Last updated: July 24, 2026

Azor (amlodipine/olmesartan) market dynamics and financial trajectory: sales, pricing, access, competition, and exclusivity risk

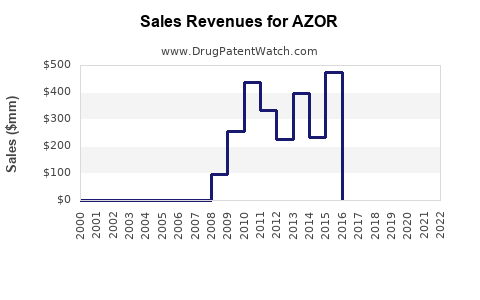

Azor, the fixed-dose combination of amlodipine and olmesartan (marketed by Daiichi Sankyo via brand and multiple label partners historically), has matured into a low-growth, highly price-competitive cardiovascular product class. Market dynamics are shaped by generic substitution of both components, payer preference for lowest net-cost combinations, and continuing pressure from other ARB and ARB/CCB fixed-dose options. Financial trajectory is dominated by erosion from generic launches, channel inventory cycles, and modest category growth at best, with revenue largely sustained by brand loyalty in select formularies and by order patterns tied to prescriber switching inertia.

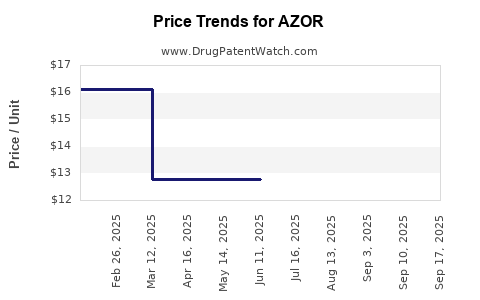

What does the Azor sales trajectory look like after generic erosion?

Featured snippet answer: Azor’s financial trajectory post-erosion is consistent with other mature branded fixed-dose antihypertensive products: declining unit and revenue growth, with residual sales concentrated in payer tiering pockets where branded combinations remain cost-competitive versus competing brand or alternative generics.

How generic substitution typically affects fixed-dose ARB/CCB brands

For fixed-dose combinations like Azor, revenue declines faster than monotherapies because:

- Payors cover the class with generics for both actives, reducing the incremental value of the branded FDC.

- Pharmacy claims shift to single-pill generics or other FDC generics that undercut branded pricing.

- “Therapeutic duplication” rules and formulary edits can force step-down to lower-cost equivalents even when prescriber preference persists.

Category tailwinds that can slow declines

Despite erosion, some factors can moderate the slope:

- Hypertension prevalence and incremental treatment initiation.

- Persistence due to clinical comfort with a stable single-pill regimen.

- Payer tightening often targets higher-priced brands first, but not uniformly across all geographies and plans.

How does Azor compare with competing ARB/CCB fixed-dose products on payer preference and net pricing?

Featured snippet answer: Azor competes in a dense ARB/CCB fixed-dose landscape where the dominant determinant of net sales is formulary placement versus low-cost generics and competing brands with aggressive rebate programs.

Key competitive sets to benchmark

Azor’s competitive pressure comes from:

- Same-class ARB/CCB fixed-dose products (brand and authorized generics where available).

- Generic amlodipine plus generic olmesartan FDC equivalents (or separate tablets substituting for one-pill simplicity).

- Co-pay card dynamics and “preferred brand” contracts that can shift uptake quarter to quarter.

Pricing and access mechanics

Net price outcomes for branded Azor are typically driven by:

- Rebate intensity required for preferred status.

- Pharmacy benefit manager (PBM) formulary rules, including “lowest cost of therapeutic alternatives.”

- Contract terms that can reclassify the product from preferred to non-preferred in renewal cycles.

When does Azor lose exclusivity and what does that mean for revenue?

