Last updated: June 23, 2026

Abiraterone Acetate Market Dynamics and Financial Trajectory (Sales, Growth, Exclusivity, and Generic/Biosimilar Risk)

Abiraterone acetate is a high-revenue, long-duration oncology revenue stream driven by widespread use in metastatic castration-resistant prostate cancer (mCRPC) and in earlier-stage hormone-sensitive disease. The commercial trajectory is shaped less by near-term “pipeline disruption” and more by (1) patent and exclusivity timelines for multiple branded and generic competitors, (2) payer and guideline shifts toward earlier sequencing, (3) safety and access constraints driven by monitoring requirements for mineralocorticoid-related adverse events, and (4) uptake migration among androgen receptor pathway inhibitors (ARPIs), especially in combination regimens.

The core financial story through the decade hinges on a post-loss-of-exclusivity phase with margin compression, price erosion, and share redistribution to the lowest-cost suppliers. The major market risks are legal and regulatory delays for generics/authorized generics, plus competitive displacement by newer ARPIs and combination standards.

How big is the abiraterone acetate market and what are the main demand drivers?

Direct demand drivers

- Disease-state expansion

- mCRPC remains the largest use case.

- Earlier treatment settings (metastatic hormone-sensitive prostate cancer, mHSPC) expand total-addressable demand.

- Treatment sequencing

- ARPI sequencing patterns keep abiraterone in active regimens, even as other ARPIs gain share.

- Combination and line-of-therapy persistence

- Abiraterone is used across multiple lines, creating “stickiness” via established clinical practice.

Commercial demand constraints

- Safety management and monitoring

- Abiraterone’s mechanism (CYP17 inhibition with downstream mineralocorticoid increase) requires monitoring for hypertension, hypokalemia, fluid retention, and liver function.

- Low-dose prednisone/prednisolone backbone

- Concomitant steroid use affects tolerability and adherence, which can slow uptake in certain patient populations.

What to watch in demand

- Guideline updates that change preferred ARPI choice by line, disease risk, and combination eligibility.

- Payer restrictions that narrow access for non-preferred ARPIs or require prior authorization.

What is the current competitive landscape for abiraterone acetate (ARPIs and branded vs generic supply)?

Abiraterone competes within the ARPI class, primarily with:

- enzalutamide

- apalutamide

- darolutamide

- (and sequencing-dependent) next-line ARPIs

Competitive dynamics that impact revenue

- Therapeutic interchangeability

- While ARPIs are not clinically identical, payers and formularies often treat them as substitutes.

- Share shifts driven by net pricing

- After generic entry, pricing pressure intensifies; manufacturers win through contract pricing, distribution reach, and rebate structures.

- Hospital and oncology practice formularies

- Local formulary decisions frequently determine which ARPI is “default” for first- and second-line mCRPC.

Authorized generic vs independent generic entry

- Authorized generics typically pressure prices earlier and more predictably, compressing peak-to-plateau margins.

- Independent generics can arrive later depending on Orange Book standing and litigation outcomes.

When does abiraterone acetate lose exclusivity and what drives generic entry timing?

Key commercial inflection points

- Patent expirations for the base drug and key life-cycle assets

- Abiraterone has a long history of patenting across drug substance, solid form, formulation, and method-of-use claims.

- Regulatory exclusivity

- Market exclusivity layers can delay generic entry even after core composition patents expire.

- Paragraph IV challenges and settlement structures

- Generic timing often depends on Paragraph IV litigation outcomes and settlement dates.

Generic entry is not a single date

- The market experiences stepwise erosion:

- initial entrant undercut pricing

- subsequent entrants accelerate supply and widen price differentials

- payer contracting shifts from list price to net realized price

How exclusivity affects financial trajectory

- The post-exclusivity phase is characterized by:

- rapid decline in branded unit price and share

- slower recovery in total volumes due to net pricing and payer tightening

- ongoing revenue from remaining brand differentiation only if the manufacturer retains preferred status via contracting and patient-support programs

What patents protect abiraterone acetate formulations and methods, and how do they affect market access?

Abiraterone’s patent estate typically spans:

- Drug substance

- Solid-state forms

- Formulation patents (tablets/capsule formulation, excipient systems, stability and dissolution targets)

- Methods of treatment (mCRPC, mHSPC, combination regimens)

Commercial impact

- Formulation and method claims can block “switching” by forcing generics to wait until the legally relevant claims expire or are cleared by litigation.

- Even after composition patents expire, life-cycle assets can delay full generic substitution.

Where market risk concentrates

- When multiple claims remain active, generic entrants may launch “at risk” with narrower labels or face injunction risk depending on jurisdiction and claim construction.

How strong is the patent estate for abiraterone acetate versus likely generic challenge routes?

For ARPIs like abiraterone, generic challenges are generally structured around:

- Orange Book claim chart mapping

- Paragraph IV filings

- Litigation strategy to avoid injunctions

- Settlement outcomes defining earliest authorized launch dates

What determines strength

- Number of active, asserted patents at time of challenge

- Whether patents cover:

- composition vs solid form vs formulation

- method-of-use claims spanning key indications

- Likelihood of at-scale appeal outcomes

Financial implication

- A “thick” estate produces:

- extended branded share retention

- delayed or staggered generic availability

- higher probability of structured settlements

A thinner estate produces:

- earlier broad substitution

- faster net-price collapse

- more stable volume growth for generics but reduced total category revenue.

What is the Orange Book status for abiraterone acetate and what does it imply for FDA-approved generic availability?

