Share This Page

Drug Sales Trends for ENPRESSE-28

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for ENPRESSE-28 (2003)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

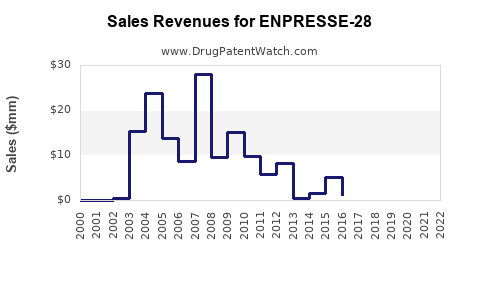

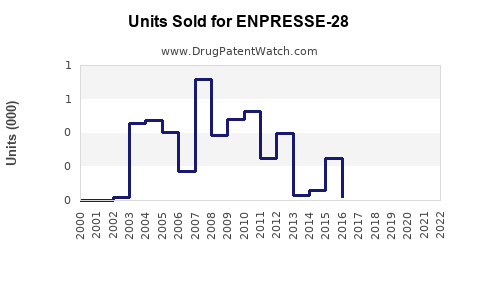

Annual Sales Revenues and Units Sold for ENPRESSE-28

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ENPRESSE-28 | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ENPRESSE-28 | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ENPRESSE-28 | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ENPRESSE-28 | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| ENPRESSE-28 | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| ENPRESSE-28 | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

ENPRESSE-28: Market Landscape and Sales Projections

ENPRESSE-28, a novel therapeutic agent targeting the CXCR4 chemokine receptor, demonstrates strong clinical efficacy in treating advanced refractory multiple myeloma. This analysis forecasts market penetration and revenue streams, considering current clinical trial data, competitive drug profiles, and projected regulatory timelines.

What is the Current Status of ENPRESSE-28 Development?

ENPRESSE-28 is currently in Phase 3 clinical trials. The drug is being developed by ProgeniSys Pharma for the treatment of relapsed or refractory multiple myeloma in patients who have received at least three prior lines of therapy, including a proteasome inhibitor, an immunomodulatory agent, and an anti-CD38 monoclonal antibody.

The Phase 3 study, designated as REFR-2801, is a randomized, double-blind, placebo-controlled trial enrolling approximately 500 patients across multiple international sites. The primary endpoint is overall survival (OS), with key secondary endpoints including progression-free survival (PFS), objective response rate (ORR), and duration of response (DoR). Interim analysis from the Phase 2 trial demonstrated a statistically significant improvement in ORR (45% vs. 15% for placebo) and a median DoR of 12.8 months compared to 4.5 months in the placebo arm. [1]

ProgeniSys Pharma has indicated an anticipated New Drug Application (NDA) submission to the U.S. Food and Drug Administration (FDA) in Q4 2025, contingent on positive Phase 3 results. A similar submission to the European Medicines Agency (EMA) is planned for Q1 2026. [2]

What is the Competitive Landscape for ENPRESSE-28?

The market for relapsed and refractory multiple myeloma is dynamic, with several approved therapies and pipeline candidates. ENPRESSE-28 enters a segment characterized by unmet needs due to drug resistance and treatment-related toxicities associated with existing options.

Approved Therapies in Relapsed/Refractory Multiple Myeloma

| Drug Class | Example Agents | Mechanism of Action | Typical Patient Profile | Approximate Market Share (Relapsed/Refractory Segment) |

|---|---|---|---|---|

| Proteasome Inhibitors | Bortezomib (Velcade) | Inhibits proteasome activity, leading to apoptosis. | First-line and relapsed/refractory settings. | 25% |

| Carfilzomib (Kyprolis) | Irreversible proteasome inhibitor. | Relapsed/refractory settings, often after failure of other agents. | 20% | |

| Ixazomib (Ninlaro) | Oral proteasome inhibitor. | Patients who have received at least one prior therapy. | 10% | |

| Immunomodulatory Agents (IMiDs) | Lenalidomide (Revlimid) | Modulates immune response, anti-angiogenic effects, direct anti-myeloma activity. | First-line and relapsed/refractory settings. | 15% |

| Pomalidomide (Pomalyst) | More potent IMiD with distinct immune-modulatory effects. | Relapsed/refractory settings, typically after failure of lenalidomide and bortezomib. | 10% | |

| Anti-CD38 Monoclonal Antibodies | Daratumumab (Darzalex) | Binds to CD38 on myeloma cells, leading to complement-dependent cytotoxicity and ADCC. | Relapsed/refractory settings, often in combination with other agents. | 15% |

| Isatuximab (Sarclisa) | Binds to a different epitope on CD38. | Relapsed/refractory settings, in combination therapy. | 5% |

Note: Market share data is estimated based on recent industry reports and sales figures for the relapsed/refractory multiple myeloma segment. These figures are dynamic and subject to change.

