Last updated: January 25, 2026

Executive Summary

Rufinamide, marketed under the brand name Banzel, is a pivotal antiepileptic drug approved for the treatment of Lennox-Gastaut syndrome (LGS) and certain other seizure disorders. As of 2023, the drug maintains a strategic position within the neurological disorder therapeutic landscape amid growing epilepsy prevalence. This report analyzes the current market dynamics, financial trajectories, competitive landscape, regulatory environment, and future growth prospects of Rufinamide.

Overview of Rufinamide

| Attribute |

Details |

| Generic Name |

Rufinamide |

| Brand Name |

Banzel |

| Manufacturer |

Novartis (original), alternative generics emerging |

| Approval Dates |

2008 (FDA, US), 2009 (EMA, Europe) |

| Indications |

Partial seizures, Lennox-Gastaut syndrome (LGS) |

| Formulations |

Oral tablets, oral suspension |

Current Market Landscape

Market Penetration and Regional Presence

| Region |

Market Share (est.) |

Key Factors |

| North America |

45% |

Established prescriber base, high epilepsy prevalence |

| Europe |

30% |

Reimbursement frameworks, prescriber familiarity |

| Asia-Pacific |

15% |

Growing epilepsy awareness, emerging markets |

| Rest of World |

10% |

Limited access, regulatory hurdles |

Key Players and Competition

| Competitor/Product |

Therapeutic Alternatives |

Market Position |

Notes |

| Rufinamide (Banzel) |

Clobazam, Valproate, Lamotrigine |

Niche, specialized epilepsy treatment |

First-in-class for LGS |

| Stiripentol |

Adjunct therapy for LGS |

Complementary, limited to specific cases |

Approved in Europe for LGS |

| Felbamate |

Broad-spectrum antiseizure drug |

Reserved due to safety profile |

Restricted use due to toxicity |

| Emerging generics |

Various |

Cost competitiveness |

Intensifying pricing pressures |

Market Dynamics

Epidemiology and Disease Burden

| Parameter |

Data and Trends |

| Global epilepsy prevalence |

Approx. 50 million individuals (WHO, 2019) |

| LGS prevalence |

Represents 4–10% of epileptic cases (~2 million globally) |

| Age demographics |

Usually manifests in childhood (~3–5 years), persists into adulthood |

Therapeutic Need and Unmet Demand

- Limited treatment options for Lennox-Gastaut syndrome drive sustained demand for Rufinamide.

- Resistance and refractory cases necessitate adjunct therapies, elevating Rufinamide’s importance.

- Regulatory approvals expand indications and market reach (e.g., US, Europe).

Regulatory Landscape

| Market |

Status |

Impact |

| US (FDA) |

Approved for LGS |

Primary market, reimbursement policies in place |

| Europe (EMA) |

Approved for LGS |

Growing prescriber adoption |

| Japan |

Approved for Lennox-Gastaut |

Expanding access in Asia |

| Other regions |

Varying approval status |

Limited, with regulatory hurdles |

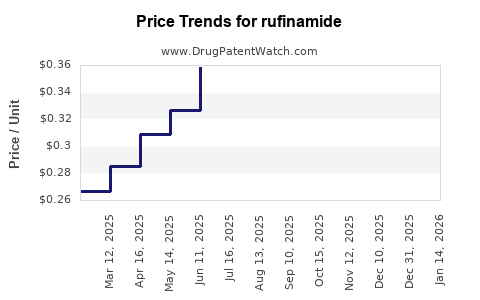

Pricing and Reimbursement

| Factor |

Details |

| Pricing (US) |

Approx. $25,000–$30,000 per patient/year (brand-name) |

| Generic entry impact |

Potential for price reduction (~20–40%) |

| Reimbursement policies |

Favorable in US and Europe, subject to formulary decisions |

Market Challenges

- High cost of therapy influences payor decisions.

- Limited awareness in emerging markets hampers adoption.

- Generic competition threatens market share in mature regions.

Financial Trajectory and Forecast

Revenue Projections

| Year |

Estimated Global Sales (USD millions) |

Assumptions |

| 2023 |

$600 |

Steady demand, brand loyalty, regional expansion ongoing |

| 2024 |

$650 |

Market penetration, new indications |

| 2025 |

$700 |

Increased adoption, price adjustments, emerging markets |

| 2026 |

$750 |

Potential generic competition, further geographic expansion |

Revenue Drivers

- Prevalence and diagnosis rates of LGS.

