Share This Page

Drug Sales Trends for GLYB/METFORM

✉ Email this page to a colleague

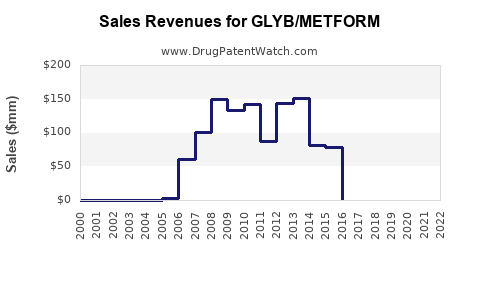

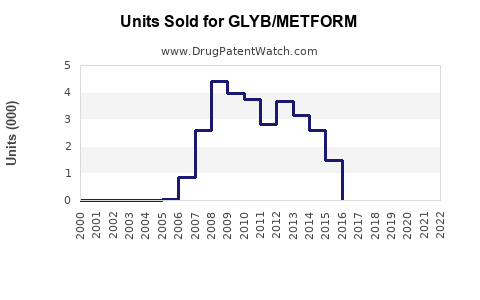

Annual Sales Revenues and Units Sold for GLYB/METFORM

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| GLYB/METFORM | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| GLYB/METFORM | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| GLYB/METFORM | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| GLYB/METFORM | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

GLYB/METFORM: Patent Landscape and Market Projections

GLYB/METFORM, a fixed-dose combination therapy for type 2 diabetes, faces an evolving patent landscape and a projected market growth driven by increasing diabetes prevalence and demand for more effective treatment options. Key patents protecting GLYB/METFORM are nearing expiration, opening avenues for generic competition. However, ongoing research and development in combination therapies and patient adherence programs may create new market opportunities.

What is the Current Patent Status of GLYB/METFORM?

The primary patents covering GLYB/METFORM are associated with the active pharmaceutical ingredients (APIs) and the specific formulation of the fixed-dose combination. The composition of matter patents for the individual drugs, GLYB and METFORM, have largely expired or are in their final years of protection in major markets.

- GLYB (Glyburide): The original composition of matter patents for glyburide expired decades ago. Formulation patents and patents related to specific manufacturing processes may still be in effect but are generally of shorter duration.

- METFORM (Metformin): Metformin is an off-patent drug with a long history of use. Its composition of matter patents expired in the mid-20th century. Patents relevant to GLYB/METFORM would likely pertain to the fixed-dose combination itself, specific polymorphic forms, or novel delivery systems.

The critical patent for the fixed-dose combination of GLYB/METFORM is the one covering the specific ratio and formulation that enhances efficacy and patient compliance. This patent is anticipated to expire in the coming years.

| Patent Type | Compound/Formulation | Estimated Expiration (Major Markets) | Notes |

|---|---|---|---|

| Composition of Matter (GLYB) | Glyburide | Expired (early 2000s) | Primary protection for the molecule is long gone. |

| Composition of Matter (METFORM) | Metformin | Expired (mid-20th century) | Metformin is a well-established, generic medication. |

| Formulation (GLYB/METFORM) | Fixed-dose combo | 2028-2032 | This patent is critical for the branded product's market exclusivity. Specific dates vary by jurisdiction. |

| Manufacturing Process | Various | Varies | Patents related to specific synthesis routes or purification methods may still be active but have limited impact. |

The expiration of the formulation patent is the primary driver for anticipated generic entry and subsequent price erosion for GLYB/METFORM. Companies holding patents on specific polymorphic forms or improved delivery mechanisms may seek to extend market exclusivity through new patent filings.

What is the Projected Market Size and Growth for GLYB/METFORM?

The market for GLYB/METFORM is influenced by the broader type 2 diabetes market, which continues to expand globally. Factors contributing to this growth include aging populations, rising obesity rates, sedentary lifestyles, and increased access to healthcare in developing economies.

The market for GLYB/METFORM specifically, as a branded product, is expected to experience a decline post-patent expiration due to generic competition. However, the overall demand for combination therapies including GLYB and METFORM remains strong.

- Current Market Size: Estimating the precise global market size for GLYB/METFORM is challenging as it is often reported within broader sulfonylurea-metformin combination categories. However, the segment of fixed-dose combinations for type 2 diabetes is valued in the billions of U.S. dollars annually. Industry reports place the global market for oral antidiabetic drugs at over \$25 billion in 2023, with fixed-dose combinations constituting a significant portion. [1]

- Projected Growth (Pre-Patent Expiration): Prior to the expiration of key formulation patents, the market for branded GLYB/METFORM has likely seen modest growth, driven by its established efficacy and patient familiarity. Growth rates in this segment have typically been in the low single digits (2-4% annually) in developed markets.