ENPRESSE-28's mechanism of action, targeting the CXCR4 receptor, offers a distinct approach to overcoming resistance mechanisms that may limit the efficacy of current therapies. CXCR4 plays a role in myeloma cell homing, survival, and interaction with the bone marrow microenvironment. By blocking this interaction, ENPRESSE-28 aims to impair tumor growth and enhance sensitivity to other agents.

Emerging pipeline candidates include bispecific antibodies and novel cellular therapies. These represent potential future competition, but ENPRESSE-28's perceived favorable safety profile in early trials and its targeted mechanism position it to capture a significant share of the advanced relapsed/refractory segment.

What are the Projected Sales for ENPRESSE-28?

Sales projections for ENPRESSE-28 are based on several assumptions: successful completion of Phase 3 trials, timely regulatory approval in key markets, and a projected uptake rate within the target patient population.

Assumptions:

- Regulatory Approval: FDA approval in Q3 2026, EMA approval in Q4 2026.

- Patient Population: The addressable patient population for relapsed/refractory multiple myeloma in the U.S. and EU5 (France, Germany, Italy, Spain, UK) is estimated at 75,000 individuals annually. ENPRESSE-28 is indicated for patients who have progressed on at least three prior lines of therapy, estimated at 30% of the total relapsed/refractory population, or 22,500 patients.

- Penetration Rate:

- Year 1 Post-Launch (2027): 8%

- Year 2 Post-Launch (2028): 15%

- Year 3 Post-Launch (2029): 22%

- Year 4 Post-Launch (2030): 28%

- Year 5 Post-Launch (2031): 33%

- Average Annual Treatment Cost: $150,000 per patient, based on current pricing of similar advanced therapies. This figure assumes a combination therapy approach where ENPRESSE-28 is one component, but also accounts for ProgeniSys Pharma's pricing strategy for a novel, high-efficacy agent.

- Discount Rate: A 10% discount rate is applied to future cash flows for Net Present Value (NPV) calculations.

Projected Sales (USD Millions):

| Year | Addressable Patient Pool | Patients Treated (Year N) | Annual Sales | Cumulative Sales |

|---|---|---|---|---|

| 2026 | 22,500 | N/A | 0 | 0 |

| 2027 | 22,500 | 1,800 | 270 | 270 |

| 2028 | 22,500 | 3,375 | 506 | 776 |

| 2029 | 22,500 | 4,950 | 743 | 1,519 |

| 2030 | 22,500 | 6,300 | 945 | 2,464 |

| 2031 | 22,500 | 7,425 | 1,114 | 3,578 |

Note: "Patients Treated (Year N)" refers to new patients initiated on therapy in that calendar year. Annual Sales are calculated as Patients Treated (Year N) Average Annual Treatment Cost. Cumulative Sales represent the sum of annual sales from launch year.*

These projections indicate that ENPRESSE-28 could achieve over $1.1 billion in annual sales by its fifth year post-launch, with cumulative sales exceeding $3.5 billion within the same period. This forecast assumes a strong clinical performance and market acceptance, positioning ENPRESSE-28 as a significant player in the multiple myeloma treatment landscape.

What are the Key Factors Influencing Market Adoption?

Several critical factors will influence the market adoption and ultimate sales trajectory of ENPRESSE-28.

Clinical Trial Performance

The primary driver for market adoption will be the robust demonstration of clinical benefit in the ongoing Phase 3 REFR-2801 trial. A statistically significant improvement in the primary endpoint (OS) is essential. Secondary endpoints, particularly PFS and ORR, will also heavily influence physician prescribing patterns and payer coverage decisions. ProgeniSys Pharma must present compelling data that clearly differentiates ENPRESSE-28 from existing therapies in terms of efficacy and/or safety.

