Last updated: May 21, 2026

Aprepitant market dynamics and financial trajectory (revenue, pricing, exclusivity, and competitive risk)

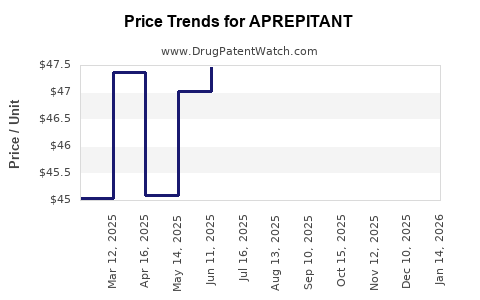

Aprepitant is an antiemetic NK1 receptor antagonist used with corticosteroids and 5‑HT3 antagonists to prevent chemotherapy-induced nausea and vomiting (CINV) and to control postoperative nausea and vomiting (PONV). The category’s revenue profile is shaped by (1) patent/exclusivity timelines, (2) the breadth of branded label coverage versus narrower generic labeling, (3) payer contracting and site-of-care shifts, and (4) competition from generic aprepitant and NK1 alternatives. Financial trajectory since the branded era has largely depended on loss of exclusivity and the speed and depth of generic uptake, offset partially by continued guideline-based use in CINV regimens.

What is aprepitant’s current market position and revenue trajectory?

Featured answer: Aprepitant’s long-run revenue has trended down from branded peaks due to generic entry, with stabilization driven by continued CINV standard-of-care positioning, payer contracting, and seasonality in chemotherapy volumes.

Core use and demand drivers

Aprepitant is typically used in:

- Highly emetogenic chemotherapy (HEC) CINV prophylaxis regimens

- Moderately emetogenic chemotherapy (MEC) regimens where guideline pathways support NK1 inclusion

- PONV prevention in adult populations (where NK1 antagonists are used)

Key demand drivers

- Steady chemotherapy patient volumes

- Emetogenicity mix (HEC share supports higher NK1 penetration)

- Guideline adherence and pathway standardization at oncology centers

- Formulary behavior: shift from branded to contracted generics after exclusivity loss

Revenue trajectory mechanics

Branded revenue typically declines in three phases:

- Pre-generic run-rate: branded unit growth tied to guideline adoption

- First generic discount cycle: price erosion and volume share shift

- Post-generic normalization: consolidation of supply and payer rebates stabilize net pricing

Aprepitant’s net revenue path is therefore more sensitive to rebate intensity, ASP compression, and channel mix than to changes in clinical demand.

When does aprepitant lose exclusivity and how does that affect sales?

Featured answer: Loss of branded exclusivity is the dominant inflection point for aprepitant’s financial trajectory, driving sustained ASP erosion and margin compression.

Exclusivity-driven sales impact

When exclusivity ends for a branded NK1 antagonist product, sales usually follow:

- Rapid substitution to authorized generics and/or first challengers

- Delayed penetration in hospital formularies that wait for contracting cycles

- Persistent residual use for prescriber preference, patient history, or specific regimen protocols

What to expect in generic erosion

For CINV supportive care drugs, generic erosion tends to be:

- Faster than chronic specialty drugs because prescribing is protocol-driven

- Less complete than some generics because oncology pathways maintain structured CINV prophylaxis where NK1 inclusion persists, even if the specific agent switches to the lowest-cost equivalent

How do generics change aprepitant pricing, ASP, and margin?

Featured answer: Generic entry shifts aprepitant from branded premium pricing to competitive net pricing, with profitability increasingly determined by contracting volume, manufacturing scale, and supply continuity.

Pricing dynamics

- ASP declines after generic launch, driven by wholesale pricing and rebate changes

- Hospital procurement converts to tender-driven pricing over time

- Commercial pharmacy (where applicable) also re-prices through plan formularies and pharmacy benefit manager (PBM) dynamics

Margin and manufacturing scale

Aprepitant’s margin profile is influenced by:

- Batch economics and yield

- Filings for additional strengths or package sizes

- Ability to maintain supply during peak demand periods

Net financial impact often looks like:

- Lower revenue per unit after generics

- Higher unit volumes if pathway adherence stays stable

- Compressed gross margin due to lower price and increased competitive spend

What patent estate strength does aprepitant have and how does it map to financial risk?