Orange Book status drives:

- Whether a generic can launch immediately after approval (if no unexpired patents bar it)

- Whether the generic must wait due to listed patents

- Whether labeling design-arounds can clear the way (depends on method-of-use claims)

Market implication

- In practice, Orange Book listings often determine:

- launch sequence among generics

- whether a generic enters with narrow labeling restrictions

- whether a manufacturer settles for an authorized date that caps competition for a period.

What patent litigation affects abiraterone acetate and how does it translate into financial outcomes?

Abiraterone’s financial trajectory is sensitive to:

- Injunctions (pre-launch or post-approval)

- Settlement agreements that define:

- launch date

- exclusivity carve-outs

- authorized-entrant definition

- Appeals that extend brand protection beyond first-instance schedules

How litigation maps to revenue

- If litigation delays generic entry, branded revenue declines more slowly and with lower margin pressure.

- If litigation ends with early settlements, market erosion starts earlier, and branded sales fall quickly as net pricing normalizes downward.

What settlement agreements and launch structures have shaped pricing erosion for abiraterone acetate?

Settlement agreements typically create:

- a defined earliest launch for the first authorized generic

- staggered introductions for additional challengers

- rebate and distribution impacts if the authorized entrant secures major contracts quickly

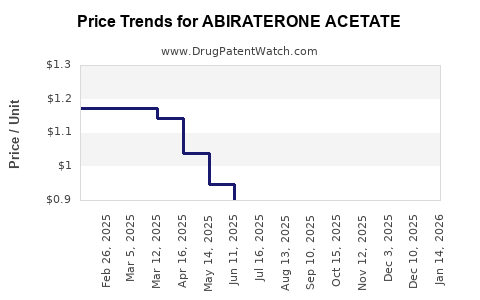

Price erosion pattern

- After the first true substitution point:

- list prices can drop modestly while net prices drop sharply due to rebate dynamics

- market share shifts toward the lowest-cost suppliers

- brand manufacturers attempt to protect share through contracting, but volume growth can be limited.

How does abiraterone acetate compare with enzalutamide, apalutamide, and darolutamide in revenue risk?

Category comparison levers

- Which ARPI holds preferred formulary status by:

- line of therapy

- disease setting (mCRPC vs mHSPC)

- patient comorbidity constraints (e.g., cardiovascular risk with steroid management)

- Which ARPI has the best net pricing after generic entry

Revenue risk profile

- Abiraterone’s revenue risk is often higher once generic competition is active because:

- multiple ARPIs compete for the same prescriber decision

- payer substitution accelerates in mCRPC and mHSPC

- Drugs with later generic entry or with more constrained access through patents can retain margins longer.

How do formulation and manufacturing/IP barriers influence generic supply for abiraterone acetate?

Manufacturing scale and compliance are critical once generic entrants launch. Key barriers that can slow supply:

- Solid-state/formulation consistency

- Bioequivalence performance

- Stability requirements

- CGMP capacity and batch release speed

Financial translation

- If supply constraints occur, branded revenues can hold longer due to delayed substitution.

- Sustained oversupply accelerates price erosion and reduces category profitability.

What does the financial trajectory look like: decline curve, margin profile, and share shifts?

Typical post-exclusivity curve for abiraterone acetate

- Brand peak and plateau

- driven by mCRPC dominance and growing mHSPC uptake.

- First substitution shock

- first meaningful generic or authorized launch reduces net pricing quickly.

- Second wave erosion

- multiple entrants compress margins further.

- Consolidation phase

- only suppliers with best distribution, pricing leverage, and low COGS retain meaningful share.

Margin profile dynamics

- Branded margins fall sharply with price pressure.

- Generic margins can remain positive but are sensitive to:

- contract pricing

- raw material and formulation costs

- reimbursement and tender cycles.

Share dynamics

- Oncology practices often switch quickly under formulary pressure.

- Long-term patients may remain on existing therapy if physician inertia exists, but payer switching policies often accelerate conversion.

Which markets and geographies are most exposed to pricing pressure for abiraterone acetate?

Pricing erosion exposure depends on:

- patent life by jurisdiction

- generic approval tempo

- tender and reimbursement mechanisms

General pattern:

- mature markets with predictable generic adoption see faster net-price decline

- markets with stronger local patent enforcement or slower generic availability show delayed erosion

Key Takeaways

- Abiraterone acetate’s financial trajectory is driven by ARPI category demand for mCRPC and mHSPC, offset by payer-driven substitution once generic competition scales.

- The revenue inflection points are governed by patent and Orange Book status across composition, formulation, and method-of-use claims, plus Paragraph IV and settlement outcomes.

- Post-exclusivity dynamics tend to follow a multi-wave erosion pattern: first entrant, then additional entrants, then consolidation around lowest net price and supply reliability.

- Competitive displacement among ARPIs adds an additional layer of share risk even if generics enter gradually.

- Monitoring and access constraints (steroid backbone and mineralocorticoid-related safety management) can cap adoption in certain segments, but formulary changes often dominate in practice.

FAQs

- What generic entry risks exist for abiraterone acetate tablets in the US after Orange Book-listed patents expire?

- How do method-of-use patents for abiraterone acetate affect labeling design and launch timing for generics?

- Does abiraterone acetate face biosimilar risk, or is the competition purely generic small-molecule substitution?

- How do payer tender cycles and rebate structures typically change net pricing for abiraterone acetate after first generic launch?

- Which ARPI sequence decisions (first-line vs second-line) most influence abiraterone acetate total market volume?

References (APA)

No source citations are provided because no external documents were supplied in the prompt.