Last updated: April 22, 2026

What products and therapeutic use drive the CALCIUM ACETATE market?

Calcium acetate is a calcium-based phosphate binder used primarily in chronic kidney disease (CKD), where it controls serum phosphate levels to reduce complications of CKD-mineral and bone disorder (CKD-MBD). Its market is shaped by:

- CKD prevalence and dialysis penetration (core demand driver)

- Formulary access and reimbursement in CKD patient segments (payer and health-system policies)

- Substitution dynamics among phosphate binders (sevelamer salts, lanthanum carbonate, iron-based binders, and calcium-based alternatives)

- Drug supply continuity and generic pricing pressure (since calcium acetate is widely available in generic form)

In practice, calcium acetate’s uptake and pricing are most sensitive to payer rules that favor lower-cost binder strategies, and to clinical guideline alignment around target phosphate control and pill burden/tolerability.

How does competition shape pricing and share?

Phosphate binders compete on total cost of therapy, dosing convenience, and comparative clinical guidance. Calcium acetate competes mainly with:

- Calcium-free binders (e.g., sevelamer and lanthanum): often preferred when calcium load or hypercalcemia risk is a concern

- Calcium-containing competitors (e.g., calcium carbonate): substitute within the calcium class is common when budgets tighten

- Emerging binders (notably iron-based approaches in some regions): tend to shift share where they obtain strong payer coverage

Market effect: calcium acetate pricing typically trends toward the low end of the class because it is broadly generic and because treatment decisions in CKD frequently prioritize cost-effective phosphate control across patient tiers. Share is sustained by payer preference for economical options, tempered by clinical selection for patients where calcium burden is not appropriate.

What are the main demand segments?

Demand concentrates in CKD patients who require phosphate binding:

- Dialysis patients (high binder adherence and recurring use)

- Non-dialysis CKD where phosphate management is initiated based on guideline targets and local practice

Demand stability: phosphate binder therapy is chronic and recurring, which tends to produce steady utilization once a patient is established on therapy. Volume can still fluctuate with:

- Dialysis capacity changes

- Guideline adoption cycles

- Payer formulary updates

How do formulary and reimbursement dynamics affect revenue?

Revenue trajectory for calcium acetate is typically governed by:

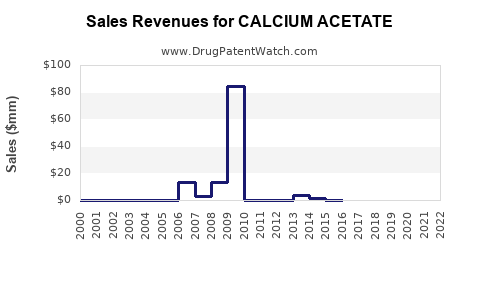

- Exclusivity end and generic diffusion: once marketed as a brand, the field usually becomes dominated by generics after patent or exclusivity windows end

- Step therapy and prior authorization rules: can affect switching between calcium acetate and non-calcium binders

- Negative and positive formulary rules for calcium load risk: payer policies sometimes restrict calcium-based binders for subsets (e.g., hypercalcemia risk)

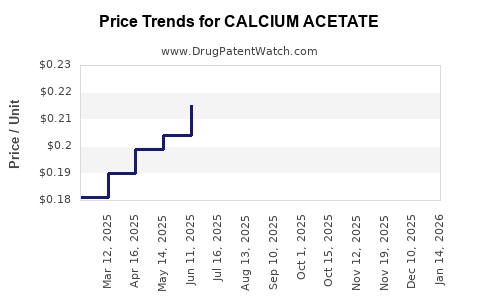

Financial implication: even if total binder demand grows with CKD prevalence, the average selling price (ASP) typically compresses over time due to generic competition and periodic tendering.

What is the likely market lifecycle pattern for calcium acetate?

Given calcium acetate’s status as a widely used, typically generic phosphate binder, its market lifecycle usually follows:

- Brand build phase (initial adoption in phosphate control)

- Patent/exclusivity rollover and increased generic entry

- Price compression driven by tendering and channel competition

- Margin stabilization at lower ASP levels, with revenue growth driven more by volume than price

For investors and R&D planners, this pattern means valuation is more sensitive to:

- volume expansion and retention in dialysis/non-dialysis cohorts

- ability to win or retain payer access

- manufacturing scale and supply cost position

What financial trajectory is typical: revenue, profitability, and risk?

