Last updated: February 19, 2026

Nateglinide, an oral insulin secretagogue, has experienced shifts in its market position due to patent expirations and the introduction of newer diabetes treatments. Its financial trajectory reflects these dynamics, with declining sales for originator products and ongoing generic competition.

What is Nateglinide and How Does it Function?

Nateglinide is a short-acting meglitinide analog used to manage type 2 diabetes mellitus [1]. It works by stimulating insulin secretion from pancreatic beta cells in response to elevated blood glucose levels. This mechanism aims to reduce postprandial hyperglycemia. Nateglinide binds to a specific site on the ATP-sensitive potassium channel of beta cells, leading to channel closure, cell depolarization, and subsequent calcium influx, which triggers insulin release [2].

Key pharmacological properties include:

- Onset of Action: Rapid, typically within 30 minutes [1].

- Peak Plasma Concentration: Achieved in approximately 1 hour [1].

- Half-life: Short, around 1.5 hours, facilitating flexible dosing before meals [2].

- Administration: Oral, taken shortly before meals (within 30 minutes) [1].

Nateglinide is primarily indicated as an adjunct to diet and exercise to improve glycemic control in adult patients with type 2 diabetes. It is often used in combination with metformin or thiazolidinediones, or as monotherapy when diet and exercise alone are insufficient [3].

Patent Landscape and Market Exclusivity

The patent landscape for nateglinide has significantly influenced its market exclusivity and subsequent financial performance. The primary patents protecting nateglinide and its formulations have expired in major markets.

Key patent details and their impact:

- United States: The foundational patents for nateglinide, including U.S. Patent No. 4,488,389 and its related continuations and divisionals, have expired. These patents provided market exclusivity for the innovator product, marketed as Starlix by Novartis. The last significant patent protection for the original formulation expired in the early to mid-2010s [4].

- Europe: Similar patent expirations occurred across European Union member states. Supplementary Protection Certificates (SPCs) extended some exclusivity periods, but these have also lapsed.

- Other Major Markets: Patent expiry timelines in Canada, Japan, and Australia have followed similar patterns, with the expiration of core patents opening the door for generic market entry.

The expiration of these patents has led to:

- Generic Competition: Numerous generic manufacturers have entered the market with bioequivalent versions of nateglinide. This has resulted in significant price erosion for the drug.

- Loss of Market Share: The innovator product has seen a substantial decline in market share and revenue as healthcare providers and payers shift towards lower-cost generic alternatives.

- Limited New Patenting: While new patents might exist for novel formulations, delivery systems, or combination therapies, the core compound patents are no longer active, limiting opportunities for substantial market exclusivity on the drug itself.

Market Dynamics and Competitive Landscape

The market dynamics for nateglinide are characterized by a mature product facing intense generic competition and evolving treatment paradigms for type 2 diabetes.

Key Market Dynamics:

- Generic Dominance: The market is heavily saturated with generic nateglinide. Pricing is driven by competition among manufacturers, leading to significantly lower wholesale acquisition costs compared to the innovator product's launch period.

- Price Erosion: The introduction of generics has caused substantial price erosion. For example, the average selling price (ASP) for nateglinide has decreased by over 90% from its peak levels during the innovator's exclusivity period [5].

- Shifting Treatment Guidelines: Recent diabetes treatment guidelines emphasize drugs with cardioprotective and nephroprotective benefits, such as GLP-1 receptor agonists and SGLT2 inhibitors. These newer classes offer additional advantages beyond glycemic control, diminishing the standalone appeal of older oral agents like nateglinide for many patient profiles [6].

- Niche Therapeutic Use: Nateglinide's role has become more specialized. It is primarily utilized in patients who require rapid postprandial glucose control and may not be candidates for, or have failed, newer therapeutic classes, or where cost is a primary driver.

- Geographic Variations: Market penetration and sales volume for nateglinide can vary by region, influenced by local healthcare policies, formulary restrictions, and the availability and adoption of alternative diabetes medications.

Competitive Landscape:

- Direct Competitors (Other Meglitinides): Repaglinide is the closest competitor within the meglitinide class. Both drugs share a similar mechanism of action and dosing regimen. However, repaglinide has also faced generic competition and has seen its market share decline [7].

- Indirect Competitors (Other Oral Hypoglycemics):

- Metformin: Remains the first-line therapy for most patients with type 2 diabetes due to its efficacy, safety profile, low cost, and established benefits in reducing cardiovascular events [6].

