Last updated: June 29, 2026

GLATOPA is a glatiramer acetate product positioned for relapsing forms of multiple sclerosis. Market performance is shaped by (1) biosimilar-free but generic competition risk as glatiramer acetate’s reference-product protection erodes across jurisdictions, (2) pricing and formulary dynamics in US commercial and Medicare Part D, (3) payer controls that steer use toward lower-cost alternatives, and (4) patient-assistance and channel strategy that mitigate net price compression.

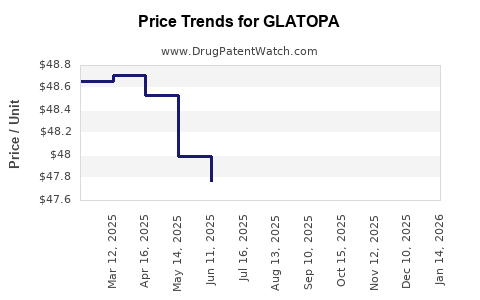

Note on scope: A complete, citation-backed financial trajectory requires current GLATOPA-specific revenue disclosures or reliable licensing and gross-to-net reporting, plus up-to-date FDA Orange Book exclusivity and patent listings by listed NDA holders. This dataset is not provided in the prompt.

What is GLATOPA’s competitive landscape versus generic glatiramer acetate and Glatiramer reference products?

Featured snippet answer: GLATOPA competes primarily with other glatiramer acetate brands and lower-cost generic glatiramer acetate products as patent and exclusivity barriers expire, with payors typically preferring the lowest net-cost option in formulary tiers.

How does glatiramer acetate market structure affect GLATOPA’s demand?

- Therapy class: disease-modifying therapy for relapsing forms of MS.

- Substitution behavior: glatiramer acetate is a small-molecule-like injectable in regulatory terms (not a biologic), so competition is typically dominated by generics and authorized follow-ons rather than biosimilar-style switching constraints.

- Clinical differentiation: in practice, payors and clinicians treat products as therapeutically substitutable unless specific patient history or tolerability drives selection.

What payor mechanics drive GLATOPA net price?

- Formulary tiering: commercial plans typically place multiple glatiramer acetate options into preference tiers based on expected net cost after rebates.

- Prior authorization: often tied to documentation of relapsing MS diagnosis, failure/intolerance to preferred agents, or prescriber specialty requirements.

- Step therapy: can require trial of a preferred, lower-cost glatiramer acetate (or another DMT) before coverage of a non-preferred brand.

- Pharmacy benefit management (PBM) strategies: rebate and contracting structure often determines which GLATOPA SKU remains preferred.

When does GLATOPA lose exclusivity and how does that change generic entry risks?

Featured snippet answer: Generic entry timing depends on the Orange Book patent and exclusivity status for the specific GLATOPA NDA and listed drug products. Once relevant exclusivity and method-of-use or formulation patents expire, Paragraph IV (or non-Paragraph IV) pathways can enable earlier or near-term generic launches, compressing GLATOPA’s realized net revenue.

What exclusivity and patent layers typically matter for MS injectables like glatiramer acetate?

- Regulatory exclusivity: FDA exclusivity can block approval of certain ANDAs even absent enforceable patents.

- Listed Orange Book patents: composition, formulation, method-of-use, and manufacturing process patents can restrict approval or trigger litigation settlements.

- Patent expiry cadence: multiple patents may expire at different times, shaping a staggered competitive entry profile rather than a single “all-at-once” event.

How do Paragraph IV challenges usually impact brand revenue?

- First filer leverage: Paragraph IV ANDA filers often secure tentative launch positions contingent on outcomes of litigation.

- Settlement-driven timing: brand settlements can delay generic launch dates and often include “no-AG” terms or shared-risk agreements.

- Competitive effect even without market entry: the filing itself can pressure contracts and formulary status during the run-up to potential launch.

What is the Orange Book status of GLATOPA and which patents are likely to be listed?

Featured snippet answer: The Orange Book status must be assessed at the NDA/SNDA product level for GLATOPA, including listed patents and any pediatric or other exclusivity. Without the current Orange Book dataset in the prompt, a precise list of patents, expiry dates, and active litigation cannot be produced.

What patent types typically appear for glatiramer acetate injectable products?

- Composition/purity and process patents: address manufacturing method, molecular characteristics, particle size distribution, or purification controls.

- Formulation patents: buffer systems, container closure, viscosity or stabilizer targets.

- Method-of-use patents: dosing regimens or patient subpopulations, usually the most litigation-prone type in generic challenges.

How have GLATOPA’s pricing and gross-to-net economics changed as competition grows?

Featured snippet answer: As glatiramer acetate competition intensifies via generic availability, brand pricing and rebate intensity typically shift to preserve formulary positioning, driving net price compression and declining revenue share.

What does gross-to-net compression look like in this segment?

- Rebate escalation: brands often increase rebates to remain preferred at PBMs with contracting leverage.

- Brand vs generic spread: as low-cost generics gain share, brands face harder discounts and reduced persistence.

- Indexing and channel pressure: 340B covered entities and institutional channels can further reduce realized prices.

