Last updated: June 16, 2026

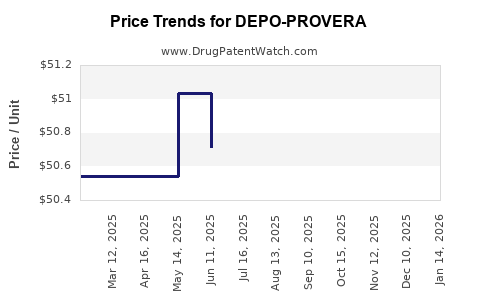

Executive summary: DEPO-PROVERA (medroxyprogesterone acetate, MPA) has remained a long-running, high-volume injectable under broad generics competition in multiple geographies. The market’s financial trajectory is shaped less by near-term patent exclusivity and more by (1) cyclic demand tied to contraception and women’s health care delivery settings, (2) reimbursement and payer formulary positioning, (3) substitution behavior toward lower-cost MPA generics, and (4) inventory and sourcing stability across manufacturers. For the US specifically, DEPO-PROVERA faces ongoing generic substitution risk because the product’s core market advantage is formulation and historical brand position rather than sustained legal exclusivity.

What are the latest market dynamics for DEPO-PROVERA (medroxyprogesterone acetate) by indication?

DEPO-PROVERA is used primarily for contraception and secondary indications including treatment of endometriosis-related conditions and certain gynecologic uses (depending on local labeling). Demand is driven by adherence to scheduled injections, clinic administering capacity, and payer coverage policies for contraceptives.

How do contraception category trends affect DEPO-PROVERA volumes?

Key dynamics typically affecting MPA injection sales include:

- Switch intensity between injectables (3-month depot) and alternatives such as intrauterine devices (IUDs) and implants.

- Patient preference shifts toward “set-and-forget” long-acting methods when cost-sharing favors them.

- Local network contracts that can steer dispensing toward specific NDCs or specific injectable SKUs used by high-volume clinics.

How do payer and PBM reimbursement policies affect DEPO-PROVERA pricing and access?

For legacy injectables under generics pressure, payer dynamics usually determine net price more than WAC:

- Formulary tier placement for depot medroxyprogesterone products is a major determinant of covered utilization.

- States and national programs that negotiate contraceptive supply influence which branded vs generic products are stocked by clinics.

- Coinsurance and prior authorization rules can reduce initiation or continuation rates, especially when patients are forced to change products mid-cycle.

What is the competitive landscape for injectable progestins and how does it affect DEPO-PROVERA?

The competitive set includes:

- Generic and authorized-generic versions of medroxyprogesterone acetate injectable products.

- Alternative long-acting contraception (IUDs, implants) which can trade off volume even when DEPO-PROVERA remains the lowest “clinic-administered” injectable option in some settings.

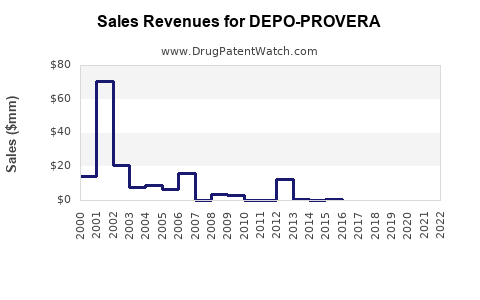

How has DEPO-PROVERA’s financial trajectory evolved since generic entry risk increased?

DEPO-PROVERA’s commercial trajectory is generally consistent with a mature branded legacy drug:

- Revenue is sustained but compressed versus pre-generic periods due to substitution and channel discounting.

- Net sales become heavily dependent on brand retention in reimbursement channels and where prescriber habits lock into clinic-administered SKUs.

- Any growth tends to be incremental and tied to population-level contraception needs, not to unit-price expansion.

What KPIs typically explain DEPO-PROVERA revenue performance in mature markets?

- Prescription starts and continuation through scheduled dosing intervals.

- Clinic buy-through rates and wholesaler inventory turns.

- Net price after rebates, patient assistance effects, and payer contracting.

What role do inventory and supply stability play in DEPO-PROVERA financial outcomes?

For injectable depots, supply constraints can cause temporary demand transfer between NDCs and manufacturers. In mature markets, revenue volatility often reflects:

- Manufacturer lot release cadence.

- Distribution disruptions that force clinics to use alternative equivalent NDCs.

When do DEPO-PROVERA exclusivity and key patent events end, and how does that impact sales?

DEPO-PROVERA’s market is not typically characterized by a single dominant modern “exclusivity wall” that blocks generic competition. The practical implication is that sales are already exposed to substitution dynamics rather than protected by a long, clean exclusivity timeline.

What exclusivity typically mattered historically for DEPO-PROVERA?

For legacy injectable progestins, brand protection historically has depended on:

- Periods of regulatory exclusivity related to original approvals and/or line extensions, plus

- Patent coverage that may have expired well before current market conditions in many regions.

How does the end of patent protection affect net price and volume?

Once robust generic competition is active:

- Volume usually shifts toward the lowest net-cost NDCs within each payer’s formulary.

- Brand revenue can remain stable if the brand retains certain contracts, but overall market economics tilt toward generic pricing.

What is the Orange Book status of DEPO-PROVERA, and which patents are most relevant to generic entry risks?

DEPO-PROVERA’s core active ingredient is medroxyprogesterone acetate (MPA) with multiple approved injectable versions. In the US market, generic entry risk is driven by whether any listed patents still restrict Abbreviated New Drug Application (ANDA) approvals.

What does Orange Book listing generally imply for DEPO-PROVERA competition?

- If relevant patents are expired or do not block approval, generics can compete on price and contracting.

- If any formulation or method-of-use patents remain listed and unexpired, they can delay specific ANDA approvals or require Paragraph IV litigation.