- DPP-4 Inhibitors: Drugs like sitagliptin and linagliptin offer good glycemic control with a low risk of hypoglycemia and weight gain.

- SGLT2 Inhibitors: Empagliflozin, canagliflozin, and dapagliflozin provide significant cardiovascular and renal benefits, often positioning them as preferred agents in patients with established atherosclerotic cardiovascular disease or chronic kidney disease [6].

- Thiazolidinediones (TZDs): Pioglitazone and rosiglitazone are also available generically but have seen reduced usage due to concerns about side effects such as fluid retention and increased fracture risk [8].

- Newer Injectable Therapies:

- GLP-1 Receptor Agonists: Semaglutide, liraglutide, and dulaglutide offer substantial weight loss benefits and proven cardiovascular outcome benefits, making them highly attractive options [6].

The competitive environment is thus characterized by intense pressure from generics and a strong preference for newer drug classes that offer broader therapeutic advantages.

Financial Trajectory and Sales Performance

The financial trajectory of nateglinide has followed a predictable pattern post-patent expiry. Sales for the innovator product have drastically declined, while the market for generic nateglinide has stabilized at a much lower price point.

Innovator Product (Starlix) Performance:

- Peak Sales: Starlix achieved peak annual sales in the range of $300 million to $400 million globally in the late 2000s to early 2010s, prior to significant patent expirations [9].

- Post-Patent Expiry Decline: Following the loss of market exclusivity in major markets (approximately 2012-2015), sales of Starlix experienced a steep decline. By 2017-2018, global sales for Starlix had fallen below $50 million annually and have continued to decrease [9, 10].

- Discontinuation: Novartis has largely phased out marketing and sales efforts for Starlix in many regions due to its diminished market presence and the availability of generics. In some markets, the product may have been formally discontinued.

Generic Nateglinide Market:

- Market Size: The total market size for generic nateglinide is difficult to ascertain precisely due to fragmentation and a lack of specific reporting by individual generic manufacturers. However, it is estimated to be in the range of $50 million to $100 million annually worldwide, based on volume and average selling prices [5, 11].

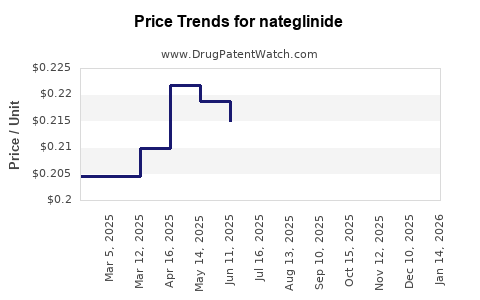

- Price Trends: Generic nateglinide is available at a fraction of the innovator's price. A typical 30-day supply can cost between $10 and $30 USD, depending on the pharmacy, insurance coverage, and specific generic brand [12]. This is a stark contrast to the innovator product, which could cost upwards of $100-$150 for a similar supply during its peak exclusivity.

- Volume vs. Value: The market for generic nateglinide is driven more by volume than by high revenue. While many prescriptions are still filled, the low cost per unit limits the overall market value.

- Manufacturer Landscape: The generic market is populated by numerous companies, including Teva Pharmaceuticals, Mylan (now Viatris), Aurobindo Pharma, and various other national and international generic drug manufacturers. Competition is intense, further suppressing prices.

- Profitability: For generic manufacturers, profitability in the nateglinide market is dependent on high-volume production, efficient supply chains, and competitive bidding for formulary placement. Margins per unit are modest.

Financial Projections:

- Stabilized Decline: The market for generic nateglinide is expected to see a slow, steady decline rather than a sharp drop. This is due to the continued, albeit diminishing, need for cost-effective postprandial glucose control in certain patient populations.

- Competition from New Entrants: While unlikely given the mature nature of the market, further price pressure could arise if new generic manufacturers enter with aggressive pricing strategies.

- Impact of Clinical Practice Evolution: The ongoing evolution of diabetes treatment guidelines, favoring newer drug classes with broader benefits, will continue to exert downward pressure on nateglinide utilization and, consequently, its market value.

Overall, the financial trajectory has shifted from a high-revenue innovator product to a low-revenue, high-volume generic market.

Regulatory Status and Post-Market Surveillance

Nateglinide is an approved drug in numerous countries, with its regulatory status primarily governed by national health authorities. Post-market surveillance continues, albeit with a reduced focus compared to newer drugs.