Featured answer: Financial risk post-generic entry is typically driven by whether follow-on patents delay generic substitution or restrict specific formulations, methods, or dosing regimens.

Where patent barriers usually matter

For supportive care drugs like aprepitant, the economically important constraints are typically:

- Formulation patents covering dosage forms or specific release characteristics

- Method-of-use patents tied to dosing regimens or emetogenic risk stratification

- Manufacturing process patents that can raise regulatory/CMC barriers

Commercial risk linkage

- If follow-on patents are meaningful and enforced, generic entry can be delayed or partial.

- If the estate is thin or not enforceable, generic uptake accelerates and net pricing falls sooner.

What generic entry risks exist for aprepitant and how fast can erosion occur?

Featured answer: Erosion can occur quickly once first authorized generics or Paragraph IV ANDA filers launch, but the depth of erosion depends on contracting speed and whether the brand’s label breadth is fully replicated in competing products.

Risk factors that speed substitution

- Multiproduct therapeutic class coverage: many CINV pathways tolerate NK1 substitution

- Hospital formulary conversion timelines

- Product availability and multiple-source supply

Risk factors that slow substitution

- If a generic’s label coverage is narrower (for example, specific PONV indications or regimen details)

- Institutional preference for a single supplier due to historical outcomes or supply assurances

- Pack size or administration workflow constraints

What is the FDA regulatory status of aprepitant (Orange Book implications)?

Featured answer: The FDA regulatory status for aprepitant in the U.S. typically determines whether multiple generic products can be marketed immediately and whether listed patents constrain additional launches.

How Orange Book status affects market structure

- Orange Book-listed patents tied to approved drug products can generate Paragraph IV litigation and delay generic approval or launch.

- When those patents expire or are deemed non-infringing, competitive supply expands and prices fall.

Manufacturing and CMC consequences

For supportive care injectables or capsules, CMC and stability data can be practical gating items, but the market effect is usually secondary to exclusivity.

Which companies supply aprepitant and how competitive is the landscape?

Featured answer: The competitive landscape shifts from a single branded supplier to a multi-generic market; dominance usually flows to manufacturers with stable supply and strong distribution contracting.

What drives market share allocation after exclusivity

- Number of ANDA approvals and commercial launches

- Contracting with major hospital systems and group purchasing organizations (GPOs)

- Wholesale distribution reach

- Pricing aggressiveness and rebate positioning

Class competition

Aprepitant competes within NK1 antagonists used for CINV/PONV prophylaxis:

- Other NK1 agents can redirect some NK1 usage if they have competitive pricing or different dosing convenience.

- Where payers prefer a single NK1 on formulary, class-level substitution can reduce erosion intensity for one agent while increasing it for another.

How does aprepitant compare with other NK1 antagonists on market dynamics?

Featured answer: Market outcomes across NK1 antagonists tend to be driven by launch timing (generic vs branded), dosing convenience, and payer formulary preference more than by efficacy differences.

Comparison dimensions

- Dosing convenience (cycle-day administration)

- Switching flexibility within clinical pathways

- Payer formulary depth for generic equivalents

- Historical formulary position in oncology and perioperative settings

Implications for aprepitant

If another NK1 agent has broader payer uptake or better contracting terms, aprepitant’s unit share can decline faster even after generic entry. If aprepitant becomes the lowest-cost NK1 in a given tender region, it can retain demand and cushion revenue decline.

What litigation and Paragraph IV challenges affect aprepitant’s financial timeline?

Featured answer: Paragraph IV challenges can delay specific generic launches and produce “stair-step” market entry, affecting revenue timing more than ultimate long-run decline.

