality-system performance and avoidance of supply interruptions.

No single company controls the HCTZ market. Supply may be concentrated for an individual strength or product at a given time, but the active ingredient has multiple approved suppliers.

How do generic entry and Paragraph IV challenges affect hydrochlorothiazide?

Generic entry has already transformed HCTZ into a commodity market. Paragraph IV litigation is historically more relevant to branded combination products than to standalone HCTZ.

Under the Hatch-Waxman framework, an ANDA applicant can certify that a listed patent is invalid, unenforceable, or not infringed. A Paragraph IV certification may trigger patent litigation and, in certain circumstances, a 30-month stay of FDA approval.[6] For old HCTZ combinations, this process occurred primarily when branded products still had unexpired formulation or combination patents.

Current generic entry risks are therefore asymmetric:

| Product segment |

Generic-entry risk |

| Standalone HCTZ 12.5 mg, 25 mg, 50 mg |

Already realized; high competition |

| HCTZ with older ACE inhibitors |

High; mature generic segment |

| HCTZ with older ARBs |

High; mature generic segment |

| Newer or reformulated combinations |

Depends on product-specific patents |

| Branded extended-release or specialty formulations |

Potentially higher, if patents remain active |

| Hospital and institutional supply |

Competition moderated by procurement and shortage dynamics |

A generic applicant challenging a combination product may still face patents covering the non-HCTZ active ingredient, the ratio of ingredients, manufacturing processes, or a particular formulation. Those rights do not restore exclusivity to HCTZ itself.

What formulations are protected by hydrochlorothiazide patents?

The principal formulations are conventional immediate-release oral tablets. These products have limited differentiation and generally do not support durable premium pricing.

Potentially protectable formulation features include:

- Specific active-ingredient ratios in fixed-dose combinations.

- Modified-release delivery.

- Excipient systems.

- Improved stability or dissolution profiles.

- Taste-masking or alternative dosage forms.

- Combination products designed to manage potassium balance.

- Formulations addressing adherence or dosing frequency.

In practice, the strongest remaining formulation positions are usually attached to a broader branded product strategy, not to hydrochlorothiazide alone. A company seeking commercial protection would need a differentiated formulation, a clinically meaningful benefit, or a combination with a less commoditized active ingredient.

How does hydrochlorothiazide compare with chlorthalidone and indapamide?

Hydrochlorothiazide competes with other thiazide and thiazide-like diuretics, especially chlorthalidone and indapamide.

| Attribute |

Hydrochlorothiazide |

Chlorthalidone |

Indapamide |

| Market maturity |

Very mature |

Very mature |

Mature |

| Generic availability |

Extensive |

Extensive |

Extensive |

| Duration of action |

Shorter than chlorthalidone |

Longer |

Relatively long |

| Typical use |

Hypertension and combinations |

Hypertension, often once daily |

Hypertension |

| Brand pricing power |

Minimal |

Minimal |

Minimal to limited |

| Guideline position |

First-line option |

Often favored where longer duration is desired |

Used in selected patients |

| Commercial differentiation |

Low |

Low |

Low to moderate |

Some clinical guidelines and specialists favor chlorthalidone because of its longer duration and outcome data. That preference can reduce HCTZ demand in certain hypertension populations. HCTZ retains an important position because it is widely embedded in fixed-dose ARB and ACE inhibitor products, familiar to prescribers, and inexpensive.

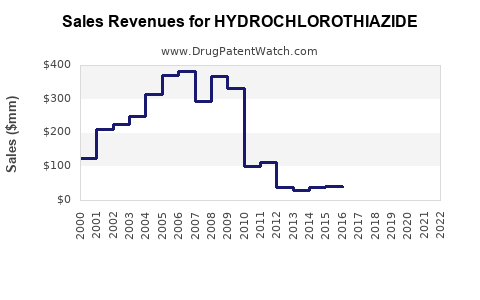

What is the financial trajectory for hydrochlorothiazide?