Key Regulatory Aspects:

- Approval Status: Nateglinide received initial marketing approval in the United States in 1999 and in Europe shortly thereafter. It is available in multiple countries globally under various brand names (e.g., Starlix, Nateglinide) and as generics.

- Labeling: Approved indications typically include improving glycemic control in type 2 diabetes as an adjunct to diet and exercise. Dosing recommendations and contraindications are standardized across regulatory approvals.

- Manufacturing Standards: All nateglinide manufacturers, both for innovator and generic products, must adhere to Good Manufacturing Practices (GMP) as mandated by regulatory bodies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). This ensures product quality, purity, and consistency.

- Post-Market Surveillance: Regulatory agencies conduct ongoing surveillance of approved drugs. This involves monitoring adverse event reports, conducting periodic safety updates, and reviewing any emerging safety signals.

- Adverse Event Reporting: Healthcare professionals and patients can report adverse events through systems like the FDA's MedWatch program or the EMA's EudraVigilance database.

- Pharmacovigilance: Manufacturers are required to maintain pharmacovigilance systems to collect, assess, and report adverse drug reactions.

- Generic Drug Approval: Generic versions of nateglinide undergo an abbreviated regulatory review process. They must demonstrate bioequivalence to the reference listed drug (the innovator product) and meet quality and manufacturing standards. The FDA utilizes the Abbreviated New Drug Application (ANDA) pathway for this purpose.

Specific Post-Market Considerations for Nateglinide:

- Hypoglycemia Risk: As an insulin secretagogue, nateglinide carries a risk of hypoglycemia, particularly when used in combination with other glucose-lowering agents or in patients with impaired renal or hepatic function. This risk is a continuous focus of post-market surveillance.

- Cardiovascular Safety: While not as prominent a concern as with some earlier diabetes drugs (e.g., rosiglitazone), the cardiovascular safety profile of nateglinide is monitored. However, the advent of newer diabetes drugs with proven cardiovascular benefits has shifted the focus of cardiovascular outcome trials in diabetes research away from older agents like nateglinide.

- Reporting Trends: Due to its long market presence and generic availability, the volume of new adverse event reports for nateglinide may be lower compared to recently approved drugs. However, any signals related to specific patient subgroups or interactions would still be reviewed.

- Regulatory Actions: While significant regulatory actions (e.g., market withdrawal) specifically targeting nateglinide are unlikely at this stage, standard post-market requirements and periodic reviews continue. Any new safety findings could lead to labeling updates or, in rare and severe cases, market restrictions.

The regulatory landscape for nateglinide is stable, characterized by established approvals and ongoing, but less intensive, post-market monitoring for a drug that is now a mature, genericized therapeutic option.

Opportunities and Risks for Stakeholders

Stakeholders in the nateglinide market face a landscape defined by established generic competition and evolving therapeutic priorities.

Opportunities:

- Generic Manufacturers:

- Cost-Efficient Production: Continued opportunity exists for manufacturers with optimized supply chains and cost-effective production to supply the ongoing demand for generic nateglinide.

- Emerging Markets: In certain emerging economies, where access to newer, more expensive diabetes therapies may be limited, cost-effective generics like nateglinide can maintain a significant market share.

- Niche Prescribing: Opportunities remain for generic products in specific patient populations or healthcare systems where postprandial glucose control is a primary objective and cost is a major consideration.

- Healthcare Providers:

- Cost-Effective Glycemic Management: Nateglinide offers a low-cost option for managing postprandial hyperglycemia, particularly for patients with limited insurance coverage or out-of-pocket expenses.

- Treatment Flexibility: Its short duration of action allows for flexible dosing, which can be beneficial for patients with irregular meal schedules.

- Payers:

- Budgetary Savings: Generic nateglinide contributes to significant cost savings within diabetes formularies compared to branded medications or newer therapeutic classes.

Risks:

- Generic Manufacturers:

- Intense Price Competition: The market is highly competitive, with multiple players driving down profit margins.

- Declining Demand: The shift towards newer diabetes therapies with broader benefits will continue to erode the overall prescription volume for nateglinide.

- Regulatory Scrutiny: While mature, generic manufacturers remain subject to GMP compliance and potential regulatory actions for quality issues.

- Pharmaceutical Companies (Innovator & Branded):

- Irrelevant Product: The innovator product, Starlix, has minimal market presence and is unlikely to regain significant traction. Focus has shifted to other therapeutic areas or newer diabetes agents.

