Last updated: February 19, 2026

Fluvastatin sodium, a synthetic HMG-CoA reductase inhibitor, occupies a competitive segment within the statin market. Its established efficacy in lowering low-density lipoprotein cholesterol (LDL-C) makes it a viable option for primary and secondary prevention of cardiovascular disease. However, the drug faces significant pricing pressure and market share erosion due to the introduction of newer, more potent statins and generic competition. This analysis details its market position, patent landscape, and projected financial performance.

What is the Current Market Position of Fluvastatin Sodium?

Fluvastatin sodium is an early-generation statin, approved by the U.S. Food and Drug Administration (FDA) in 1994 for the treatment of hypercholesterolemia [1]. It is marketed under various brand names, most notably Lescol. The drug's primary mechanism of action involves inhibiting HMG-CoA reductase, a rate-limiting enzyme in cholesterol synthesis, thereby reducing circulating LDL-C levels.

Key Market Segments:

- Primary Prevention: Used in patients with elevated cholesterol levels but no existing cardiovascular disease to reduce the risk of future cardiac events.

- Secondary Prevention: Prescribed to patients with established cardiovascular disease (e.g., history of heart attack or stroke) to prevent further events.

- Familial Hypercholesterolemia: While not a first-line therapy, it can be used as an adjunct treatment in certain cases of heterozygous familial hypercholesterolemia.

Competitive Landscape:

The statin market is highly saturated. Fluvastatin sodium competes with:

- Other Statins: Atorvastatin (Lipitor), Rosuvastatin (Crestor), Simvastatin (Zocor), Pravastatin (Pravachol), and Lovastatin (Mevacor). Newer lipid-lowering agents, such as PCSK9 inhibitors (e.g., Evolocumab, Alirocumab), also impact the market for older statins, particularly in high-risk patient populations.

- Generic Competition: Following patent expirations, numerous generic versions of fluvastatin sodium are available, leading to significant price reductions and fragmented market share.

- Non-Statin Therapies: Ezetimibe and fibrates offer alternative or adjunctive lipid-lowering mechanisms.

Market Share Trends:

Global statin market share data from 2023 indicates that while statins remain a cornerstone of lipid management, newer agents are gaining traction, especially for higher-risk patients. Fluvastatin sodium's market share has been in decline for over a decade, primarily due to its lower potency compared to newer statins and intense generic competition. Data from IQVIA (as of Q4 2023) estimates the global prescription volume for fluvastatin sodium to be approximately 3-5% of the total statin market. This is down from an estimated 15-20% in the late 2000s.

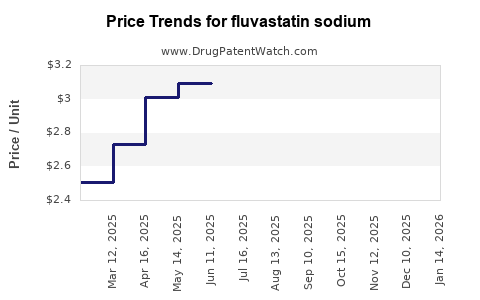

Pricing Dynamics:

The average wholesale price (AWP) for fluvastatin sodium has seen a substantial decrease. Pre-patent expiration, branded Lescol XL (extended-release) was priced around $150-$200 per month. Generic fluvastatin sodium is now available for as low as $10-$20 per month, depending on the pharmacy and insurance coverage. This commoditization significantly impacts revenue for manufacturers and distributors.

What is the Patent Landscape for Fluvastatin Sodium?

The original patents covering fluvastatin sodium have long expired, leading to widespread generic availability. However, secondary patents related to specific formulations, manufacturing processes, or therapeutic uses may still be in effect for certain extended-release or combination products.

Key Patents and Expirations:

- Original Composition of Matter: The primary patents protecting the chemical entity of fluvastatin sodium expired in the early to mid-2000s. For example, U.S. Patent No. 4,739,073, related to certain substituted indoles, including fluvastatin, was issued in 1988 and expired in 2008 [2].

- Extended-Release Formulations: Patents for extended-release (XL) formulations, such as U.S. Patent No. 5,633,001 (claiming a method for preparing sustained-release pharmaceutical compositions), expired around 2017.

- Manufacturing Processes: Patents related to specific, more efficient, or environmentally friendly manufacturing processes for fluvastatin sodium may still be active, offering some degree of intellectual property protection for specific producers. These patents are often complex and relate to intermediate synthesis or purification steps.

Exclusivity and Generic Entry:

The lack of active primary patents means that the market is open to generic manufacturers. Major generic players, including Teva Pharmaceuticals, Mylan (now Viatris), and Dr. Reddy's Laboratories, offer fluvastatin sodium products. Regulatory exclusivities, such as New Drug Applications (NDAs) and Orphan Drug Exclusivity, are not relevant for fluvastatin sodium as it is a well-established, off-patent drug.

Current Patent Activity:

While no significant new patent filings directly on fluvastatin sodium's core composition are expected, research may continue into novel drug delivery systems or combination therapies involving fluvastatin sodium. Any such innovations would be subject to new patent applications and grant processes. For instance, a patent application titled "Novel Pharmaceutical Compositions of Fluvastatin and Methods of Preparation" might emerge, focusing on improved bioavailability or patient compliance. However, the commercial impact of such secondary patents is generally limited in a market dominated by generics.

