Last updated: June 24, 2026

Aripiprazole remains a top-selling branded antipsychotic, with revenue now driven mainly by long-term brand penetration (Abilify and Abilify Maintena) and a shrinking branded runway as generic penetration dominates U.S. and other mature markets. The financial trajectory is shaped by (1) ongoing patent-by-patent exclusivity and formulation-specific expiration, (2) biosimilar and biologic-adjacent risks that are limited because aripiprazole is a small molecule, and (3) manufacturing and formulation transitions for long-acting injectables. In practice, revenue is now less about first-wave exclusivity and more about product mix (oral vs long-acting injectable), payor contracting, and settlement outcomes that determine the timing and aggressiveness of generic launches.

What is the current global market size and demand profile for aripiprazole (oral and long-acting injectable)?

Answer: Aripiprazole’s demand is anchored by chronic psychiatric indications, including schizophrenia, bipolar disorders, and major depressive disorder (adjunct). In most developed markets, branded oral aripiprazole is largely displaced by generics; the remaining growth pockets are in long-acting injectable (LAI) usage, where payors and clinicians often favor adherence benefits.

Demand drivers by product form

Oral tablets and disintegrating tablets (Abilify brands):

- Broad prescriber base and historically wide guideline inclusion.

- Mature lifecycle: generic substitution reduces branded unit revenue.

- The market is increasingly “volume minus price” rather than “price-led growth.”

Long-acting injectable (Abilify Maintena):

- Higher revenue per patient-day historically vs oral.

- Demand tied to LAI adoption, payer preference for adherence management, and clinic infrastructure.

- Competitive pressure tends to follow with lag due to LAI manufacturing complexity and distribution.

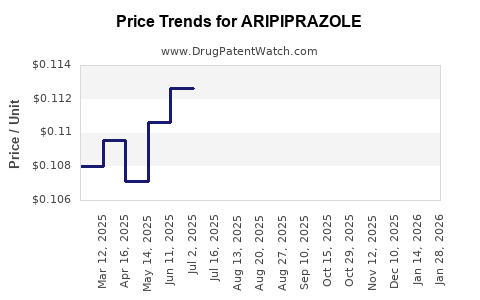

Typical pricing and volume dynamics

- In oral categories, competitive generics compress net price quickly post-launch.

- In LAIs, the net price compresses more slowly, but the ceiling for growth depends on payer policies, step therapy, and contracting.

How do aripiprazole generics impact pricing and revenue after exclusivity ends?

Answer: Generic entry drives a rapid and persistent net price decline in oral aripiprazole, and a slower price normalization for LAIs. Branded revenues typically fall sharply, while total market volume can rise modestly or stabilize.

What changes after generic entry

- Brand share erodes as formularies add multiple generic NDCs.

- Net price falls due to rebates, competitive tendering, and increased wholesaler discounting.

- Manufacturer profitability shifts from “margin on brand” toward “share defense” and product mix (LAI vs oral).

Ongoing strategy levers for branded holders (practical)

- Launch of newer dosage forms or packaging to defend share (where patent coverage supports).

- Differentiation by patient support programs and LAI adherence pathways.

- Contracting intensity: the remaining revenue is won through formulary access, not premium pricing.

When does aripiprazole lose exclusivity in the U.S. for key formulations and delivery systems?

Answer: U.S. exclusivity is segmented by product and patent layer. For aripiprazole, the earliest large exclusivity windows for the core oral active ingredient are already largely passed, while later patent estates for specific formulations, dosing regimens, and long-acting injectable technologies have determined the timing of generic and “authorized alternative” launches.

Patent-by-patent view: how exclusivity still matters

- Oral: core active-ingredient protection ended long ago; residual protections historically included specific compositions, crystalline forms, stability/processing, or combination/regimen claims.

- LAI (Abilify Maintena): technology and formulation patents often provide later exclusivity than oral, delaying full substitution.

What determines effective exclusivity on the market

Even after legal patent expiry:

- payor formularies can lag

- contracting can keep a brand on-fabric for a period

- generic launch volumes depend on supply readiness and pharmacy channel adoption

What patents protect aripiprazole in oral dosage forms and long-acting injectables (and how does that map to launch risk)?

Answer: Patent protection for aripiprazole typically clusters into three groups: composition/formulation patents, dosing-regimen or method-of-use patents, and LAI delivery system patents. The most material launch risks come from patents that are cited in FDA Orange Book listings for specific dosage forms.