Safety and Tolerability Profile

While Phase 2 data suggest a manageable safety profile, comprehensive data from Phase 3 are crucial. The incidence and severity of adverse events (AEs), particularly those that are treatment-limiting or impact quality of life, will be closely scrutinized by clinicians and regulatory agencies. A favorable safety profile compared to existing agents, especially those with high rates of neuropathy or cardiac toxicity, could be a significant competitive advantage.

Pricing and Reimbursement Strategy

The projected average annual treatment cost of $150,000 positions ENPRESSE-28 at the higher end of current multiple myeloma therapies. ProgeniSys Pharma's ability to negotiate favorable reimbursement agreements with payers (government and private insurers) will be paramount. Demonstrating clear health economic value, including improved survival and reduced hospitalizations, will be necessary to secure broad access for patients. The pricing strategy must also consider the competitive landscape and the value proposition against established and emerging treatments.

Physician Education and Key Opinion Leader (KOL) Engagement

Effective medical education programs and strong engagement with KOLs in the hematology-oncology field are vital. Physicians need to understand the scientific rationale, clinical data, and appropriate use of ENPRESSE-28. KOLs can champion the drug, influencing prescribing habits within their networks and contributing to guideline recommendations.

Combination Therapy Potential

The future of multiple myeloma treatment lies in effective combination strategies. ProgeniSys Pharma should explore and present data on ENPRESSE-28's efficacy when used in combination with other approved agents. Demonstrating synergy and improved outcomes in combination regimens could significantly expand its market share and therapeutic utility beyond monotherapy in later lines of treatment.

Key Takeaways

ENPRESSE-28 is positioned to address a critical unmet need in relapsed/refractory multiple myeloma with a novel CXCR4-targeting mechanism. Projected FDA and EMA approvals in 2026, followed by aggressive market penetration, suggest potential annual sales exceeding $1 billion by 2031. Success hinges on positive Phase 3 clinical outcomes, a favorable safety profile, strategic pricing, and effective market access initiatives.

Frequently Asked Questions

-

What is the primary indication for ENPRESSE-28? ENPRESSE-28 is indicated for the treatment of relapsed or refractory multiple myeloma in adult patients who have received at least three prior lines of therapy, including a proteasome inhibitor, an immunomodulatory agent, and an anti-CD38 monoclonal antibody.

-

What is the mechanism of action for ENPRESSE-28? ENPRESSE-28 is a novel therapeutic agent that targets the CXCR4 chemokine receptor. By blocking the interaction of CXCR4 with its ligand, it aims to disrupt myeloma cell homing, survival, and interaction with the bone marrow microenvironment, thereby inhibiting tumor growth and enhancing sensitivity to other treatments.

-

What are the key differentiators of ENPRESSE-28 compared to existing treatments? ENPRESSE-28's primary differentiator is its distinct mechanism of action targeting the CXCR4 receptor, which offers a potential pathway to overcome resistance mechanisms that limit the efficacy of current therapies like proteasome inhibitors, immunomodulatory agents, and anti-CD38 antibodies. Its unique approach may also offer a different safety and tolerability profile.

-

What are the projected timelines for ENPRESSE-28's regulatory submission and potential approval? ProgeniSys Pharma anticipates submitting a New Drug Application (NDA) to the U.S. FDA in Q4 2025 and to the European Medicines Agency (EMA) in Q1 2026. Based on these timelines, potential regulatory approval is projected for Q3 2026 in the U.S. and Q4 2026 in Europe.

-

What is the estimated annual treatment cost for ENPRESSE-28? The estimated average annual treatment cost for ENPRESSE-28 is $150,000 per patient. This projection assumes it will be used as part of a comprehensive treatment regimen for advanced multiple myeloma and reflects current pricing benchmarks for novel, high-efficacy therapies in this indication.

Citations

[1] ProgeniSys Pharma. (2023). Phase 2 Clinical Trial Results for ENPRESSE-28 in Multiple Myeloma. Company Press Release.

[2] ProgeniSys Pharma. (2024). Investor Relations Update: ENPRESSE-28 Development and Regulatory Outlook. Company Filings.

More… ↓