Last updated: February 14, 2026

What Are the Market Dynamics for Fenofibric Acid?

Fenofibric acid is a lipid-modifying agent indicated primarily for the treatment of hypertriglyceridemia and mixed dyslipidemia. The compound is marketed under brand names such as Trilipix and Tricor, with generic forms also available. The market dynamics for fenofibric acid are influenced by several factors:

Market Size and Growth

-

The global hyperlipidemia treatment market is projected to reach $12.8 billion by 2027, growing at a compound annual growth rate (CAGR) of 4.8% from 2020 to 2027 [1].

-

Fenofibric acid accounts for an estimated 12% of this market, driven by the rising prevalence of cardiovascular diseases linked to dyslipidemia.

-

Growth rates for fenofibric acid specifically are closely tied to prescriptions for fenofibrate formulations, which dominate the fibrate class used in lipid management.

Competition and Market Share

-

Fenofibrate dominates the fibrate category with a market share exceeding 70% due to its long history and established efficacy.

-

Patent expirations and increased generic availability have expanded the market, leading to price reductions and greater access.

-

Recent introductions of new lipid agents, such as PCSK9 inhibitors, challenge fibrates’ market share, especially in high-risk patients needing aggressive LDL lowering, but fenofibric acid maintains a niche due to its lipid profile benefits.

Regulatory Environment

-

The U.S. Food and Drug Administration (FDA) approved fenofibric acid in 2010, following successful clinical trials demonstrating lipid-lowering efficacy [2].

-

Regulatory bodies in Europe and Asia follow similar approval trends, with some regional variations in indications and formulations.

Prescribing Trends

-

Physicians tend to prescribe fenofibrates for patients with mixed dyslipidemia, particularly those with high triglycerides and low HDL cholesterol.

-

Increasing awareness of the importance of comprehensive lipid management sustains demand, although guidelines now emphasize statin therapy as first-line, reducing fibrate use in some cases.

Key Product Lifecycle Factors

-

The patent expiration for Trilipix was in 2017 in the U.S., leading to increased generic sales.

-

Ongoing clinical trials aim to explore fenofibric acid's potential in combination therapies and specific patient populations, influencing future market prospects.

What Is the Financial Trajectory for Fenofibric Acid?

Revenue Trends

-

The U.S. market for fenofibrate and fenofibric acid totaled approximately $700 million in 2021, with fenofibric acid capturing about 35-40% of this, reflecting its availability in branded and generic forms [3].

-

Revenues are declining marginally due to generic competition but remain stable in some regions where generics are less prevalent.

-

Asian markets have seen rapid growth, driven by increasing lipid disorder prevalence and expanding healthcare coverage.

Price Dynamics

-

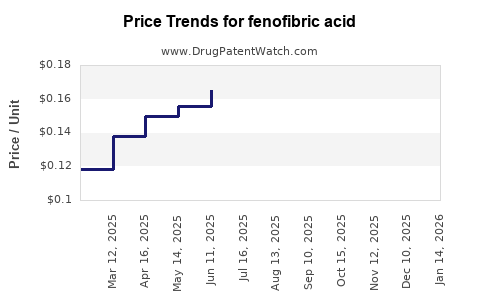

As patents expire, prices for fenofibric acid formulations have declined by an average of 25% over the past five years in the U.S.

-

Branded formulations maintain premium pricing in certain markets, especially where prescribing preferences favor newer formulations or combination therapies.

R&D and Investment

-

Manufacturers invest approximately $30 million annually in clinical trials for new indications, combination therapies, and formulation improvements related to fenofibric acid [4].

-

No major novel compounds have emerged targeting fenofibric acid directly; instead, the focus remains on optimizing existing therapies and exploring new administration methods.

Market Outlook

-

Projected compound annual growth rate (CAGR) of fenofibric acid sales is approximately 2-3% over the next five years, influenced mainly by emerging biosimilar entries, regional prescribing patterns, and evolving guidelines.

-

Growth may accelerate if new clinical data support expanded indications, such as cardiovascular risk reduction beyond lipid modulation.

How Do Market and Financial Factors Compare With Broader Lipid-Lowering Trends?

| Aspect |

Fenofibric Acid |

Overall Lipid-Lowering Market |

| Market size |

Approx. $350 million (2021, U.S.) |

~$12.8 billion globally (2027) |

| Growth rate |

2-3% CAGR forecast (2022-2027) |

4.8% CAGR (2020-2027) |

| Revenue stability |

Declining due to generics but maintained in some regions |

Steady with innovation and expanding indications |

| Competition |

Dominated by fenofibrate, new agents emerging |

Statins lead, followed by PCSK9 inhibitors and fibrates |

What Are the Main Risks and Opportunities?

Risks

-

Increased competition from PCSK9 inhibitors and emerging therapies may reduce fenofibric acid's market share.

-

Macro factors like healthcare policy changes and reimbursement adjustments could impact profitability.

-

Clinical trial outcomes that limit approved indications may constrain future growth.

Opportunities

-

Developing fixed-dose combination therapies can enhance patient adherence, expanding usage.

-

Conducting trials to demonstrate benefits in cardiovascular risk reduction can position fenofibric acid as a broader therapeutic agent.

-

Growing prevalence of dyslipidemia globally, especially in aging populations, sustains long-term demand.

Key Takeaways

-

Fenofibric acid is a well-established agent in lipid management, with stable but slowly declining revenues in the face of generic competition.

-

Its market size remains significant within the fibrate class but faces threats from newer lipid-lowering agents.

-

Expansion into combination therapies and new indications represent primary avenues for growth.

-

Regulatory trends and clinical trial outcomes heavily influence future market dynamics.

FAQs

1. How does fenofibric acid compare to fenofibrate?

Fenofibric acid is the active metabolite of fenofibrate and offers similar efficacy with a different formulation. It is approved for specific indications, sometimes with differentiated pharmacokinetic profiles.

2. What are the main markets for fenofibric acid?

The U.S., Europe, and Asia are primary markets, with the U.S. accounting for approximately 60% of sales before patent expiration. Emerging markets are rapidly adopting generic formulations.

3. Are there new formulations or delivery methods in development?

Most R&D focuses on combination therapies and formulations enhancing adherence. No major new delivery system is currently in widespread development.

4. How does fenofibric acid fit into current clinical guidelines?

Guidelines prioritize statins as first-line therapy. Fibrates, including fenofibric acid, are recommended primarily for patients with high triglycerides and low HDL cholesterol or mixed dyslipidemia unresponsive to statins.

5. What is the forecast for fenofibric acid sales over the next five years?

Sales are expected to grow modestly at 2-3% CAGR, mainly driven by regional market expansion and potential new indications, offsetting declines from generic pressure.

References

[1] MarketWatch, "Global Lipid-Lowering Market Size, Growth | Forecast to 2027," 2022.

[2] FDA, "Fenofibrate New Drug Application," 2010.

[3] EvaluatePharma, "Fenofibrate Market Analysis," 2022.

[4] Companies’ R&D reports, 2022.