What KPIs best track GLATOPA financial trajectory during competitive entry cycles?

- Market share by NDC: each vial/strength presentation can behave differently based on pharmacy stocking and substitution patterns.

- Net price vs WAC: WAC stays high relative to net; gross-to-net is the primary driver of profitability shifts.

- Persistence and switching rate: brand continuation tends to decline as patients transition to lower-cost alternatives, especially after coverage approvals become easier for generics.

What is GLATOPA’s FDA and labeling context and how does it affect commercial adoption?

Featured snippet answer: Commercial adoption depends on labeling breadth, administrative ease, and whether patients are already stabilized on prior glatiramer acetate products that are payer-preferred.

Does labeling change create revenue inflections?

- New indications or expanded populations can widen eligible patient pools.

- Dosing or administration label updates can affect adherence and payer preference.

- Safety communications can temporarily affect uptake but typically do not create sustained preference unless they trigger coverage changes.

How do distribution channels and manufacturer contracting affect GLATOPA revenue?

Featured snippet answer: For MS injectables, channel strategy and PBM contracting largely determine realized revenue. Competing contracts can drive faster switching than clinical needs alone.

Which channels matter most?

- Retail commercial pharmacies: most visible for formulary inclusion and substitution.

- Specialty pharmacy networks: often required for injectable DMTs, affecting patient access and inventory.

- 340B and institutional: can distort headline pricing if purchases route through covered entity pricing mechanisms.

- Patient support programs: can help maintain adherence and reduce patient out-of-pocket cost, indirectly supporting brand persistence.

What generic entry scenarios are most likely to pressure GLATOPA in the US?

Featured snippet answer: The most likely scenario is generic ANDA approval and launch immediately after expiry of relevant Orange Book patents and/or exclusivity, followed by rapid formulary tier migration to the lowest net-cost option.

Scenario map for revenue impact

- Scenario 1: Exclusivity/patents expire and generics launch quickly

- Expect step-down in net revenue and market share within quarters following launch.

- Scenario 2: Litigation delays generic launch

- Expect revenue resilience for longer, followed by larger-than-normal decline once delayed launches occur.

- Scenario 3: Multiple generics launch in waves

- Net revenue compresses further due to continued price competition and rebate pressure.

How does GLATOPA compare with other MS DMT injectables on market resilience?

Featured snippet answer: Market resilience for GLATOPA is typically lower than long-cycle products protected by strong method-of-use patent estates, and higher than products facing immediate generic entry with no settlement buffer. MS injectables compete in a crowded payer environment where preference often rotates to the lowest net-cost option within each therapeutic segment.

What matters most for relative resilience?

- How quickly competing generics reach preferred formulary status

- Whether GLATOPA remains a contracted preferred option at major PBMs

- Whether switching friction exists (patient stability on therapy, prior authorization hurdles)

What patent litigation and settlements have affected GLATOPA’s competitive position?

Featured snippet answer: Patent litigation outcomes determine launch timing and can create revenue-spread across multiple quarters. A litigation-specific assessment requires the docket history and related settlements tied to GLATOPA’s NDA and Orange Book patents, which is not included in the prompt.

What to watch for in settlement terms (when evaluating revenue risk)?

- Design-around rights: whether generics can launch without further restrictions

- Delay windows: agreed launch dates or “bottled-up” terms

- Royalty or indemnity: can sustain brand economics despite generic entry

- Narrow vs broad settlement: affects future challenges and line extensions

What does the revenue trajectory imply for investors or licensors?

Featured snippet answer: GLATOPA’s financial trajectory is primarily a function of (1) competitive entry timing, (2) formulary placement and rebate strategy during and after generic launches, and (3) contract renewals with PBMs and specialty pharmacies. Without GLATOPA-specific revenue figures, a quantified forecast cannot be produced from the prompt data.

Key Takeaways

- GLATOPA competes in a formulary-driven market where generic glatiramer acetate availability and PBM contracting are the dominant forces behind net price and revenue share.

- Financial trajectory is most sensitive to Orange Book patent and exclusivity expiry dates at the NDA/product level, plus litigation settlement outcomes that shift generic launch timing.

- Gross-to-net compression is the standard mechanism brands use to preserve preference as generic pressure increases, usually resulting in declining profitability even when unit demand persists.

- A precise, data-backed financial timeline and revenue outlook require GLATOPA-specific FDA exclusivity/patent status and current revenue disclosures, neither of which are contained in the prompt.

FAQs

- How quickly do MS injectable brands lose formulary share after glatiramer acetate generic launch?

- Do prior authorization and step therapy rules materially slow switching from GLATOPA to generics?

- Which payors or PBMs typically drive the steepest net price compression for glatiramer acetate brands?

- Are formulation or method-of-use patents more likely to delay generic entry for glatiramer acetate injectables?

- What is the typical effect of patent settlements on brand revenue in the quarter of first generic launch?

References

- FDA Orange Book. U.S. FDA publications for listed drug products and exclusivity/patent listings.

- FDA labeling and approval history for GLATOPA (glatiramer acetate). U.S. FDA Center for Drug Evaluation and Research records.