The financial trajectory is best characterized as stable-to-declining in volume-adjusted revenue, with periodic price volatility caused by supply conditions.

Revenue drivers

- Large installed base of chronic hypertension patients.

- Continued use in fixed-dose combinations.

- Low acquisition cost for payers.

- Broad generic formulary coverage.

- Use in primary care and institutional settings.

- Demand for low-cost cardiovascular therapy in emerging markets.

Revenue constraints

- Near-total generic substitution.

- Lack of exclusivity.

- Limited clinical differentiation.

- Reimbursement pressure.

- Multiple competing manufacturers.

- Substitution by chlorthalidone, indapamide, ACE inhibitors, ARBs, calcium channel blockers, and newer antihypertensive approaches.

- Low per-tablet revenue.

For manufacturers, HCTZ is generally a scale and portfolio product rather than a growth asset. Profitability depends on manufacturing efficiency, procurement discipline, and the ability to bundle HCTZ with other products. Standalone tablets can remain commercially useful when produced at low cost, but they offer little strategic pricing power.

Revenue exposure by product type

| Product type |

Financial importance |

| Standalone HCTZ tablets |

Low margin, high volume |

| Branded HCTZ combinations |

Historically meaningful, now largely eroded by generic entry |

| Generic fixed-dose combinations |

More commercially attractive than standalone tablets |

| Hospital supply contracts |

Volume-driven and price-sensitive |

| International markets |

Important in aggregate, with variable pricing and regulation |

| API sales |

Dependent on scale, quality compliance, and supply reliability |

Exact global revenue estimates are difficult to interpret because many commercial datasets attribute combination-product revenue to the finished product or brand rather than allocating revenue to the HCTZ component.

What is the manufacturing and intellectual-property risk?

Manufacturing risk is more important than patent risk. HCTZ is an established small molecule with conventional tablet technology, so the main barriers are regulatory compliance and cost control.

Key risks include:

- API contamination or impurity events.

- FDA warning letters or manufacturing restrictions.

- Loss of an approved manufacturing site.

- Raw-material concentration in particular regions.

- Product recalls.

- Dissolution or content-uniformity failures.

- Shortages caused by low-margin economics.

- Difficulty maintaining supply at older generic prices.

A manufacturer with a low-cost, compliant supply chain can compete effectively. A manufacturer with high overhead or unstable API sourcing may exit even when demand remains strong.

What litigation and settlement issues affect hydrochlorothiazide?

There is no single active litigation campaign defining the HCTZ market. Historical litigation has generally involved branded combination products and patents covering particular formulations or combinations.

Potential litigation categories include:

- Paragraph IV challenges to listed patents.

- ANDA litigation involving ARB/HCTZ or ACE inhibitor/HCTZ products.

- Patent disputes over dosage ratios or extended-release formulations.

- Product-liability claims involving electrolyte disorders, renal effects, or skin-cancer labeling.

- Antitrust or pricing claims involving generic supply markets.

Settlement agreements in this category typically concern the timing of generic entry for a specific branded combination. They do not create broad exclusivity for hydrochlorothiazide.

What generic launch scenarios exist for hydrochlorothiazide?

For standalone HCTZ, the generic launch phase has already occurred. Future market events are more likely to involve supplier entry, exit, shortage-driven price movements, or changes in combination-product competition.

| Scenario |

Expected market effect |

| New generic supplier enters |

Lower prices and greater supply redundancy |

| Major supplier exits |

Temporary price increases or shortages |

| Branded combination loses remaining patent protection |

Rapid generic substitution |

| Guideline shift toward chlorthalidone |

Lower HCTZ share in selected patients |

| Greater use of single-pill combinations |

Supports HCTZ combination volume |

| New safety concern |

Potential prescribing and labeling pressure |

| Manufacturing disruption |

Short-term price and availability volatility |

The most credible upside case is not a patent-driven price expansion. It is improved economics in a combination product, supply-constrained market, or differentiated formulation.

What is the geographic coverage of hydrochlorothiazide?

