Last updated: April 24, 2026

Ciprofloxacin is a long-established, high-volume antibiotic whose market dynamics are dominated by (1) generic availability and price pressure, (2) usage discipline and stewardship-driven demand, and (3) periodic safety-communication cycles that shift prescribing patterns. Financially, the commercial trajectory is defined by steady volume offsetting declining net price, with brand-level monetization largely replaced by generic economics.

What is the market structure for ciprofloxacin?

Ciprofloxacin sits in the systemic antibacterials category (fluoroquinolones). The commercial landscape is typical of mature molecules that have transitioned to broad generic coverage.

Competitive form

- Generic tablets/suspensions/injectables dominate the market.

- Brand presence persists in limited geographies and segments (often tied to legacy supply, formulation advantages, or local brand contracts), but has been eclipsed in aggregate by generics.

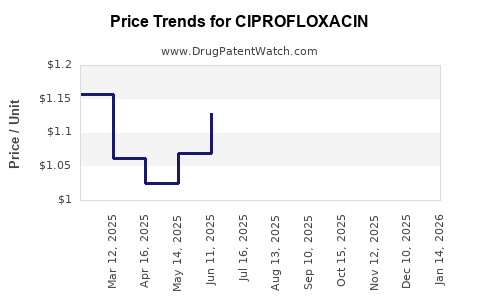

Pricing and reimbursement dynamics

- Net price declines are structural because multiple suppliers compete after generic entry.

- Wholesale and retail dynamics depend on:

- tendering and hospital formularies for injectable and oral inpatient use

- national health system reimbursement rules

- outpatient channel contracting and PBM dynamics in markets that use them

Manufacturing and supply dynamics

- Ciprofloxacin is chemically and operationally “mature” from a manufacturing standpoint, so supply can scale once regulatory and quality system requirements are met.

- Capacity additions and new generic launches increase SKU-level competition and compress margins.

How do stewardship and safety communications shape demand?

Demand for fluoroquinolones is not purely epidemiological. Ciprofloxacin prescribing responds to stewardship guidance and safety communications, which can affect both the breadth of indications used in practice and the site-of-care mix.

Stewardship and guideline effects

Key demand drivers include:

- shift toward narrow-spectrum alternatives when local resistance patterns support them

- restriction of fluoroquinolones in uncomplicated settings due to risk-benefit frameworks

- greater reliance on culture-directed therapy which can reduce empiric fluoroquinolone use

Safety and risk messaging effects

Major safety scrutiny around fluoroquinolones (class-wide) influences clinicians to:

- reserve for higher-risk cases or when alternatives are not suitable

- increase documentation and patient selection

- avoid in lower-acuity indications where other antibiotics are appropriate

These forces tend to produce volume stability with lower willingness to prescribe outside targeted scenarios.

What are the key demand segments by usage channel?

Ciprofloxacin is used across inpatient and outpatient settings, with demand split shaped by guideline-driven preference and local formulary behavior.

Inpatient and acute care

- Injectable formulations and oral equivalents capture segments where clinicians treat susceptible gram-negative infections.

- Hospital formulary placement is decisive because it determines default therapy access.

Outpatient and community care

- Oral formulations drive most chronic volume.

- Outpatient prescribing is more sensitive to safety messaging and guideline interpretation, especially for non-complicated indications.

Travel and “consumer” demand patterns

In some geographies, ciprofloxacin has historically benefited from empiric use in certain travel-related diarrheal settings. Over time, stewardship and updated clinical guidance have reduced broad empiricism, which generally limits upside.

How has ciprofloxacin’s financial trajectory evolved across the life cycle?

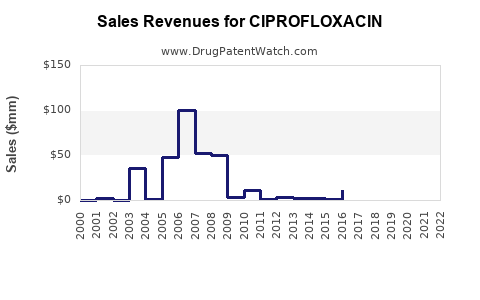

Ciprofloxacin entered the market as a branded product and later shifted to generic dominance. The financial trajectory therefore reflects classic maturity dynamics: declining branded revenue, stable-to-declining price, and persistent utilization in susceptible indications.

Revenue pattern: brand to generic

Typical life-cycle outcomes for molecules at this stage:

- Brand revenue largely stops being the primary commercial engine once generics take share.

- Industry revenue becomes a function of combined generic volume.

- Margin compression is persistent because multiple manufacturers compete on price.

Investment and profit pools

Profit pools shift from R&D-led innovation to:

- manufacturing cost advantage

- regulatory and quality execution

- supply reliability and contract wins

- litigation or exclusivity resolution (where applicable)

For investors and operators, the relevant financial levers become working capital discipline, tender competitiveness, and unit cost control rather than differentiated clinical marketing.

What does the competitive landscape imply for profitability?

Competition among generics creates predictable financial constraints.

Price pressure mechanisms

- Tender-driven pricing compresses unit margins for hospital supply.

- Retail and pharmacy contracting drives additional discounting.

- SKU fragmentation (strengths, dosage forms, package sizes) increases operational complexity and can reduce economies of scale.

Quality and compliance costs

Manufacturing-grade compliance, stability testing, and pharmacovigilance costs persist even when the product is mature. These costs reduce profitability for smaller or less efficient suppliers.