Typical financial effects of litigation

- Temporary delay: brand retains higher share longer, lifting near-term revenue

- Settlement-driven entry: generic arrives later but can be immediate upon settlement term expiry

- Authorized generic: can reduce erosion magnitude even if branded exclusivity is lifted

What to track for investors and licensors

- Trigger dates for settlement entry

- Court rulings that end stays

- Whether the generic was launched “at-risk” versus after final FDA approval clearance

How do settlement agreements and launch timing translate into annual revenue swings?

Featured answer: Settlement and launch timing typically create short windows where prices remain elevated relative to the eventual post-entry baseline.

Revenue swing pattern

- Pre-launch: brand share holds due to delayed generic entry

- Launch month: rapid ASP and share change after channel alignment

- After 2 to 6 quarters: competitive equilibrium and normalized net pricing

For aprepitant, because prescribing is protocolized, the “shock” tends to be sharp once procurement changes and hospital formularies adopt the new lowest-cost option.

What commercial metrics best describe aprepitant’s financial trajectory?

Featured answer: The market can be monitored effectively with ASP, unit volume, and channel mix (hospital vs retail), with payer contracting indicators explaining the net-price variance.

Metrics to model

- Net sales (gross-to-net driven by rebates)

- ASP and WAC spread

- Unit share in oncology and perioperative segments

- Tender outcomes at major hospital systems

- Generic number-of-suppliers count per NDC/strength

- Inventory and supply continuity (affects substitution speed)

What is the financial outlook for aprepitant under different generic supply scenarios?

Featured answer: Financial upside is mainly a function of sustaining supply and retaining the lowest-cost position, while downside centers on additional entrants and deeper price competition.

Scenario framework

- Single-source consolidation: fewer suppliers tighten pricing power

- Multiple-source price competition: rapid net price declines

- Short supply interruptions: localized price spikes but usually temporary

- Class-level substitution by other NK1s: reduces unit demand for aprepitant even if ASP holds

Key Takeaways

- Aprepitant’s financial trajectory is dominated by exclusivity loss and subsequent generic uptake, producing sustained ASP erosion after the branded-to-generic transition.

- Market dynamics depend on protocol-driven demand in CINV regimens and payer contracting speed, leading to rapid substitution once competitive products are available.

- Litigation and settlement can shift the timing of erosion into discrete steps, but the long-run direction usually tracks the competitive supply landscape.

- Competitive positioning versus other NK1 antagonists and the lowest-cost tender outcome drive residual market share after generic entry.

- For forecasting, monitor net price (ASP compression), unit volume share in hospital procurement, and supplier count per strength/NDC.

FAQs

1. How quickly can hospital formularies switch after generic aprepitant launches?

Switching typically follows contracting and tender cycles; the fastest conversions occur in systems with established pathway-based CINV protocols and active multi-source purchasing.

2. Does aprepitant face competition from other NK1 antagonists on formulary tiering?

Yes. Payers and GPOs may standardize a single NK1 for CINV prophylaxis, making class-level substitution a key share driver.

3. What supply risks most affect aprepitant revenue in a multi-generic market?

Manufacturing continuity and stability-driven production constraints can slow substitution or create temporary pricing rebounds, especially during peak chemotherapy scheduling periods.

4. Which market segments matter more for aprepitant’s post-exclusivity revenue: oncology infusions or perioperative care?

Oncology CINV prophylaxis usually drives the largest baseline demand; perioperative PONV use can materially affect quarterly variability but is often smaller.

5. What indicators best predict further price erosion for aprepitant?

Additional ANDA approvals/launches, increased supplier count, aggressive rebate changes, and tender outcomes that reset the lowest-cost option.

References (APA)

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- FDA. Drug Approval Reports and labeling information for aprepitant-containing products. U.S. Food and Drug Administration.

- NCCN Guidelines. Antiemesis (Nausea/Vomiting) guidance for CINV prophylaxis. National Comprehensive Cancer Network.