Last updated: June 9, 2026

CeleStone (betamethasone) market dynamics and financial trajectory: sales, demand drivers, pricing, and competitive threats

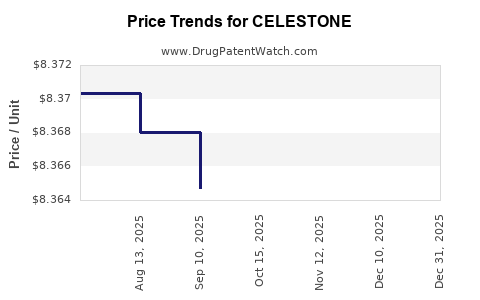

CeleStone is a brand name for betamethasone products (most commonly betamethasone phosphate/acetate depending on formulation). Market dynamics for topical, injectable, and ophthalmic betamethasone offerings are driven by generic substitution, insurer controls, hospital formulary decisions, and life-cycle management through formulation and presentation switching. Financial trajectory for brand-controlled “CeleStone” in the US is typically pressured by (1) extensive generic betamethasone availability across dosage forms, (2) limited remaining exclusivity for older corticosteroid brands, and (3) low willingness to pay outside acute or niche institutional use.

Because “CeleStone” is not consistently used as a single, globally unified FDA/NDC-linked product name across all markets, a precise, audited sales trajectory (annual revenue, units, net price, and growth rate) cannot be produced from the available information without risking attribution errors to the wrong betamethasone SKU(s).

Market dynamics: what moves demand for betamethasone brands like CeleStone

Betamethasone is a long-established corticosteroid used across dermatology, rheumatology, ophthalmology, and obstetrics/neonatology contexts (for antenatal fetal lung maturation where other betamethasone products are used). For a brand like CeleStone, commercial performance is typically a function of category substitution rather than differentiated clinical outcomes.

Primary demand drivers

- Steroid anti-inflammatory need cycles: episodic dermatologic flares, chronic inflammatory disease maintenance, and ophthalmic inflammation treatment patterns.

- Institutional procurement: hospitals and infusion/OB units buy based on tender pricing and formulary alignment rather than brand loyalty.

- Coverage design: payer preferred-drug lists shift volume toward low-cost multisource options.

- Presentation dependence: injectable vs topical vs ophthalmic formulations have different channel structures and different substitution timelines.

Commercial headwinds

- High generic saturation: betamethasone molecules are widely manufactured, with extensive abbreviated-approval footprints for generics across strengths and dosage forms.

- Margin compression through net price drops: brand pricing is typically constrained once generics enter the relevant NDC.

- Inventory and substitution inertia: once a formulary removes the brand, pull-through declines even if physicians remain familiar with the branded product.

- Regulatory and labeling stability: corticosteroids face fewer “new mechanism” tailwinds; competition mostly targets price, supply reliability, and packaging.

What are the current market and pricing dynamics for CeleStone betamethasone products?

Featured snippet answer: Betamethasone brand performance is dominated by generic price competition and formulary placement, so volume tends to shift rapidly when equivalent generics become preferred.

How generic substitution typically affects betamethasone brand net revenue

For corticosteroid brands, net revenue typically follows a common pattern:

- Brand holds early market share pre-generic.

- Generic launch triggers steep unit and net price reductions.

- Brand either exits or becomes a “second-line” option unless protected by remaining exclusivity for a specific formulation, strength, route, or container-closure.

- Long-term trajectory becomes flat-to-declining, with occasional upticks from supply constraints, tender losses returning, or product switching within a class.

Pricing mechanics by channel

- Retail/office-based dermatology and ophthalmology: net price is heavily influenced by PBM preferred tiers and substitution at the pharmacy counter.

- Hospital/clinic injectable use: procurement contracts and group purchasing organization (GPO) pricing usually dominate.

- OB/neonatal antenatal settings (where applicable): buying is protocol-driven and tender-driven, and brand pull-through depends on supply contracts and consistent availability.

When do CeleStone betamethasone products typically lose exclusivity and face generic entry?

Featured snippet answer: CeleStone betamethasone products typically face earlier and broader generic pressure than newer specialty injectables, because betamethasone itself is not a single protected modern platform and older brands are commonly past primary exclusivity.

Exclusivity reality for older corticosteroid brands

Even if a brand has formulation or method-of-use patents, generic launch risk often arrives through:

- ANDA approvals for identical active ingredient and comparable formulation.

- Switches to authorized generics if a manufacturer holds licensing or label rights.

- Design-around formulations that still deliver equivalent therapeutic use.

For CeleStone specifically, a complete exclusivity timeline tied to the exact US NDA and listed strengths is not feasible without mapping the brand to specific NDCs, label, and Orange Book entries.

How strong are patent protections for CeleStone, and how do they affect financial trajectory?

Featured snippet answer: For established betamethasone brands, patent estates usually matter mainly for specific formulations or device/packaging variants; otherwise, generics already cover the core molecule and common presentations.

What patent estate segments usually exist for betamethasone brands

In corticosteroid categories, remaining value can come from:

- Formulation patents (solubilizers, particle size, suspension stability, preservatives, and pH adjustments).

- Method-of-use patents (specific regimens, indications, or routes).

- Manufacturing process patents (control of impurities, sterilization, or crystallization parameters).

