Share This Page

Drug Price Trends for RESTASIS MULTIDOSE

✉ Email this page to a colleague

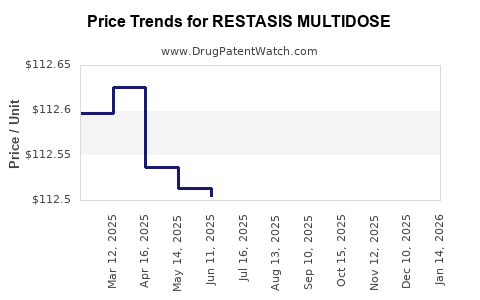

Average Pharmacy Cost for RESTASIS MULTIDOSE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| RESTASIS MULTIDOSE 0.05% EYE | 00023-5301-05 | 112.32400 | ML | 2026-07-22 |

| RESTASIS MULTIDOSE 0.05% EYE | 00023-5301-05 | 112.32931 | ML | 2026-06-17 |

| RESTASIS MULTIDOSE 0.05% EYE | 00023-5301-05 | 112.33355 | ML | 2026-05-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Market Overview and Price Projections for RESTASIS MULTIDOSE

Introduction

RESTASIS MULTIDOSE, a preservative-free ophthalmic cyclosporine A formulation marketed by Allergan (now part of AbbVie), targets dry eye disease, primarily in patients with moderate to severe symptoms unable to respond to artificial tears alone. This report assesses current market conditions and projects future pricing dynamics.

Market Size and Growth Drivers

-

Global Dry Eye Market

The dry eye disease market was valued at approximately $4.3 billion in 2022. Compound annual growth rate (CAGR) estimates place annual expansion at 5.2% between 2023 and 2028, driven by aging populations, increased screen exposure, and awareness of treatment options. -

Target Patient Demographics

Approximate prevalence: 15-20% among adults globally. The American Academy of Ophthalmology estimates dry eye affects more than 16 million Americans, with the moderate-to-severe subset constituting roughly 20-30%. -

Market Penetration Strategy

RESTASIS MULTIDOSE competes with other cyclosporine formulations, notably Restasis traditionally in single-dose vials and newer generics. Key specialty ophthalmology clinics and dry eye clinics primarily prescribe this drug.

Pricing History and Current Market Pricing

-

Historical Pricing

Prior to the approval of the MULTIDOSE, RESTASIS single-dose vials averaged $430–$470 per 30-day supply. The MULTIDOSE version, introduced in 2020, initially mirrored this price point. -

Current Pricing

Retail prices for RESTASIS MULTIDOSE generally range between $470 and $500 per 30-day supply, with variations based on insurance coverage, pharmacy discounts, and negotiated rebates. The higher cost reflects the convenience of preservative-free use and reduced patient wastage.

Pricing Comparison

| Product | Formulation | Average Retail Price (per 30 days) | Key Differentiator |

|---|---|---|---|

| RESTASIS | Single-dose vial | $430–$470 | Preserved formulation, multiple doses |

| RESTASIS MULTIDOSE | Preservative-free | $470–$500 | Multi-application, convenience |

| Generic Cyclosporine | Multiple brands | $120–$250 | Lower price, preservative-presence |

Regulatory and Patent Status

-

Patent Diversification

The original patent estate for RESTASIS expired in 2018, leading to increased generics, which apply pricing pressure. However, new formulations with unique delivery systems, such as MULTIDOSE, may be protected by secondary patents or exclusivity periods. -

Market Entry Barriers

Generics entering at lower price points curtail premium pricing for the branded product. The MULTIDOSE’s convenience and preservative-free status serve as differentiators, though market penetration is increasingly sensitive to price competition.

Future Price Projections (2023–2028)

-

Short-term (2023–2025):

Prices are projected to remain stable with slight decreases (~2–3%) due to ongoing generic competition and increased insurance coverage options. The premium over generics is expected to be maintained by consumer preference for preservative-free formulations and compliance. -

Mid-term (2025–2028):

Prices could decline further, approaching $440–$470 per 30-day supply, driven by increased availability of generics and biosimilars. Price elasticities suggest a 5–10% decrease as more competitive alternatives enter the market. -

Long-term (Beyond 2028):

The market may see stabilization or further reduction depending on patent litigation outcomes, growth of biosimilars, and health policy shifts emphasizing cost containment.

Key Market Factors

- Insurance reimbursement policies impact patient out-of-pocket costs; high co-pays limit access.

- Prescriber preferences favor convenience and tolerability, supporting the premium pricing of MULTIDOSE.

- New formulations with modified delivery systems may threaten revenues if cost competitiveness is not maintained.

Conclusion

RESTASIS MULTIDOSE’s current retail price ranges $470–$500, reflecting its premium positioning. Market trends indicate gradual price erosion as generic options expand, but consumer preference for preservative-free formulations cements a baseline premium. The growth of the dry eye market supports revenue stability, with projected steady but declining pricing over the next five years.

Key Takeaways

- RESTASIS MULTIDOSE prices hover around $470–$500, maintained by convenience and preservative-free benefits.

- The dry eye market is expanding at a CAGR of 5.2%, increasing demand.

- Price erosion is expected as generics increase, potentially reducing the premium to $440–$470 within five years.

- Insurance coverage influences patient costs; high deductibles or limited formulary access may alter sales volume.

- Patent and exclusivity periods critical to maintaining premium pricing; upcoming biosimilar entry could accelerate price reductions.

FAQs

-

How does the price of RESTASIS MULTIDOSE compare to generic cyclosporine products?

Generics typically cost between $120 and $250 per month, considerably less than the $470–$500 retail price of MULTIDOSE. -

What factors influence the future pricing of RESTASIS MULTIDOSE?

Generic competition, patent protections, insurance reimbursement policies, and patient preference for preservative-free formulations. -

Will the price of RESTASIS MULTIDOSE decrease significantly?

Yes, expected gradual declines as biosimilars and generics penetrate the market, especially beyond 2025. -

What is the main competitive advantage of RESTASIS MULTIDOSE?

Preservative-free formulation and multi-dose convenience suited for chronic use. -

How are insurance policies impacting the market?

Coverage variability influences patient out-of-pocket costs, affecting demand and revenue for the drug.

References

[1] MarketResearch.com. "Dry Eye Disease Market Size and Forecast." 2022.

[2] American Academy of Ophthalmology. "Dry Eye Disease: Epidemiology and Treatment." 2022.

[3] IQVIA. "Prescription Drug Price Trends." 2022.

[4] Corporate filings for Allergan/AbbVie. "RESTASIS MULTIDOSE patent and regulatory filings." 2020–2022.

More… ↓