Net outcome

The market tends toward:

- stable volumes

- reduced price and margin per unit

- profitability concentrated among the most cost-competitive manufacturers and those with strong distribution and contracting access

How do generics and originator dynamics typically change the P&L?

Even without molecule-level financial disclosures by every market participant, the structure of a mature, generic-dominant antibiotic implies the P&L shape:

Revenue

- driven by volume (retention of prescribing patterns and susceptible infection incidence)

- constrained by dispersion of share across many suppliers

Cost

- anchored by COGS (API and formulation)

- plus compliance costs

- plus logistics and inventory management

Margins

- decline over time as more entrants compete

- stabilize only when supply consolidation or demand firmness offsets price erosion

What market dynamics can create periodic inflections?

Ciprofloxacin can see short-lived demand or pricing shifts from events such as:

- supply disruptions at API or finished-dose manufacturing sites

- tender repricing at the hospital and national formulary level

- resistance or outbreak patterns in specific regions

- new safety communications or label changes that influence prescribing

In mature markets, these inflections rarely create long-duration growth. They more often create short-term volume or price deviations.

How do resistance trends affect long-run demand?

Antibiotic resistance shapes the effective clinical utility of ciprofloxacin.

Resistance and prescribing

- higher local fluoroquinolone resistance tends to reduce use in empiric therapy

- culture confirmation can preserve use in targeted cases

Long-run implication

Resistance typically produces:

- a gradual reduction in broad-spectrum empiric usage

- a shift toward narrower, culture-directed use

- reduced growth rates even when total bacterial infection incidence stays stable

What financial trajectory best fits ciprofloxacin today?

The current trajectory aligns with “mature generic economics”:

- stable-to-slowly declining net unit value

- volume stability supported by ongoing clinical needs

- competitive margin pressure across most geographies

For a business plan, the practical read-through is that ciprofloxacin remains a cash-flow product but does not behave like a differentiated franchise. The upside case depends on operational differentiation (cost, access, supply continuity) and contract execution.

Key operational metrics to track for forecasting

A practical forecast for ciprofloxacin’s financial trajectory should follow a narrow set of market-facing indicators:

- Tender pricing and bid acceptance rates for hospital distribution

- Channel mix shifts (inpatient vs outpatient)

- Formulary status changes by geography

- Local resistance updates that affect empiric suitability

- Generic entry cadence (new applicants, new SKUs, package size changes)

- Supply continuity (any recurring shortages or API constraints)

These metrics connect directly to volume and net pricing, the two variables that define mature-molecule financial outcomes.

Regulatory and labeling context: what matters commercially?

Regulatory actions do not just change label text. They change prescribing behavior and procurement behavior.

Label and risk communication effects

- additional risk warnings reduce willingness to prescribe in lower-risk settings

- procurement committees may steer clinicians toward alternative agents

- prescriber confidence can shift toward agents with simpler risk communication profiles

Commercial implication

In a generic market, regulatory-driven prescribing changes tend to influence:

- the share of therapy among competing antibacterials

- the speed of uptake or erosion in specific indications

- tender outcomes and formulary preferences

Key Takeaways

- Ciprofloxacin is a mature, generic-dominant antibiotic where price pressure is structural and volume stability is the main offset.

- Demand is shaped by stewardship and fluoroquinolone safety communications, which tend to restrict broad empiric use and narrow the addressable prescribing base.

- The financial trajectory fits stable cash-flow economics rather than growth: net value declines over time, margins compress, and profitability concentrates in the most cost-competitive and contract-winning suppliers.

- Forecasting should track tender pricing, formulary status, resistance patterns, and supply continuity, since these drive both net price and utilization.

- Periodic inflections occur mainly from supply or policy shocks, not from sustained innovation-led expansion.

FAQs

-

Is ciprofloxacin’s market growth driven by new clinical differentiation?

No. The molecule is mature; the market is driven by utilization in susceptible indications and generic competitive pricing.

-

What factor most directly compresses ciprofloxacin margins?

Generic competition that drives tender and contract price erosion.

-

How do safety messages affect prescribing?

They typically shift ciprofloxacin toward more selective use, reducing broad empiric prescribing and changing the inpatient/outpatient mix.

-

Does antibiotic resistance always reduce ciprofloxacin use?

It tends to reduce empiric suitability, but culture-directed therapy can preserve use in confirmed susceptible cases.

-

What operational levers matter most for profitability in a generic market?

Cost position, supply reliability, and contracting performance in hospital and retail channels.

References (APA)

[1] U.S. Food and Drug Administration. (2016, June 21). FDA Drug Safety Communication: FDA updates warnings for fluoroquinolone antibiotics on risks of mental health and low blood sugar. https://www.fda.gov/drugs/drug-safety-and-availability

[2] U.S. Food and Drug Administration. (2018, December). Drug Safety and Availability: Fluoroquinolone antibiotics and risk of disabling side effects. https://www.fda.gov/drugs/drug-safety-and-availability/fluoroquinolone-antibiotics

[3] European Medicines Agency. (2018). PRAC recommendations on signals: Fluoroquinolone antibiotics and risk of disabling and potentially long-lasting side effects (class review). https://www.ema.europa.eu/ (document pages under PRAC referrals and recommendations)

[4] World Health Organization. (2014). Antimicrobial resistance: Global report on surveillance. https://www.who.int/publications/ (AMR surveillance reports)