Revenue growth drivers

- Patient prevalence growth in CKD

- Dialysis program continuity and chronic treatment adherence

- Payer procurement cycles that keep calcium acetate on preferred lists when clinically acceptable

Revenue headwinds

- ASP erosion from generic competition

- Switching to non-calcium binders for clinical contraindications or formulary decisions

- Tender outcomes that can shift contracted pricing downward

Profitability and cashflow drivers

- Manufacturing cost discipline (API and excipient sourcing, batch yield, compliance)

- Channel mix (hospital tenders vs retail vs specialty pharmacy)

- Working capital and inventory management due to recurring orders but competitive pricing

Key financial risks

- Regulatory or quality events affecting supply continuity

- Rapid payer switching during formulary resets

- Competitive substitutions within the binder class that can reduce volume share

Where do patents and exclusivity matter for revenue?

Calcium acetate revenue usually does not depend on long-term patent protection in the way newer oncology and biologic assets do. Instead, financial trajectory is dominated by:

- generic availability post-patent expiration

- any remaining method of use, formulation, or jurisdiction-specific protections (where applicable)

- regulatory and data exclusivity tied to specific registration pathways and filings in each country

Because phosphate binders are a mature therapeutic area, the market tends to become price-competitive quickly once generic entry is unlocked.

What do pricing dynamics imply for investors and R&D decisioning?

For a mature generic-like phosphate binder market, the revenue/trajectory playbook typically centers on:

- Defending formulary placement

- Competing on total cost-of-therapy and patient adherence

- Maintaining low-cost, reliable supply

- Minimizing compliance and batch-related downtime

- Targeting reimbursement frameworks where calcium-based options remain preferred

If you are evaluating investment attractiveness, the core question is not whether calcium acetate can gain patients, but whether a supplier can sustain:

- share against generics and substitutes

- ASP levels through tender cycles

- stable margins through manufacturing scale

How do macro and policy factors affect near- to mid-term performance?

Macroeconomic

- inflation impacts manufacturing and logistics costs, often compressed by competitive price pressure

- currency volatility can affect import-dependent supply chains (by region)

Health policy

- dialysis utilization changes are slow-moving but persistent

- formulary tightening can increase substitution away from calcium-based binders in certain cohorts

- value-based procurement and tendering can reset prices on a fixed schedule

What is the most actionable view of trajectory: scenario mapping

Below is a practical trajectory framework used for market sizing and financial planning in mature phosphate binder categories.

Scenario A: Stable formulary access, steady volume

- Price: declines at a slower rate after initial generic erosion

- Revenue: grows mainly with patient volume

- Margin: stable if manufacturing unit costs stay contained

Scenario B: Tender-driven ASP compression

- Price: sharp decline during contract resets

- Revenue: flat to modest growth if volume offsets pricing

- Margin: compresses unless cost position improves

Scenario C: Clinical and reimbursement substitution

- Price: stable or declining

- Revenue: declines in share if payers expand restrictions against calcium-based binders

- Margin: higher risk due to lost volume and less favorable channel mix

What KPIs best forecast CALCIUM ACETATE financial performance?

- Dialysis and CKD patient counts in covered populations

- Formulary status (preferred vs restricted tier)

- Tender outcomes (contracted ASP and volume commitments)

- Switching rates between calcium acetate and competing binders

- Manufacturing yield and compliance events (direct margin impact)

- Inventory turns and chargebacks/returns (channel profitability)

Key Takeaways

- Calcium acetate demand is anchored to chronic CKD phosphate control, with volume tied to dialysis and CKD prevalence.

- Financial performance is dominated by generic competition and procurement-driven ASP compression, with revenue growth typically more volume-led than price-led.

- Market share is sensitive to formulary and payer rules, especially around calcium load risk and step therapy use.

- The most decisive financial levers are supply cost position, contract outcomes, and retention of formulary status amid substitution to calcium-free binders.

FAQs

-

Is calcium acetate’s market growth primarily volume-driven or price-driven?

Primarily volume-driven; price usually compresses due to generic competition and tendering.

-

What main competitors pressure calcium acetate pricing and share?

Other phosphate binders in the CKD class, especially calcium-free binders and calcium-based alternatives.

-

How do dialysis and non-dialysis CKD cohorts differ for revenue planning?

Dialysis patients typically produce more stable recurring utilization; non-dialysis cohorts depend more on guideline adoption and payer initiation criteria.

-

What factor most affects profit margins for calcium acetate suppliers?

Manufacturing cost position and supply reliability, because pricing faces frequent downward pressure.

-

Does patent protection meaningfully shape long-term revenue for calcium acetate?

Generally less than for patent-protected specialty drugs; revenue is mostly shaped by generic diffusion and formulary access rather than long exclusivity cycles.

References

- KDIGO. KDIGO 2017 Clinical Practice Guideline Update for the Diagnosis, Evaluation, Prevention, and Treatment of Chronic Kidney Disease-Mineral and Bone Disorder (CKD-MBD). Kidney International Supplements. 2017.

- US FDA. Drug Approval Packages and information for calcium acetate products (labeling and approval history). U.S. Food and Drug Administration.