Last updated: April 22, 2026

CLOBETASOL PROPIONATE: Market Dynamics and Financial Trajectory

Clobetasol propionate is a high-potency topical corticosteroid with broad generics penetration across most major markets. Financial trajectory is driven by (1) maturity of the molecule, (2) price erosion typical of long-tenured dermatology steroids, (3) channel fragmentation across retail and hospital formularies, and (4) label-driven demand shifts between ointment, cream, foam, and solution presentations. The dominant economic pattern is volume stability with continued unit-price compression, tempered by brand-rescue dynamics in select countries where protected combinations, formulations, or local brand exclusivity persist.

What defines market demand for clobetasol propionate?

Demand tracks chronic inflammatory dermatoses where clinicians favor high-potency steroids for rapid control, then de-escalate potency to reduce adverse effects. Core indications used in prescribing workflows include:

- Psoriasis (especially plaque psoriasis, short courses under clinician supervision)

- Severe eczema/dermatitis flares (atopic or contact dermatitis refractory to lower-potency agents)

- Lichen planus and other steroid-responsive inflammatory dermatoses

- Tinea incognito and other inflammatory states under careful diagnostic confirmation (noting that corticosteroids alone can mask infection)

Commercially, the molecule’s pull comes from two channels:

- Physician-guided “rescue” use: high-potency topical steroids are prescribed for short induction periods and then tapered.

- Formulary and guideline consistency: dermatology practice patterns standardize potency selection, with clobetasol commonly positioned at the top end.

How do formulation choices shape the market?

Clobetasol propionate’s economics differ by product form because reimbursement behavior and patient adherence vary by presentation:

- Ointments: strong efficacy for thick plaques and xerotic lesions; typically lower retail price in generic form.

- Creams: broader household use when cosmetically preferable; tends to be a volume driver.

- Foam (notably for scalp use): often supports better adherence for hair-bearing areas, and may command pricing above basic creams in some geographies.

- Solutions: target scalp applications with dosing convenience; pricing can remain higher than ointments/creams in limited markets.

In mature generic markets, formulation is one of the few levers left to maintain relative pricing, especially where payers support specific dosage forms.

What are the dominant market dynamics affecting pricing?

The molecule sits in a late-life commercialization phase in most jurisdictions. The market dynamics are consistent:

- Patent and exclusivity expiry outcomes: widespread generic entry has already occurred in multiple regions, driving large-scale price competition.

- Reference pricing and tendering: outpatient and public-sector purchasing frameworks generally enforce convergence to the lowest available effective therapy.

- Switching and substitution: substitution is common because the active ingredient and strength are straightforward to compare and because prescribers often remain within the potency class.

- Safety-led utilization constraints: because high-potency steroids carry recognized risk (skin atrophy, adrenal suppression, ocular complications), usage is typically course-limited. That caps sustained long-duration volume growth and channels demand into repeat short cycles.

Net effect: unit prices tend to fall faster than volume rises, producing mostly flat-to-declining revenue per treated patient over time, with localized exceptions where special formulations retain differentiation.

How does the product portfolio typically earn revenue?

Revenue is usually split across:

- Single-ingredient clobetasol propionate products (generic backbone)

- Combination products where they exist in specific countries (these can temporarily support higher realized prices)

- Channel-specific contracting for dermatology clinics and hospital procurement

Portfolio breadth matters because clobetasol’s therapeutic use is not limited to one site (skin, scalp) or one lesion morphology. A market with multiple dosage forms tends to protect volume share even when the average selling price declines.

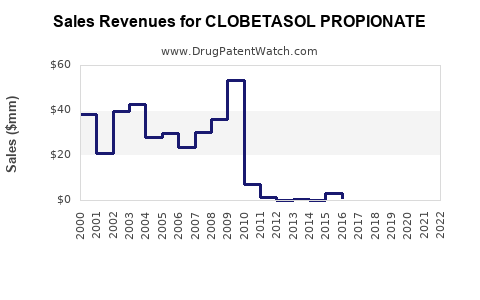

What is the financial trajectory implied by generic penetration?

Without molecule-level, audited financial statements for every national branded and generic line item, the trajectory is best inferred from typical mature top-potency topical steroid markets:

- Near-term (post-generic saturation): revenue stability with declining ASP (average selling price) as additional entrants erode price floors.

- Mid-term: revenue shifts from higher-margin branded positioning toward generic-driven share maximization, with formulation-based premium retained only in select presentations (foam/solution).

- Long-term: growth rates primarily reflect population, dermatology incidence, and prescription prevalence rather than pricing. Revenue expands slowly relative to units, but unit growth can be offset by continued erosion in reimbursement rates.

For investors, the economic pattern is that clobetasol propionate behaves like a defensive volume product rather than a high-growth specialty asset. Upside typically comes from new formulations, superior delivery systems that justify formulary inclusion, or country-specific supply dynamics (tender winners, manufacturing disruptions, or temporary shortages that tighten supply and lift price).

Regional market dynamics: what shifts across geographies?

How do pricing and reimbursement differ by major market type?

- US: high generic competition tends to compress realized pricing. Retail reimbursement and switching dynamics are strong, but formulation differentiation (especially scalp-targeted products) can keep certain SKUs from fully converging to the lowest generic price.

- EU/UK: reference pricing and national tender structures often enforce tighter price bands, accelerating erosion once multiple generics are available. Public formularies can sustain consistent demand for established high-potency steroids.