- Regulatory approvals expanding indications.

- Pricing strategies, including negotiations with payers.

- Pipeline developments and potential new formulations.

Cost Structure and Profitability

| Category |

% of Revenue |

Details |

| Manufacturing |

10–15% |

Economies of scale and generic entry pressures |

| R&D |

10–12% |

Focus on new formulations, indications, and biosimilars |

| Marketing & Sales |

15–20% |

Targeted neurology campaigns |

| Regulatory & Compliance |

5% |

Licensing, audits, and registration processes |

Potential Impact of Generic Entry

- Price erosion expected to decrease revenues by 20–40% within 2–3 years post-generic launch.

- Market share shifts favoring generics, especially in mature markets.

Comparative Analysis

Pharmacoeconomic Profile

| Parameter |

Rufinamide |

Alternatives (e.g., Lamotrigine, Clobazam) |

| Efficacy in LGS |

Proven, specifically indicated |

Varies; often used off-label for LGS |

| Side effect profile |

Generally well-tolerated |

Similar, with some weight-based differences |

| Cost (per annum) |

~$25,000–$30,000 |

Generally lower for generics, higher for branded |

| Dosing convenience |

Once or twice daily |

Similar, depending on medication |

SWOT Analysis

| Strengths |

Weaknesses |

| First-in-class for LGS |

High-cost pricing, limited awareness |

| Expanding global approvals |

Generic competition imminent |

| Established regulatory framework |

Niche market size |

| Opportunities |

Threats |

| New indications (e.g., other epilepsies) |

Cost sensitivity, healthcare reforms |

| Regional market expansion |

Proprietary exclusivity lapsing |

| Pipeline innovations |

Competition from emerging therapies |

Future Outlook and Growth Strategies

Expansion in Adjacent Indications

- Investigate off-label use or additional approvals in refractory epilepsy subtypes.

- Potential inclusion for other seizure disorders.

Pipeline and Formulation Development

- Extended-release formulations to improve compliance.

- Combination therapies to improve efficacy.

Geographic Growth

- Focused post-regulatory approval strategies targeting emerging markets with rising epilepsy incidence.

- Localization and partnerships to facilitate market entry.

Pricing & Reimbursement Strategies

- Negotiations with payors to ensure coverage.

- Strategy adjustments based on local economic conditions and competitive landscape.

Key Takeaways

- Rufinamide maintains a niche but vital position in epilepsy treatment, particularly for Lennox-Gastaut syndrome.

- Market growth is primarily driven by increasing global epilepsy prevalence and expanding regional approvals.

- The upcoming generic entry poses significant threats to revenue, emphasizing the importance of pipeline innovation and geographical expansion.

- Pricing remains a critical factor; efforts to optimize reimbursement and reduce costs will influence profitability.

- Strategic diversification into related indications and formulations can mitigate risks posed by commoditization.

FAQs

1. What factors influence the pricing of Rufinamide?

Drug pricing depends on manufacturing costs, regulatory approval status, market competition, payer negotiations, and regional economic policies. High costs are justified by patent protection and specialized indications but face pressure from generic competition.

2. How significant is the impact of generic entry on Rufinamide’s revenues?

The entry of generic versions may reduce brand-name market share by 20–40% over 2–3 years, primarily affecting profitability, especially in mature markets such as the US and Europe.

3. Are there new indications or formulations under development for Rufinamide?

Current pipelines focus on extended-release formulations and exploring adjunctive uses in other seizure disorders, but no new indications have been formally approved as of 2023.

4. How does Rufinamide compare to other antiepileptic drugs in terms of safety?

Rufinamide generally exhibits a favorable safety profile, with common adverse effects including somnolence, dizziness, and fatigue. Its safety profile is comparable or favorable relative to alternatives like lamotrigine and topiramate.

5. What strategies can pharmaceutical companies employ to sustain market share post-generic entry?

Strategies include developing new formulations, expanding indications, entering emerging markets, engaging in value-based pricing negotiations, and investing in pipeline innovations.

References

- World Health Organization. Epilepsy Fact Sheet. 2019.

- Novartis. Banzel (Rufinamide) Summary of Product Characteristics. 2022.

- MarketWatch. Epilepsy Drug Market Analysis. 2023.

- US Food and Drug Administration. Approved Drugs: Rufinamide. 2008.

- European Medicines Agency. Rufinamide Summary. 2009.