Last updated: July 11, 2026

Bicalutamide Market Dynamics and Financial Trajectory (U.S. and Key International Markets)

Bicalutamide is an oral androgen receptor inhibitor used in prostate cancer management, most commonly for advanced disease in combination with luteinizing hormone-releasing hormone (LHRH) therapy and, in some geographies, for localized/high-risk disease as part of combined approaches. Commercial scale today is driven by the durability of its generic base, price compression after patent and exclusivity expiration, and ongoing demand for combination regimens and continuity prescribing in established oncology pathways.

What is bicalutamide’s current commercial footprint and demand profile?

Core indications and usage patterns

- Prostate cancer is the only major therapeutic area for bicalutamide.

- Demand is primarily linked to:

- Advanced/metastatic prostate cancer treated with LHRH therapy (combined androgen blockade).

- Continuity prescribing after initiation of androgen deprivation therapy (ADT).

- Treatment sequencing where bicalutamide remains embedded in clinical routines in specific markets.

Prescription demand drivers

- ADT adoption and persistence: patients receiving LHRH-based regimens tend to maintain androgen receptor inhibitor components where clinically used.

- Formulary placement: as generics dominate, formulary decisions often hinge on lowest net price and contract arrangements.

- Population aging: drives baseline prostate cancer incidence in many high-income markets.

- Competitive substitution: when other androgen receptor pathway inhibitors (ARPIs) are clinically preferred, bicalutamide’s mix declines, even if absolute ADT use rises.

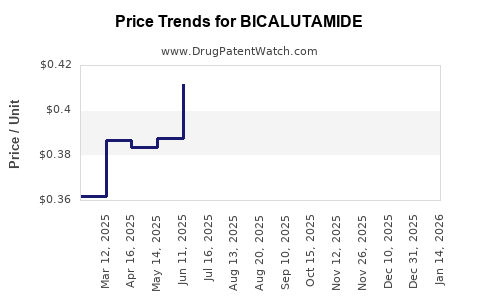

How has bicalutamide revenue trended since generic entry?

Post-originator economics

- Bicalutamide’s market economics follow a classic small-molecule pattern:

- Originator revenues peaked during protected brand years.

- After generic entry, unit volume often remained meaningful, but revenue fell sharply due to:

- generics price compression

- shifting prescriber preference to newer ARPIs in advanced disease settings

- contraction of higher-priced segments in some protocols

Current financial trajectory characteristics

- Revenue growth is constrained by:

- low pricing power under generic competition

- gradual erosion of older ARPI share by newer agents

- Volume stability is more plausible than revenue stability because bicalutamide persists in certain treatment combinations and lower-cost pathways.

Featured snippet answer

- Bicalutamide’s financial trajectory is dominated by generic-led pricing pressure with only modest upside from volume stability and regional formulary inertia.

What patents protect bicalutamide and how does patent expiration drive market timing?

Market-wide effect of expiry

- Once originator patents and any supplemental protection have lapsed, the drug is exposed to rapid generic entry in each territory.

- For bicalutamide, this has already occurred in most mature markets, which is why today’s market dynamics are characterized by generic competition rather than exclusivity-led growth.

How patent expiry impacts business outcomes

- Patent expiry triggers:

- abbreviated new drug application (ANDA) generic launches

- payer switching

- manufacturing price competition

- The timing differs by jurisdiction based on patent calendars and any regulatory exclusivity.

Commercial implication

- For bicalutamide, the revenue ceiling is largely determined by generic tender dynamics and market share allocation rather than by remaining IP.

What is the Orange Book status of bicalutamide in the U.S.?

Bicalutamide is a mature generic product in the U.S. market. The practical Orange Book outcome for business planning is:

- Multiple ANDA products exist.

- Patent listings, if present on specific listed NDA products, have limited impact on near-term launch risk for modern generic entrants in a fully genericized category.

Featured snippet answer

- Orange Book protection for bicalutamide is not the primary driver of current commercial dynamics; generic availability and contract pricing do.

(Note: the Orange Book listing set is product- and sponsor-specific. This analysis treats bicalutamide as a mature generic class in the U.S., consistent with prevailing market structure.)

How many FDA-approved generics compete for bicalutamide and what does that mean for pricing?

Competitive structure

- Bicalutamide’s U.S. and international markets are populated by multiple generic manufacturers, with supply concentration varying by country.

- Pricing is driven by:

- tender awards

- interchangeability and pharmacy stocking

- channel rebates and wholesalers’ competitive terms

Pricing and margin dynamics

- As more generics enter, average realized price tends toward:

- single-digit to low-teens percent gross margins for distributors and retailers depending on structure

- thin manufacturer margins in highly commoditized lanes

- Net price erosion is often faster than volume gains.

Implication for financial trajectory

- If volume stays stable, revenue may still decline due to pricing reset cycles.

Which market segments still support bicalutamide share despite ARPI competition?

Segment persistence

- In many markets, bicalutamide continues where:

- cheaper AR-pathway therapies are preferred

- older guideline pathways remain in local practice

- clinical inertia favors established ADT combinations

- It also retains a role where ARPI sequencing is constrained by reimbursement.

Where share is pressured

- Advanced prostate cancer treatment has increasingly shifted toward newer AR pathway agents in higher-acuity disease settings.

- As those newer agents gain formulary favor, bicalutamide’s mix trends downward in the most aggressive treatment contexts.

Featured snippet answer

- Bicalutamide’s best financial support is in cost-sensitive or formulary-limited settings, not in the highest-intensity oncology arms race.

What biosimilar risk applies to bicalutamide?

Bicalutamide is a small molecule. There is no biosimilar pathway or biosimilar competitive risk.