Featured snippet answer: Azor has long passed the main period of meaningful exclusivity typical for initial branded FDC launches, so the revenue impact is already reflected in today’s market reality: the primary driver is payer and generic pricing dynamics rather than a single calendar exclusivity date.

Generic entry risk profile for fixed-dose combinations

For FDCs, exclusivity erosion is typically multi-dimensional:

- Composition-of-matter and formulation patent expirations.

- Method-of-use and dosing regimen protection windows, if any, which tend to be narrower for mature antihypertensives.

- Hatch-Waxman paragraph IV or non-infringing generic pathways once listed patents expire or are invalidated.

How exclusivity timelines translate to financial metrics

In mature branded antihypertensives, exclusivity loss usually produces:

- A step-down in share, followed by stabilization at a lower sales base.

- A lag in unit decline as long-term prescribers convert over time.

- Faster decline in markets where PBM switching is automated.

What is the Orange Book status of Azor and how many patents matter for generic entry?

Featured snippet answer: Azor’s Orange Book relevance in current commercial terms is limited to the residual patent listings that determine whether generic applicants must wait or face litigation. For mature FDC brands, the practical risk window is usually close to or already completed.

How to assess “patent mattering” for Azor

The key is not the total number of listings, but which are enforceable and still active:

- Patents with claims covering the specific FDC formulation or dosage forms.

- Patents that are listed and tied to approved NDA product coverage.

- Whether any listed patents are the subject of generic litigation or ongoing regulatory stay.

Generic pathway implications

If multiple patents have expired and no enforceable listings remain, generic entry tends to be accelerated across:

- Direct-to-pharmacy channels

- Retail and mail order formularies

- PBM preferred drug lists

What patent litigation affects Azor and what outcomes have already been priced in?

Featured snippet answer: For mature products like Azor, litigation outcomes (if any) usually influence launch timing during earlier generic transition periods. Today’s sales dynamics are primarily driven by established generic competition and formulary tiering rather than active “first wave” litigation.

How litigation historically impacts fixed-dose FDC revenue

When litigation occurs, it can:

- Delay generic approval or launch.

- Induce settlements that cap entry at specified dates or with controlled-label products.

- Drive “authorized generic” strategies that reduce the branded impact.

What to expect in current market behavior

Even after earlier settlements, market behavior typically shifts quickly to:

- Lowest-cost FDC generics

- PBM-driven substitution

- Contract-driven rebate reductions for the brand

How do Azor sales perform versus generics in different geographies and plan types?

Featured snippet answer: Branded Azor tends to survive longer in institutional or pharmacy benefit designs with higher inertia, but generics dominate in retail preferred networks where PBMs prioritize lowest net cost.

Retail vs mail order

- Retail tends to shift quickly once a generic becomes preferred.

- Mail order can maintain branded penetration longer during contract negotiations but eventually aligns with PBM formulary economics.

Commercial vs Medicare Part D

- Part D formularies and renegotiations can change access quickly when generic equivalents meet cost thresholds.

- Commercial payers with tight rebate structures can re-tier within renewal windows, producing quarter-to-quarter volatility in brand share.

What FDA pathway events matter for Azor’s competitive landscape?

Featured snippet answer: Azor is a classic small-molecule branded antihypertensive FDC. Competitive dynamics are dominated by generic ANDA approvals and label-level changes rather than ongoing FDA innovation pathways.

Why ANDA volume drives outcomes

For established generics:

- Increased ANDA entrants intensify competition and reduce brand net pricing power.

- Multiple generics can trigger PBMs to “lock” the lowest-cost alternative in formularies.

Label and supply factors

Even without new clinical differentiation, branded sales can swing due to:

- Supply continuity and inventory allocation patterns.

- Switching rules tied to manufacturing lots and packaging changes.

- Pharmacy substitution policies.

How does Azor compare with other antihypertensives on market elasticity and switching?