How should investors or licensors interpret Orange Book coverage for a mature depot product?

For mature injectables, the Orange Book estate often becomes fragmented across:

- Formulation changes (not always relevant to generic interchangeability),

- Device or delivery systems (if any),

- Specific labeled indications (method-of-use).

For DEPO-PROVERA, the practical commercial outcome is usually dominated by substitution after the last meaningful blocking patents expire.

Which companies compete with DEPO-PROVERA and what is the typical pricing and contracting pattern?

The DEPO-PROVERA market structure typically includes:

- The branded manufacturer historically holding the reference product,

- Multiple generic manufacturers offering AB-rated equivalents,

- Authorized generics in some channels depending on contract structures.

How do generics typically win in depot medroxyprogesterone?

- By placing the lowest net-cost product on formularies.

- By offering clinic-level contracting that reduces administrative switching.

- By aligning with wholesaler inventory availability.

What is the impact of biosimilar-type dynamics on DEPO-PROVERA?

DEPO-PROVERA is a small-molecule hormone, so biosimilar frameworks are not directly relevant. The competitive mechanism is generic substitution, not biosimilar interchangeability.

What patent litigation affects DEPO-PROVERA, and how does it influence timing of generic launches?

For older depot contraceptives, most litigation activity, where it occurs, tends to be around:

- Whether certain patents are valid/enforceable,

- Whether specific ANDAs satisfy the legal and regulatory requirements for approval,

- Whether settlements restrict launch dates for certain applicants.

How does Paragraph IV strategy change generic launch timing?

When a generic files a Paragraph IV ANDA, litigation can result in:

- Automatic stays under US Hatch-Waxman rules (if applicable),

- Carve-outs or negotiated settlement terms,

- Launch timing tied to court outcomes or settlement milestones.

In mature products like DEPO-PROVERA, the financial impact typically shows up as incremental share movements rather than step-function revenue recoveries for the brand.

What formulations and administration-related IP exists for DEPO-PROVERA, and what barriers do they create for competitors?

Depot MPA is an injectable suspension, so competitive barriers usually relate to:

- Process and particle characteristics that affect suspension properties,

- Stability and shelf-life within approved parameters,

- Labeling and injection instructions for safe use.

Do formulation differences materially change interchangeability?

For AB-rated generics, substitution is typically permitted when products are pharmaceutically equivalent. Barriers are usually legal or supply-based, not performance-based.

How does DEPO-PROVERA compare commercially with other contraceptive injectables and long-acting methods?

In most payer landscapes:

- IUDs and implants can take share due to adherence advantages and total cost-of-care arguments where reimbursement is favorable.

- Injectables remain competitive where clinic-administered contraception is preferred or where patients prefer an every-3-month visit cadence.

Where does DEPO-PROVERA tend to outperform?

- Settings with established depot workflows.

- Populations where injection scheduling is already embedded in care pathways.

- Low-cost procurement environments where generics of depot MPA are favored.

Where does DEPO-PROVERA tend to underperform?

- Practices that shift to IUD/implant initiation models.

- Regions where payer programs strongly incentivize long-acting reversible contraception beyond injectables.

Commercial outlook: what revenue and growth risks matter most for DEPO-PROVERA going forward?

The main forward-looking risks are structural rather than event-driven:

- Further price erosion as additional generic SKUs compete.

- Contracting and reimbursement shifts that favor alternative LARC methods.

- Utilization changes driven by public health funding cycles and payer rule updates.

- Supply and distribution dynamics across multiple generic manufacturers.

What upside scenarios could still move DEPO-PROVERA revenue?

- Improved contracting that preserves a meaningful branded share.

- Payer coverage expansions for depot injectables relative to other LARC methods.

- Increased continuation adherence reducing discontinuation-driven demand loss.

What downside scenarios most likely compress revenue?

- Faster formulary migration toward cheaper generic NDCs and away from branded reference product.

- Sustained patient and provider preference drift toward implants and IUDs.

- Distribution issues that push administration to alternative equivalent products.

Key Takeaways

- DEPO-PROVERA’s market is driven by long-established contraception demand mechanics, not by near-term, dominant exclusivity protection.

- Financial performance in mature markets is primarily shaped by payer contracting, net price compression, and substitution by medroxyprogesterone acetate generics.

- Competitive pressure from alternative long-acting contraception can erode injectable share even when depot MPA remains clinically used.

- Future revenue growth is likely incremental and depends on formulary position, supply continuity, and maintenance of clinic-level channel preferences rather than legal exclusivity milestones.

FAQs

1) What are the biggest determinants of DEPO-PROVERA net sales versus list price?

Payer rebates, formulary tier placement, wholesaler contracting, and generic NDC mix within covered channels.

2) Does DEPO-PROVERA face biosimilar competition?

No. It is a small-molecule hormone with generic substitution dynamics, not biologic biosimilar pathways.

3) How do clinic administration workflows influence DEPO-PROVERA market share?

Injection scheduling adherence and established buy-through practices can lock usage into specific NDCs, slowing or accelerating substitution.

4) What generic launch risks matter most for depot medroxyprogesterone?

Whether any remaining Orange Book listed patents still block approval and whether Paragraph IV litigation triggers launch delays or settlement-based entry restrictions.

5) How does alternative contraception (IUD/implant) typically impact DEPO-PROVERA demand?

It can shift initiation patterns away from injectables, especially where reimbursement and patient counseling favor longer-dwell LARC methods.

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. (US).

- FDA. Drug Approval Reports and labeling information for medroxyprogesterone acetate injectable products. (US).

- FDA. Hatch-Waxman Act and ANDA approval framework overview materials. (US).

- FDA. Drug shortage and discontinuation communications relevant to injectable products (US). (US).