HCTZ is sold widely across the United States, Europe, Asia-Pacific, Latin America, and other regulated and emerging pharmaceutical markets. Regulatory status, available strengths, naming conventions, reimbursement, and combination-product prevalence vary by country.

The United States has extensive generic penetration and strong pharmacy-benefit substitution. European markets also have high generic use, although some countries favor indapamide or chlorthalidone more heavily. Emerging markets may have stronger volume growth because of expanding diagnosis and treatment of hypertension, but pricing is generally lower and local manufacturing competition is intense.

Key Takeaways

- Hydrochlorothiazide is a mature generic diuretic with no meaningful standalone patent exclusivity.

- Its commercial value comes mainly from prescription volume and fixed-dose combination products.

- Generic competition has compressed prices and shifted competition toward manufacturing cost, quality, and supply reliability.

- Orange Book analysis must be performed at the specific product and application level, especially for combination products.

- Paragraph IV litigation is primarily relevant to branded HCTZ combinations, not the basic active ingredient.

- Chlorthalidone and indapamide create clinical and commercial competition, particularly where longer duration is preferred.

- Financial growth is unlikely for standalone HCTZ. The stronger commercial opportunities are in combinations, emerging markets, and supply-constrained channels.

- Manufacturing and regulatory-compliance risk now matter more than patent risk.

FAQs

Does hydrochlorothiazide still have patent protection?

No meaningful patent protection remains for hydrochlorothiazide as a standalone active ingredient. Product-specific patents may apply to certain combination or specialty formulations.

Is hydrochlorothiazide an FDA-approved generic drug?

Yes. FDA-approved generic hydrochlorothiazide tablets are widely available in multiple strengths, and the ingredient is also approved in numerous combination products.[3]

Can a company obtain new patents on hydrochlorothiazide?

A new patent could potentially cover a novel formulation, combination, manufacturing process, or method of use if statutory patentability requirements are met. A patent on the old active ingredient itself would not be available.

Is hydrochlorothiazide a good pharmaceutical licensing asset?

Standalone HCTZ has limited licensing value. A combination product with clinical differentiation, improved adherence, or a proprietary delivery system may have greater value than the active ingredient alone.

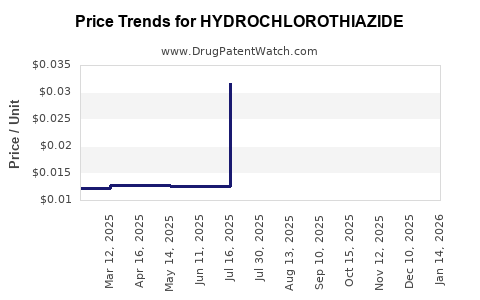

Why can hydrochlorothiazide prices rise despite generic competition?

Prices can increase temporarily when manufacturers exit, API supply is disrupted, production sites face regulatory restrictions, or wholesalers experience shortages. These changes reflect supply conditions rather than restored patent exclusivity.

References

-

U.S. Food and Drug Administration. (2024). Hydrochlorothiazide prescribing information. FDA-approved product labeling.

-

Whelton, P. K., Carey, R. M., Aronow, W. S., et al. (2018). 2017 ACC/AHA/AAPA/ABC/ACPM/AGS/APhA/ASH/ASPC/NMA/PCNA guideline for the prevention, detection, evaluation, and management of high blood pressure in adults. Hypertension, 71(6), e13-e115.

-

U.S. Food and Drug Administration. (2024). Drugs@FDA and abbreviated new drug application records for hydrochlorothiazide products. FDA.

-

U.S. Food and Drug Administration. (2020). FDA approves label changes to hydrochlorothiazide to describe small risk of non-melanoma skin cancer. FDA Drug Safety Communication.

-

U.S. Food and Drug Administration. (2024). Approved drug products with therapeutic equivalence evaluations: Orange Book. FDA.

-

U.S. Congress. (1984). Drug Price Competition and Patent Term Restoration Act of 1984, Pub. L. No. 98-417.