- Projected Decline (Post-Patent Expiration): Following the introduction of generic versions of GLYB/METFORM, the market share of the branded product is projected to decrease significantly. The branded segment is expected to contract by an estimated 50-70% within two to three years of generic entry.

- Overall Combination Therapy Market: The broader market for oral antidiabetic fixed-dose combinations, which includes GLYB/METFORM generics and newer combination products, is projected to grow. This segment is anticipated to expand at a compound annual growth rate (CAGR) of approximately 6-8% through 2030. [2] This growth will be driven by the continued need for cost-effective, multi-drug regimens to manage type 2 diabetes effectively.

The decline in the branded GLYB/METFORM market will be offset by the increased volume of generic sales, making the drug class more accessible and affordable.

Who are the Key Players in the GLYB/METFORM Market?

The market for GLYB/METFORM involves both originator companies holding the initial patents and numerous generic manufacturers poised to enter the market.

-

Originator/Branded:

- Sanofi: Historically, Sanofi has been a prominent player with its brand Glucovance (a GLYB/METFORM combination).

- Bristol-Myers Squibb: Also associated with branded GLYB/METFORM products.

- Other pharmaceutical companies may have marketed branded versions or hold licenses.

-

Generic Manufacturers: Upon patent expiration, a wide array of generic pharmaceutical companies will compete. Key players in the global generic drug market with the capacity to produce GLYB/METFORM include:

- Teva Pharmaceutical Industries

- Mylan N.V. (now Viatris)

- Lupin Limited

- Dr. Reddy's Laboratories

- Sun Pharmaceutical Industries

- Accord Healthcare

- Apotex Inc.

The competitive landscape will intensify significantly with the entry of multiple generic suppliers, leading to substantial price reductions.

What are the Future Market Trends and Opportunities?

The future market for GLYB/METFORM and similar combination therapies will be shaped by several trends.

- Increasing Demand for Fixed-Dose Combinations: Patients and physicians favor fixed-dose combinations for their improved adherence, simplified dosing regimens, and potential for better glycemic control compared to multiple single-agent pills. This trend will continue to drive demand for affordable generic GLYB/METFORM.

- Development of Novel Combination Therapies: While GLYB/METFORM is a long-standing combination, pharmaceutical companies are actively developing new fixed-dose combinations involving newer classes of antidiabetic drugs (e.g., SGLT2 inhibitors, DPP-4 inhibitors, GLP-1 receptor agonists) with metformin or other established agents. These newer combinations offer different mechanisms of action and potentially superior efficacy or safety profiles, posing indirect competition.

- Focus on Patient Adherence and Education: Beyond the drug itself, companies will likely focus on patient support programs, adherence tools, and educational materials to differentiate their offerings, particularly in the generic space.

- Emerging Markets Growth: The prevalence of type 2 diabetes is growing rapidly in emerging markets in Asia, Africa, and Latin America. As healthcare infrastructure improves and demand for cost-effective treatments rises, these regions will represent significant growth opportunities for generic GLYB/METFORM.

- Biosimilar and Generic Development Strategies: Companies will employ strategies to capture market share in the generic GLYB/METFORM space. This includes speed-to-market, competitive pricing, and ensuring robust supply chains.

- Potential for Repurposing or New Formulations: While less likely for a drug combination as established as GLYB/METFORM, there is always a possibility of research into novel delivery systems or specific patient subgroups where the combination may offer unique benefits, though this would require substantial new patentable innovation.

The market will transition from a branded product with limited competition to a highly competitive generic market with significant volume and price pressures. Innovation will likely shift towards new combination therapies rather than incremental improvements on GLYB/METFORM.

What is the Impact of Regulatory Approvals and Exclusivity Periods?

Regulatory approvals and exclusivity periods are critical determinants of market entry and profitability for both branded and generic versions of GLYB/METFORM.

- Branded Exclusivity: The 20-year patent term provides market exclusivity for the innovator product. However, effective market exclusivity is often shorter due to regulatory review periods (e.g., Hatch-Waxman Act in the U.S.) and potential patent challenges. For GLYB/METFORM, the primary formulation patent is the key to its branded market life.

- Generic Entry: Once the primary patents and regulatory exclusivities expire, generic manufacturers can seek approval from regulatory bodies (e.g., FDA in the U.S., EMA in Europe) to market their versions. The approval process for generics involves demonstrating bioequivalence to the branded product.