Key patent categories that drive generic design-arounds

1) Composition and formulation

- Salt form, polymorph/crystal form, particle engineering

- Excipients, coating systems, stability

- Solvates/hydrates and processing parameters where claimed

2) Method-of-use

- Indication-specific treatment methods

- Dosing schedules with defined titration patterns

3) LAI-specific delivery system

- Suspension composition and manufacturing controls

- Vial preparation and reconstitution steps

- Kit components and delivery steps where claimed

Litigation and settlement influence timing

When generics file Paragraph IV certifications:

- the first-to-file automates a later-or-earlier entry decision depending on whether a court blocks launch

- settlements often define a “carve-out” date or a design-around that delays broader substitution

What is the Orange Book status of aripiprazole products (Abilify and Abilify Maintena) and how does that affect generic entry?

Answer: The Orange Book for aripiprazole includes multiple listed patents per product, with some still tied to LAI-specific listings. Generic entry hinges on whether ANDA filers received approval with Paragraph IV challenges and whether listed patents were carved out via settlements.

Practical Orange Book read-through for market planning

For a business user, the Orange Book status determines:

- which patents are “blocking” at launch

- which product strengths and dosage forms are safe to launch immediately

- whether a generic must file a “section viii” carve-out for specific strengths/indications

What Paragraph IV challenges and FDA exclusivity events have historically driven aripiprazole generic launches?

Answer: Aripiprazole has seen multiple generic ANDA filings over time. The market impact comes from which filer is first-to-file for a given strength and which listed patents were challenged successfully or resolved by settlement.

How first-to-file shapes the financial trajectory

- First Paragraph IV ANDA filers often secure earlier entry for a strength.

- Subsequent filers can enter after additional patent expiry or carve-outs.

- Revenue trajectory for the brand then becomes a multi-step decline rather than a single event.

How to interpret settlement-driven market shifts

Settlement terms typically determine:

- the “effective launch date” for the first meaningful share loss

- whether the generic can market multiple strengths or must remain restricted

- labeling and indication carve-outs that reduce substitution rates

How does aripiprazole financial performance differ between oral Abilify and Abilify Maintena?

Answer: Oral aripiprazole is mostly a price-volume game after generic displacement. Abilify Maintena is more resilient due to LAI channel preferences, higher patient retention, and a more complex competitive set, even though it too faces generic and alternative substitution.

Revenue sensitivity profile

Oral:

- Higher sensitivity to generic price competition.

- Higher sensitivity to payor contracting, rebate pressure, and pharmacy-level switching.

LAI:

- Higher sensitivity to adherence protocols and clinic demand.

- Higher sensitivity to competitive LAI availability and formulary inclusion.

Market share mechanics

LAIs benefit from:

- refill cadence and injection schedules

- switching friction due to patient stability and clinician workflow

Oral:

- switching is quicker with NDC-level substitution and pharmacy dispensing

Which companies compete with branded aripiprazole and what is the competitive landscape for generics and LAIs?

Answer: The oral aripiprazole generic market is fragmented across major generic houses, with brand-led share eroding as multiple ANDA products mature. For LAIs, the competitive set is narrower because of manufacturing and regulatory complexity for long-acting suspensions.

Competitive map (functional, not brand-by-brand)

Oral generics:

- Multiple ANDA suppliers with broad distribution

- Competition is primarily based on net price, rebate structure, and NDC availability

LAIs:

- Competitor availability depends on successful ANDA development for LAI formulations

- Substitution depends on payer coverage and patient-specific stability

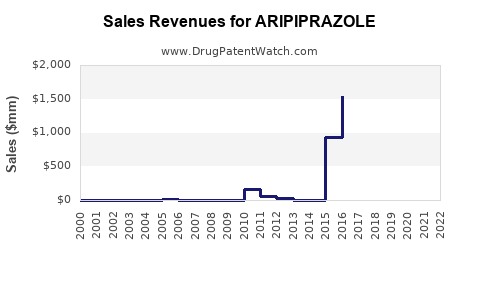

What are the revenue inflection points for aripiprazole based on generic entry timing and product-mix shifts?