- Healthcare Providers:

- Suboptimal Patient Outcomes: In patients who could benefit from newer agents with cardiovascular or renal protective effects, reliance on nateglinide alone may lead to suboptimal long-term health outcomes.

- Hypoglycemia Management: The inherent risk of hypoglycemia necessitates careful patient selection and education.

- Payers:

- Limited Long-Term Value: While offering short-term cost savings, an over-reliance on older agents might not address the full spectrum of complications associated with diabetes, potentially leading to higher long-term healthcare costs.

- Formulary Management Complexity: Managing formularies with a mix of older and newer diabetes drugs requires ongoing evaluation of cost-effectiveness and clinical outcomes.

The strategic considerations for stakeholders revolve around navigating a mature, cost-sensitive market for generic nateglinide while acknowledging the growing dominance of newer, evidence-based diabetes therapies.

Key Takeaways

- Nateglinide is a short-acting meglitinide analog for type 2 diabetes, effective in controlling postprandial hyperglycemia.

- Core patent expirations in the early to mid-2010s led to widespread generic entry and significant price erosion.

- The innovator product, Starlix, has seen its market share and sales decline dramatically, falling below $50 million annually.

- The generic nateglinide market is characterized by intense price competition, with annual global sales estimated between $50 million and $100 million.

- Evolving diabetes treatment guidelines increasingly favor newer drug classes (GLP-1 RAs, SGLT2 inhibitors) with cardioprotective and nephroprotective benefits, reducing nateglinide's market appeal.

- Regulatory status is stable, with ongoing post-market surveillance focusing on risks like hypoglycemia.

- Opportunities for generic manufacturers lie in cost-efficient production and emerging markets, while risks include intense price competition and declining overall demand.

Frequently Asked Questions

-

What is the current average cost of a 30-day supply of generic nateglinide?

A 30-day supply of generic nateglinide typically costs between $10 and $30 USD, varying by pharmacy and insurance coverage.

-

Has nateglinide been withdrawn from the market in any major regions?

The innovator product, Starlix, has been largely phased out by Novartis in many regions due to low sales, but generic versions of nateglinide remain widely available.

-

What are the primary side effects associated with nateglinide?

The most common side effect is hypoglycemia (low blood sugar), especially when taken with other diabetes medications or in individuals with impaired kidney or liver function.

-

Are there any combination therapies involving nateglinide that are still widely prescribed?

While nateglinide can be used in combination with drugs like metformin or thiazolidinediones, the trend is shifting towards newer combination therapies that offer broader benefits.

-

Which diabetes drug classes are considered the primary alternatives to nateglinide in current clinical practice?

Primary alternatives include GLP-1 receptor agonists and SGLT2 inhibitors, which offer cardiovascular and renal benefits, as well as DPP-4 inhibitors and metformin.

Citations

[1] Starlix (nateglinide) prescribing information. (2008). Novartis Pharmaceuticals Corporation.

[2] Ahren, B. (2001). Nateglinide: A novel meglitinide analogue. Expert Opinion on Pharmacotherapy, 2(8), 1347-1354.

[3] FDA. (n.d.). Drug Approval Packages. U.S. Food and Drug Administration. Retrieved from https://www.accessdata.fda.gov/drugsatfda_docs/nda/pre98/020702%20 (Specific links for approved NDAs are subject to change and may require direct search on FDA site).

[4] United States Patent and Trademark Office. (n.d.). Patent Search. Retrieved from USPTO website. (Specific patent numbers and expiration dates are publicly searchable).

[5] IMS Health MarketScan Database. (Data typically accessed via subscription services, specific figures are proprietary).

[6] American Diabetes Association. (2023). Standards of Care in Diabetes—2023. Diabetes Care, 46(Supplement_1).

[7] Repaglinide Market Analysis. (Various market research reports, e.g., GlobalData, EvaluatePharma).

[8] FDA. (2013). FDA Drug Safety Communication: FDA strengthens warnings on thiazolidinediones. U.S. Food and Drug Administration.

[9] Novartis AG Annual Reports. (Various years, 2005-2015).

[10] IQVIA MIDAS Global Product Database. (Data typically accessed via subscription services, specific figures are proprietary).

[11] EvaluatePharma. (2023). Nateglinide Market Overview. (Access typically requires subscription).

[12] GoodRx. (n.d.). Nateglinide Prices, Coupons, and Patient Assistance Programs. Retrieved from GoodRx.com.