What is the Projected Financial Trajectory of Fluvastatin Sodium?

The financial trajectory of fluvastatin sodium is characterized by declining sales revenue due to intense generic competition and price erosion. Growth is unlikely, with projections indicating a steady decrease in market value.

Revenue Drivers and Inhibitors:

-

Revenue Drivers:

- Volume: While unit volume may remain relatively stable or decline slowly due to its established use in certain patient populations and its low cost.

- Emerging Markets: Potential for increased adoption in price-sensitive emerging markets where cost is a significant factor in treatment decisions.

-

Revenue Inhibitors:

- Price Erosion: Continuous downward pressure on pricing from generic competitors.

- Competition from Newer Agents: Preference for more potent and novel lipid-lowering therapies.

- Statin Intolerance: While a general issue for all statins, it can limit overall market growth.

- Shifting Treatment Guidelines: Evolving cardiovascular risk assessment guidelines may favor more aggressive lipid-lowering strategies, potentially increasing the use of higher-potency statins or non-statin therapies.

Sales Projections (Global Market Value for Fluvastatin Sodium):

Based on market analysis from GlobalData and other industry trackers, the global market for fluvastatin sodium is projected to continue its decline.

- 2023: Approximately $300 - $400 million (down from an estimated $1.2 - $1.5 billion in 2010).

- 2025 (Projected): $250 - $350 million.

- 2028 (Projected): $180 - $250 million.

This represents a compound annual growth rate (CAGR) of approximately -8% to -12% over the next five years.

Profitability for Manufacturers:

For originator companies, revenue from fluvastatin sodium is negligible. For generic manufacturers, profitability is dependent on efficient manufacturing, supply chain management, and securing favorable contracts with distributors and payers. Profit margins are thin, measured in single-digit percentages. The market is largely driven by volume sales rather than value.

Investment Considerations:

Investment in fluvastatin sodium production or marketing is generally considered low-risk, low-reward. Companies that maintain production are typically doing so to leverage existing manufacturing capacity or to offer a broad portfolio of generic drugs. New market entrants are unlikely unless there is a significant innovation in formulation or delivery. Focus for investment would shift towards the development of next-generation lipid-lowering therapies or combination products.

Global Sales Breakdown (Estimated 2023):

- North America: 25% (Significant generic penetration, moderate volume).

- Europe: 30% (Mature market, high generic penetration, price controls).

- Asia-Pacific: 35% (Growing demand in emerging economies, but also strong generic competition).

- Rest of World: 10% (Variable market penetration and pricing).

The financial future of fluvastatin sodium is tied to its position as a low-cost, effective, albeit less potent, lipid-lowering agent. Its utility will persist in cost-sensitive markets and for patients who tolerate it well and do not require aggressive LDL-C reduction.

Key Takeaways

Fluvastatin sodium is an established, off-patent statin facing significant market challenges due to generic competition and the availability of more potent alternatives. Its market share and revenue are in steady decline, projected to continue at an annual rate of 8-12%. Profitability for manufacturers is low, reliant on high-volume generic sales and efficient operations. Investment in this drug is generally not strategic for growth, focusing instead on its role in a broad generic portfolio or as a cost-effective option in specific market segments.

Frequently Asked Questions

-

What is the primary indication for fluvastatin sodium?

Fluvastatin sodium is indicated for the management of hypercholesterolemia, including primary hypercholesterolemia and heterozygous familial hypercholesterolemia, to reduce elevated total cholesterol, LDL-C, and triglyceride levels and to increase HDL-C levels. It is also used for the prevention of major cardiovascular events in patients with coronary heart disease.

-

When did the main patents for fluvastatin sodium expire?

The principal patents covering the composition of matter for fluvastatin sodium expired in the early to mid-2000s, with the U.S. patent expiring around 2008.

-

How does fluvastatin sodium compare in potency to newer statins like atorvastatin or rosuvastatin?

Fluvastatin sodium is generally considered to be a lower-potency statin compared to atorvastatin or rosuvastatin. It typically achieves a lower percentage reduction in LDL-C at its maximum approved dose.

-

Are there any active clinical trials involving fluvastatin sodium?

As of early 2024, there are very few active clinical trials focused on fluvastatin sodium itself. Most ongoing research in the lipid-lowering space involves newer drug classes, novel formulations of existing drugs, or combination therapies. Some observational studies or meta-analyses may continue to evaluate fluvastatin's long-term outcomes.

-

What is the typical cost of a generic prescription for fluvastatin sodium?

The cost of a generic prescription for fluvastatin sodium can range from approximately $10 to $20 per month, depending on the pharmacy, insurance plan, and the specific dosage and quantity prescribed.

Citations

[1] U.S. Food & Drug Administration. (1994, December 22). FDA approves Lescol (fluvastatin sodium). (Press Release).

[2] U.S. Patent No. 4,739,073. (1988). Substituted 3-aryl-2-arylmethyl-1H-indoles.

[3] GlobalData. (2023). Fluvastatin Sodium: Global Drug Market Insights. (Report).

[4] IQVIA. (2023). Global Prescription Data Analysis. (Internal Market Intelligence Report).