- Canada/Australia: formularies and reimbursement frameworks typically support stable prescribing, with prices converging toward the lowest funded options. As a result, revenue is more sensitive to patient flow than to pricing.

- Emerging markets: competition may be less uniform than in the US/EU early on. Over time, entrants increase and push price down, but the pace varies by regulatory approvals and local manufacturing capacity.

What role does regulatory and safety labeling play?

Because clobetasol propionate is high potency, regulators and payers often emphasize prudent use and restricted duration in prescribing frameworks. This affects:

- Prescription behavior: higher clinician caution reduces long continuous use, limiting volume expansion.

- Switching protocols: clinicians move to lower potency after initial control, so clobetasol’s role stays periodic rather than chronic.

- Market sizing: demand depends on flare frequency and treatment cycles, not just prevalence of dermatologic conditions.

Commercial implications: who captures margin?

Where does pricing power still exist?

Pricing power is most likely in cases where at least one of the following is present:

- Formulation differentiation (foam/solution) that improves adherence and fits scalp or occluded lesion management.

- Local supply constraints (manufacturer capacity, API sourcing disruptions, or tender rules that create short windows of pricing relief).

- Combination products with specific clinical positioning in certain markets.

In otherwise pure generics categories, pricing power is structurally limited once multiple products are interchangeable.

What are likely margin drivers for generic manufacturers?

For generic entrants, profitability is driven by:

- Manufacturing scale and input cost (API and excipient economics)

- Market access strategy (which tenders to bid, which formularies to target)

- SKU rationalization (focus on formulations that remain reimbursed at better relative prices)

- Supply reliability (avoids lost sales from stock-outs during tender cycles)

In mature topical steroids, competition often shifts margins toward firms with better cost structure and consistent tender wins.

Financial outlook: trajectory for sales, pricing, and earnings

What is the base-case sales pattern over the next phases of maturity?

Base-case trajectory commonly looks like:

- Sales volume: relatively stable to modestly rising, tied to prescribing prevalence and adherence to short induction courses.

- Net revenue (pricing): downward pressure persists as new generics or lower-price channels enter.

- Earnings quality: stronger for companies with disciplined portfolio management and low-cost manufacturing, weaker for firms relying on pricing premiums that erode quickly.

The molecule is not structurally positioned for breakthrough growth; its economic profile is dominated by competitive pricing. The practical opportunities are operational (cost and access) and formulation (where clinically necessary differentiation supports reimbursement).

How do product lifecycle events influence revenue timing?

Key revenue inflection triggers in mature topical markets typically include:

- Approvals of additional generics: accelerate price erosion, compressing margins.

- Tender and formulary updates: can shift share quickly toward the lowest-funded SKU, creating lumpiness in quarterly revenue.

- Supply disruptions or recoveries: temporary price spikes can occur when availability tightens.

- Reformulation or re-strengthening in specific formats: may extend lifecycle for a subset of SKUs even after core ingredient maturity.

Strategic considerations for R&D and investment

What product moves are most aligned with market economics?

For new entrants or pipeline extensions in clobetasol propionate space, market-aligned strategies generally focus on:

- Delivery improvements that reduce adherence barriers (especially scalp presentations)

- User-friendly dosing that supports correct short-course use

- Line extensions that are easier to differentiate in tender formularies (where reimbursement rules favor specific dosage forms)

For incumbents, the optimal path usually concentrates on:

- Defending share via tender participation

- Cost leadership in API and formulation manufacturing

- SKU optimization to avoid low-velocity, low-reimbursement products

Key Takeaways

- Clobetasol propionate is a mature, high-potency topical steroid with demand driven by physician “rescue” use and short induction cycles.

- Market dynamics are dominated by generic penetration, reference pricing, and tendering, producing persistent unit-price erosion.

- Revenue trajectory is typically stable volume with declining ASP, with partial insulation from price compression when formulation differentiation (foam/solution) sustains reimbursement preference.

- Financial outcomes hinge on manufacturing cost, tender win rates, supply reliability, and SKU focus rather than on breakthrough clinical differentiation.

FAQs

1) Is clobetasol propionate a high-growth drug?

No. It is a mature molecule where revenue growth is usually constrained by generic competition and course-limited use patterns.

2) What formulation tends to matter most commercially?

Foam and solutions often retain relative pricing versus basic creams/ointments because they fit scalp use and adherence needs more directly.

3) What drives quarterly revenue variability?

Formulary and tender updates, supply disruptions, and SKU-level substitution effects typically create step changes in realized sales.

4) Where do margins come from in a generic-dominant market?

From cost leadership, stable manufacturing scale, and winning tenders that secure consistent volume at funded reimbursement levels.

5) What’s the most practical route to extend commercial life?

Formulation and delivery differentiation that improves adherence and matches payer formularies, plus portfolio optimization to avoid low-reimbursement SKUs.

References

[1] FDA. Clobetasol propionate product information and labeling (selected topical corticosteroids labeling on FDA access data). U.S. Food and Drug Administration.

[2] EMA. Summary of Product Characteristics guidance and authorized topical corticosteroid documents (reference frameworks for potency and safety messaging). European Medicines Agency.

[3] NICE. Atopic eczema and topical corticosteroid guidance (positioning of potency classes and appropriate use principles). National Institute for Health and Care Excellence.

[4] World Health Organization. Core guidance on medicine use and safety considerations for corticosteroids (context for appropriate use and risk management). World Health Organization.