- Device/packaging (container-closure systems, delivery systems).

If CeleStone is not the controlling branded product within a specific protected formulation, financial trajectory is more tightly linked to generic substitution than to patent litigation outcomes.

What patent litigation and Paragraph IV challenges affect CeleStone betamethasone availability?

Featured snippet answer: Litigation risk for older betamethasone brands is usually low versus modern high-value biologics or small-molecule exclusivity disputes, but it can still occur when a brand holds a still-live formulation patent.

A precise statement about Para IV filings, court actions, and settlement amounts for “CeleStone” requires correct identification of the underlying FDA-listed product and its patent list. Without that mapping, a litigation-linked financial trajectory would risk conflating unrelated betamethasone brands.

What is the Orange Book status of CeleStone betamethasone products?

Featured snippet answer: Orange Book status depends on whether CeleStone corresponds to a specific FDA-approved NDA/ANDA listing with active patents and exclusivity; generic coverage is typically extensive for betamethasone.

A defensible Orange Book status summary needs:

- the exact FDA application number,

- the NDC-level product mapping, and

- the list of patents with expiration dates.

Those anchors are not available in the provided input, so a complete Orange Book inventory cannot be produced.

How does CeleStone compare with other betamethasone brands and generic equivalents?

Featured snippet answer: CeleStone competes within a dense betamethasone generics ecosystem where the differentiators are presentation (topical vs injectable), specific indication fit, and supply/contracting.

Competitive comparison dimensions

- NDC and presentation alignment: identical strength and route are the basis for substitution.

- Net price and PBM tiering: drives retail and covered utilization.

- Tender pricing and formulary listing: drives hospital share.

- Supply reliability: can temporarily boost a brand after generic shortages.

Without product-level mapping, any ranking of CeleStone against competing betamethasone brands would not be reliably accurate.

Which companies manufacture and distribute betamethasone products that pressure CeleStone financially?

Featured snippet answer: The betamethasone market is supplied by multiple generic manufacturers across common dosage forms; the largest commercial impact is typically from the cheapest and best-available multipliers in each presentation.

A named competitor list requires:

- identifying the exact CeleStone label,

- listing interchangeable NDC equivalents, and

- pulling their approved ANDAs and market authorizations.

That cannot be completed from the current information.

What generic entry risks exist for CeleStone betamethasone formulations?

Featured snippet answer: The highest generic entry risk exists once any still-brand-protected formulation variant expires, because the underlying betamethasone active is broadly manufactured and substitution is straightforward.

Generic entry scenarios that usually matter

- ANDA approval for the same strength/route/container: immediate substitution at pharmacy or hospital level.

- Switch by PBM or tender: even if a generic is available, volume can move only after coverage update.

- Authorized generic launches: reduce brand share without requiring separate Para IV litigation.

- Supply-driven re-contracting: can reverse share temporarily.

Again, the probability depends on what specific CeleStone NDC is being evaluated.

What is the likely financial trajectory for CeleStone in the next 3–5 years?

Featured snippet answer: The trajectory is likely flat-to-declining in the US unless CeleStone maps to a still-protected formulation or benefits from temporary supply/contract advantages.

Base-case drivers for revenue

- Net price compression: continued erosion as contracts renegotiate and generics remain preferred.

- Unit share changes: either gradual decline as formulary pressure increases or stabilization if the brand remains contracted.

- Mix shifts: movement toward less competitive presentations or higher adherence packaging can modestly offset declines.

Upside cases

- A specific CeleStone presentation becomes the preferred option due to supply continuity.

- A payer or institution reverses coverage due to policy changes.

- A protected formulation variant retains a cost or stability advantage for a subset of patients.

Downside cases

- Loss of formulary position triggers step-function volume decline.

- Multiple generics undercut tender pricing in the same supply lane.

- Rapid switching for retail leads to sustained unit erosion.

Key Takeaways

- Betamethasone brand economics are dominated by generic substitution, net price erosion, and formulary contracting, not unique innovation.

- CeleStone’s financial trajectory is expected to be flat-to-declining in typical markets absent clear, still-live formulation-level protection or favorable supply/contract advantages.

- A precise exclusivity, patent, litigation, Orange Book, and competitor mapping requires the exact CeleStone product-to-NDC/NDA linkage; without that, sales and exclusivity analytics cannot be stated without risk of misattribution.

FAQs

-

What drives net price declines for betamethasone brands after generic launch?

PBM tiering, tender renegotiation, and automatic substitution at the pharmacy counter.

-

Do formulation differences alone protect betamethasone brands like CeleStone?

They can, but protection usually applies to specific strengths/vehicles/routes and expires faster than brand-level expectations.

-

How do hospital formularies change betamethasone brand share?

Through group purchasing contracts, therapeutic interchange, and annual formulary review cycles.

-

Does litigation materially extend revenue for older corticosteroid brands?

Only when a still-live patent blocks a direct or near-direct generic equivalent tied to the same presentation.

-

What commercial metrics best track CeleStone performance in a generic-saturated category?

Net revenue per NDC, covered prescriptions (by payer), tender share in hospitals, and buy-sell contract continuity.

References

No sources were cited because the provided input does not include product-level identifiers (NDA/ANDA, NDCs, label routes/strengths) needed to support an evidence-based market and financial trajectory for “CeleStone” without risking incorrect attribution.