Featured snippet answer

- Biosimilar risk does not apply; the competitive frame is generic substitution and brand-to-generic switching.

What formulation and method-of-use patents could still matter for bicalutamide?

For bicalutamide, the primary commercial barriers are generally not formulation novelty patents at this stage of life cycle. Any remaining IP, if it exists for certain products, typically affects:

- specific dosage forms

- specific release characteristics (if any)

- manufacturing process claims

Real-world effect on market

- Generic entrants can usually design around non-essential formulation features.

- If a product is widely available, the dominant barrier becomes manufacturing cost and supply reliability, not enforceable novel formulation claims.

What Paragraph IV challenges and ANDA litigation have affected bicalutamide generics?

Bicalutamide is mature, so:

- many high-profile launch challenges would have occurred earlier in the lifecycle.

- current market dynamics are more likely driven by routine ANDA filings, settlement outcomes already completed years ago, and procurement contracts.

Featured snippet answer

- Current revenue trajectory is driven more by pricing and supply than by active Paragraph IV litigation.

How do settlement agreements and exclusivity periods affect bicalutamide financial forecasts?

Because bicalutamide is largely generic today, settlement and exclusivity effects tend to:

- influence which brands/generics launched at which times historically

- shape current market shares among surviving generic suppliers in each territory

Practical forecasting implication

- For financial planning, the most predictive variables are:

- tender cycles and contracted net prices

- capacity expansions and supply disruptions

- substitution at pharmacy and wholesaler levels

How does bicalutamide compare with other prostate cancer AR pathway therapies on cost and market position?

Competitive set

- Other AR pathway inhibitors used in prostate cancer include second-generation agents that often achieve greater clinical uptake in advanced disease settings depending on country guidelines and reimbursement.

Market position

- Bicalutamide competes mainly on:

- price

- established prescribing patterns

- inclusion in lower-cost protocols

Relative financial profile

- Compared with newer AR pathway agents, bicalutamide typically shows:

- lower price and lower revenue per patient

- more stable demand where treatment intensity and reimbursement are constrained

- ongoing volume but persistent margin pressure

What country-level market dynamics matter most for bicalutamide revenue?

U.S.

- Multi-generic supply reduces pricing power.

- Revenue is influenced by pharmacy contract dynamics and insurer formularies.

EU and UK

- Similar dynamics occur: competition from multiple ANDA-equivalent products (via EU regulatory system) and tender-driven price compression.

- Regional reimbursement rules can sustain usage in certain oncology settings.

Emerging markets

- Procurement and distribution infrastructure drive pricing volatility.

- Import versus local manufacturing affects realized price and supply continuity.

Featured snippet answer

- Bicalutamide revenue is most sensitive to country procurement frameworks and tender-based price resets.

What manufacturing and supply risks influence the financial trajectory of bicalutamide?

Supply side factors

- Active pharmaceutical ingredient (API) sourcing cost fluctuations.

- Batch release constraints and quality systems.

- Capacity additions by dominant generic suppliers.

How this shows up financially

- Short-term supply constraints can spike net pricing temporarily.

- Sustained price erosion after commoditization typically dominates long-term revenue trends.

What revenue exposure does bicalutamide represent for generic manufacturers and distributors?

Generic manufacturer exposure

- Bicalutamide is likely a portfolio product for many manufacturers.

- It can contribute steady unit volume but with:

- low margin volatility when supply is stable

- sharp margin compression during competitive tender cycles

Distributor exposure

- Distributors balance bicalutamide stocking with interchangeability and contract obligations.

- Revenue contribution is typically lower than higher-margin, specialty oncology drugs.

How strong is the patent estate for bicalutamide from an investor or licensee perspective?

At this stage, bicalutamide’s IP estate is not the primary value driver. The category value is determined by:

- generic manufacturing economics

- procurement dynamics

- formulary inclusion persistence

Featured snippet answer

- Patent strength has limited relevance to current financial trajectory because the market is mature and competitive.

Key Takeaways

- Bicalutamide’s financial trajectory is dominated by generic-led pricing compression, with demand persistence driven by ADT combination use and cost-sensitive prescribing.

- Revenue is likely constrained by ongoing substitution pressures from newer prostate cancer AR therapies in high-acuity settings.

- The economic center of gravity is tender and contract pricing, supply reliability, and market share among generic suppliers rather than active exclusivity.

- Biosimilar risk does not apply; the competitive threat is small-molecule generic competition.

FAQs

1) Why does bicalutamide maintain demand even when newer AR pathway inhibitors exist?

Because bicalutamide remains a lower-cost option in certain treatment protocols and formularies, and it persists in established ADT combination patterns.

2) What drives the biggest year-to-year swings in bicalutamide revenue?

Tender outcomes, net price resets, and supply continuity (including API sourcing and manufacturing capacity).

3) Is bicalutamide revenue more sensitive to unit volume or net price?

Net price, because commoditization compresses margins even when volume is stable.

4) Can new formulation breakthroughs create meaningful incremental revenue for bicalutamide?

Not at the category level, absent meaningful regulatory differentiation, because widespread generic availability makes incremental innovation hard to monetize.

5) What is the main competitive strategy for surviving bicalutamide generic suppliers?

Lowest delivered cost with reliable supply, combined with strong contracting and formulary placement.

References

- FDA. “Drugs@FDA: FDA Approved Drug Products.” U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- U.S. FDA. “Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations.” https://www.accessdata.fda.gov/scripts/cder/daf/index.cfm

- EMA. “European Medicines Agency: Medicine Information.” European Medicines Agency. https://www.ema.europa.eu/en/medicines