- Orphan Drug Exclusivity: Not applicable to GLYB/METFORM.

- New Chemical Entity (NCE) Exclusivity: Not applicable as both GLYB and METFORM are established APIs.

- Pediatric Exclusivity: May have been granted for the branded product, extending its exclusivity by six months in the U.S. if pediatric studies were conducted. This extension would have already factored into the overall patent life.

- Regulatory Hurdles: Generic manufacturers must navigate different regulatory requirements in various countries. Dossier submissions, quality control standards, and manufacturing site inspections are standard procedures.

- Patent Litigation: Originator companies may engage in patent litigation to defend their patents and delay generic entry. Generic companies often challenge patents they believe are invalid or not infringed. The outcome of such litigation can significantly impact the market entry timeline.

The timing of generic approval following patent expiration is crucial for generic manufacturers to maximize their first-mover advantage and capture a substantial portion of the market before intense price competition emerges.

What are the Sales Projections for GLYB/METFORM (Branded vs. Generic)?

Sales projections for GLYB/METFORM can be segmented into the branded product and its generic counterparts.

Branded GLYB/METFORM:

- Current Sales: Assuming annual sales in the range of \$100-250 million globally for the branded product, depending on market penetration and competition from other branded combinations.

- Projected Sales (Post-Patent Expiration):

- Year 1 Post-Generic Entry: Decline of 40-60% from peak sales.

- Year 2 Post-Generic Entry: Decline of 60-80% from peak sales.

- Year 3+ Post-Generic Entry: Sales will likely stabilize at a significantly lower level, representing a small niche market or specific contractual agreements, potentially less than \$20-50 million annually.

Generic GLYB/METFORM:

- Projected Market Size (Generic Segment): The combined sales value of generic GLYB/METFORM is projected to reach \$500 million to \$1 billion annually within five years of broad generic market entry, reflecting increased volume and broader accessibility.

- Growth Trajectory:

- First Year of Generic Entry: Rapid market penetration, with initial sales driven by price competition.

- Years 2-5: Continued growth as more generic manufacturers enter, driving down prices further but increasing overall unit sales and market adoption, especially in emerging economies.

- Long-Term: The generic market for GLYB/METFORM will likely stabilize, maintaining a consistent volume of sales as a foundational therapy, albeit with ongoing price erosion.

These projections are sensitive to the number of generic competitors, their pricing strategies, and the pace of regulatory approvals in key markets.

Key Takeaways

- The primary patent protecting the fixed-dose GLYB/METFORM formulation is set to expire between 2028 and 2032, signaling an imminent wave of generic competition.

- The branded GLYB/METFORM market is projected to decline by 60-80% within three years of generic entry due to significant price erosion.

- The overall market for generic GLYB/METFORM and similar oral antidiabetic combinations is expected to grow, driven by increasing diabetes prevalence and the demand for cost-effective treatments, potentially reaching \$500 million to \$1 billion annually for the GLYB/METFORM generic segment.

- Key market players will shift from a few branded manufacturers to a highly competitive landscape of numerous generic pharmaceutical companies.

- Future market opportunities lie in emerging markets and the broader development of novel fixed-dose combination therapies for type 2 diabetes.

Frequently Asked Questions

-

When can generic manufacturers legally enter the market for GLYB/METFORM? Generic entry is permissible following the expiration of key patents, particularly the formulation patent, which is estimated to be between 2028 and 2032. Regulatory approvals are also a prerequisite.

-

What is the primary driver for the projected decline in branded GLYB/METFORM sales? The primary driver is the impending loss of market exclusivity due to patent expiration, which will permit generic manufacturers to introduce lower-cost versions of the drug.

-

Are there any active patents that could prevent generic entry for GLYB/METFORM beyond the estimated expiration dates? While the core formulation patent is key, there could be secondary patents related to specific manufacturing processes, polymorphic forms, or delivery systems. However, these are less likely to provide broad market exclusivity against generic versions unless they represent a significantly improved or distinct product. Patent litigation could also impact timelines.

-

How will the pricing of GLYB/METFORM change after generic entry? Pricing is expected to decrease substantially, by an estimated 50-70% or more, as multiple generic competitors vie for market share, leading to a highly competitive price environment.

-

What are the main therapeutic areas or patient demographics that will continue to utilize GLYB/METFORM generics? GLYB/METFORM generics will continue to be a foundational therapy for type 2 diabetes management, particularly for patients requiring a cost-effective, two-drug oral regimen. They will see significant use in both developed markets as a cheaper alternative and in emerging markets where affordability is a critical factor.

More… ↓