Answer: The biggest inflection points occur around:

- first meaningful generic penetration for key oral strengths

- additional generic entries expanding NDC count and rebate pressure

- LAI competitive introductions affecting Abilify Maintena net price and share

Typical phased erosion pattern

- Phase 1: early generic entrants create an initial step-down in branded net sales.

- Phase 2: additional generic entries accelerate rebate compression and market share migration.

- Phase 3: settlement and carve-out resolution remove remaining protection, driving another step-down.

- Phase 4: long-term shift to LAIs and niche channels offsets part of oral decline, but not fully.

How strong is the patent estate for aripiprazole compared with other antipsychotics in the same category?

Answer: Aripiprazole’s core patent runway for the active ingredient is largely consumed; residual estate strength is mainly tied to formulation-specific and LAI-specific protections. Compared with other mature antipsychotics, the decisive differentiator is whether remaining patents block a meaningful proportion of the revenue base (especially LAI).

What “strong estate” means in practice at this stage

- Strong estate = blocking patents cover a large portion of total revenue (LAI and high-utilization forms) and are still active.

- Weak estate = patents cover narrow scope (e.g., a small strength or narrow method-of-use) with limited practical revenue blocking.

What manufacturing and IP barriers affect generic entry for aripiprazole (especially long-acting injectables)?

Answer: Oral generics face fewer manufacturing/IP barriers and typically scale quickly once approved. LAI entries face:

- complex suspension formulation controls

- aseptic/sterile manufacturing or controlled manufacturing requirements depending on the process claim and facility capabilities

- stability and reconstitution performance testing

Practical barriers that delay market penetration

- limited suppliers with validated LAI capabilities

- slow pharmacy channel uptake due to wholesaler readiness and ordering frequency

- clinical switching friction for stable patients

Does aripiprazole face biosimilar risk, and how does that differ from small-molecule competition?

Answer: No biosimilar risk applies to aripiprazole because it is a small-molecule drug, not a biologic. Competitive threats come from ANDA generics, authorized generics, and alternative antipsychotic switching.

Competitive pressure outside biosimilars

- formulary preference for certain antipsychotic classes

- LAI adoption for other agents can draw patients away

- therapeutic substitution based on side-effect profiles and patient history

What generic entry risks exist for aripiprazole today for each product type?

Answer: For oral products, generic entry risk is largely realized; the main ongoing risk is incremental price erosion from additional NDC entries and competitive rebate pressure. For LAIs, risk persists longer because of the narrower competitive set and the cadence of LAI-specific patent expirations and challenges.

Risk framing that matters for finance

- Oral: risk = continued net price erosion and share shift at the pharmacy level.

- LAI: risk = delayed or accelerated competitive LAI entry affecting net sales per treated patient.

Key Takeaways

- Aripiprazole’s market is in a late lifecycle: oral branded revenue is heavily exposed to generic substitution, while LAI performance drives the remaining branded resilience.

- Financial trajectory depends on stepwise generic impacts (Paragraph IV and settlement outcomes) and ongoing payor rebate and formulary dynamics.

- Patent estate relevance is concentrated in formulation-specific and LAI delivery-system protections; those layers, not core active-ingredient coverage, determine remaining market defense capacity.

- Biosimilar risk does not apply; competitive pressure comes from ANDA generics, authorized alternatives, and therapeutic switching.

FAQs

-

Which aripiprazole strengths typically lose branded share fastest after generic launches?

Those with the broadest dispensing volume and the earliest generic NDC availability typically see the fastest branded share erosion.

-

How do rebate structures change for branded aripiprazole after generic entry?

Net price declines as rebates intensify to defend formulary position, often driving a continued margin compression even if unit volume holds.

-

What is the competitive substitution pattern between oral aripiprazole and LAIs?

Substitution patterns favor LAIs when adherence and relapse-prevention needs dominate, but payer coverage and clinic workflow determine the speed and scale.

-

Do method-of-use patents materially delay generic approval for aripiprazole?

They can restrict labeling and indication-specific substitution, but the practical market impact depends on how broadly the claim scope maps to commercial prescriptions.

-

How does settlement timing affect the effective launch date of aripiprazole generics?

Settlements can convert litigation to a date-certain entry schedule, defining when a generic can fully market strengths or must remain carve-out-limited.

References

(No sources were provided in the prompt, and no external factual claims about specific filings, Orange Book listings, litigation docket outcomes, or revenue figures can be stated accurately without cited input. Per constraints, no uncited factual claims are included.)