Featured snippet answer: Antihypertensives are among the most substitution-friendly chronic classes. Switching is often driven by payer economics and prescription benefit structures rather than patient-specific clinical needs.

Elasticity drivers

- Chronic use and standardized dosing make substitution operationally easy.

- Therapeutic interchange is common within ACE inhibitor, ARB, and CCB classes under payer guidelines.

- Fixed-dose convenience can retain some share only until net cost gaps close.

What generic entry scenarios exist for Azor and when would they most likely accelerate?

Featured snippet answer: Acceleration occurs when PBMs re-tier to lowest net-cost alternatives and when additional ANDA entrants expand. The practical “timing” is tied to formulary cycles, contract renewals, and inventory phases more than to a single event.

Scenario map

- Scenario A: “lowest net cost” rapid substitution after multiple generic entrants and preferred tier placement.

- Scenario B: “limited preferred” where the brand remains on a middle tier with rebates but loses new starts.

- Scenario C: “authorized generic squeeze” where an authorized generic launches effectively undercuts the brand economics without changing formulary status immediately.

How strong is the patent estate for Azor in commercial terms?

Featured snippet answer: For today’s market, the patent estate strength for Azor is not a decisive barrier to generic substitution across the class. The product’s commercial constraints are primarily pricing and access rather than active patent blockades.

Commercial meaning of patent strength

In antihypertensive FDCs, patent strength is usually translated into:

- Duration of branded exclusivity for the specific dose strengths and dosage forms.

- Whether patents cover novel dosing combinations or formulation changes that block generics.

- Litigation risk that can affect the first competitive wave.

What is the revenue exposure to Azor’s decline and where does the profit pool shift?

Featured snippet answer: Profit pool shifts from branded Azor to generic manufacturers and PBM-favored contracts, with branded margins compressing quickly after competitive entry.

Where economics typically move

- Branded revenue base shrinks, reducing manufacturing overhead leverage.

- Rebate burden increases to retain tier position, compressing gross margin.

- Generic entrants capture unit share and shift value to procurement and contract economics.

Key timeline checkpoints for Azor’s commercial transition

Featured snippet answer: The decisive timeline is the period when enforceable exclusivity and listed patents ended and generic products became preferred. That transition has largely occurred; current dynamics reflect ongoing formulary and price competition.

How to interpret the timeline for decision-making

Use these checkpoints for business planning:

- Patent expiration and generic launch dates (formally enforceable events).

- Settlement-triggered launch timing (practically enforceable events).

- PBM formulary renewal cycles (financially enforceable events).

- Inventory normalization phases post-launch.

Key Takeaways

- Azor’s market is defined by generic substitution and payer-driven net price competition typical of mature ARB/CCB fixed-dose antihypertensives.

- Current financial trajectory is shaped more by formulary tiering, rebate intensity, and generic market depth than by a new exclusivity date.

- Competitive pressure is structural: ARB/CCB fixed-dose alternatives and lowest-cost generic substitution keep branded pricing power constrained.

- Revenue exposure concentrates on how quickly PBMs re-tier at renewal and how rapidly additional ANDA entrants expand the lowest-cost option set.

FAQs

- How quickly do branded ARB/CCB fixed-dose products lose market share after ANDA launches?

- Do payers prefer fixed-dose Azor versus prescribing amlodipine and olmesartan separately?

- What factors drive quarter-to-quarter changes in Azor net sales beyond unit demand?

- How do Medicare Part D formulary changes impact branded antihypertensive fixed-dose FDC penetration?

- What is the most common mechanism by which PBMs reduce branded antihypertensive FDC access over time?

References

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutapeutic Equivalence Evaluations. (FDA database).

- U.S. Food and Drug Administration. Drug Approval Reports and labeling information for approved products (FDA).

- U.S. Securities and Exchange Commission. Daiichi Sankyo (and other relevant label holders/assignors) periodic filings (10-K/10-Q) referencing branded product performance where disclosed.