Share This Page

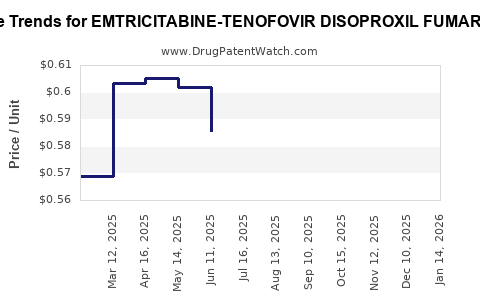

Drug Price Trends for EMTRICITABINE-TENOFOVIR DISOPROXIL FUMARATE

✉ Email this page to a colleague

Average Pharmacy Cost for EMTRICITABINE-TENOFOVIR DISOPROXIL FUMARATE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| EMTRICITABINE-TENOFOVIR DISOPROXIL FUMARATE 200-300 MG TAB | 00904-7172-07 | 0.45662 | EACH | 2026-06-17 |

| EMTRICITABINE-TENOFOVIR DISOPROXIL FUMARATE 200-300 MG TAB | 82009-0109-30 | 0.45662 | EACH | 2026-06-17 |

| EMTRICITABINE-TENOFOVIR DISOPROXIL FUMARATE 200-300 MG TAB | 42385-0953-30 | 0.45662 | EACH | 2026-06-17 |

| EMTRICITABINE-TENOFOVIR DISOPROXIL FUMARATE 200-300 MG TAB | 16714-0534-01 | 0.45662 | EACH | 2026-06-17 |

| EMTRICITABINE-TENOFOVIR DISOPROXIL FUMARATE 200-300 MG TAB | 00093-7704-56 | 0.45662 | EACH | 2026-06-17 |

| EMTRICITABINE-TENOFOVIR DISOPROXIL FUMARATE 200-300 MG TAB | 33342-0106-07 | 0.45662 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

EMTRICITABINE-TENOFOVIR DISOPROXIL FUMARATE: Market Dynamics and Price Forecasts

Emtricitabine-tenofovir disoproxil fumarate (FTC/TDF), a fixed-dose combination antiviral medication, is a cornerstone treatment for HIV-1 infection. Its efficacy in suppressing viral load, improving CD4 counts, and preventing mother-to-child transmission has cemented its market position. This analysis projects market growth and price trends based on patent expiry, generic competition, and evolving treatment guidelines.

What is the current market size and growth trajectory for FTC/TDF?

The global market for FTC/TDF is substantial, driven by the persistent global HIV/AIDS epidemic and its classification as a first-line antiretroviral therapy (ART) by major health organizations. In 2022, the market was valued at approximately \$6.8 billion, with an anticipated compound annual growth rate (CAGR) of 3.5% from 2023 to 2028. This growth is underpinned by increasing access to HIV treatment in low- and middle-income countries and the sustained demand for combination therapies.

Key Market Drivers:

- Global HIV Burden: The World Health Organization (WHO) estimates that 38.4 million people were living with HIV in 2021, requiring ongoing treatment. [1]

- Treatment Guidelines: FTC/TDF remains a recommended regimen in numerous international and national HIV treatment guidelines due to its favorable efficacy and safety profile, particularly in resource-limited settings.

- Prophylaxis (PrEP): Its use as pre-exposure prophylaxis (PrEP) for individuals at high risk of HIV acquisition is expanding, adding to market demand.

- Generic Availability: While branded versions remain significant, the increasing availability of generic FTC/TDF has expanded access and driven volume growth, albeit with pressure on overall revenue for originator products.

Market Segmentation by Region:

The market for FTC/TDF is distributed globally, with significant contributions from:

- North America: Holds a substantial share due to established healthcare infrastructure and high ART adherence rates.

- Europe: Another key market with strong public health initiatives for HIV management.

- Asia-Pacific: Expected to exhibit the highest growth rate, driven by expanding access to treatment and increasing HIV prevalence in certain nations.

- Sub-Saharan Africa: Represents a critical market for volume, though pricing pressures are more pronounced due to public health programs and the prevalence of generic options.

What is the patent landscape for FTC/TDF and its implications?

The patent landscape for FTC/TDF is a critical factor influencing market competition and pricing. The primary patents covering the active pharmaceutical ingredients (APIs) and their combination have either expired or are nearing expiration in major markets.

Key Patents and Expiries:

- Emtricitabine (FTC) and Tenofovir Disoproxil Fumarate (TDF) Compound Patents: These fundamental patents have largely expired in key markets like the United States and Europe. For instance, patents related to emtricitabine's synthesis and use expired in the early 2020s. [2]

- Formulation Patents: Patents protecting specific formulations of the FTC/TDF combination have also seen expiration. This has been a crucial period for generic manufacturers to enter the market.

- Evergreening Attempts: While core patents have expired, patent holders may have pursued secondary patents for novel formulations, delivery methods, or new indications. However, the impact of these secondary patents on the broad FTC/TDF market has been limited as generic versions of the original combination are widely available.

- Orphan Drug Exclusivity: This does not apply to FTC/TDF as it is not designated for rare diseases.

- Data Exclusivity: This provides a period of market exclusivity for approved drugs, independent of patent protection. In the US, this is typically 5 years for new drug applications. However, for products like FTC/TDF, which have been on the market for an extended period, this exclusivity has long since passed.

The expiration of primary patents has opened the door for generic competition, which has significantly altered the market dynamics and pricing.

How is generic competition impacting the FTC/TDF market?

The entry of generic FTC/TDF has been a transformative event, leading to increased accessibility and reduced treatment costs. This competition is characterized by a multi-player landscape.

Generic Market Dynamics:

- Price Erosion: The most significant impact of generic entry is substantial price erosion. Branded FTC/TDF, once commanding premium pricing, now faces intense competition from generics priced considerably lower.

- Increased Volume: Lower prices have facilitated wider adoption, particularly in emerging markets and public health programs. This has led to an overall increase in the volume of FTC/TDF consumed globally, even as the revenue generated by originator companies has declined.

- Key Generic Players: Numerous pharmaceutical companies have launched generic versions of FTC/TDF. Major players include Teva Pharmaceutical Industries, Mylan (now Viatris), Sun Pharmaceutical Industries, Aurobindo Pharma, and Cipla.

- Competitive Bidding: In large tenders, especially from governmental health organizations and NGOs, FTC/TDF prices are often subject to aggressive competitive bidding, further driving down costs.

- Quality and Bioequivalence: Regulatory agencies worldwide, such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), ensure that generic FTC/TDF products are bioequivalent to the originator drug, meeting stringent quality standards.

This competitive environment has been crucial in achieving global health goals for HIV treatment access.

What are the price projections for FTC/TDF over the next five years?

Price projections for FTC/TDF are characterized by continued downward pressure on branded products and a stable, low-cost environment for generics.

Price Trend Analysis:

- Branded FTC/TDF: Prices for originator products will likely continue to decline as generic penetration deepens. Pharmaceutical companies may focus on niche markets or specialized formulations to maintain some premium. Projected decline of 5-8% annually for the next two years, stabilizing thereafter.

- Generic FTC/TDF: Prices for generic FTC/TDF are expected to remain relatively stable at their current low levels. The market has largely matured, with pricing driven by manufacturing costs and competitive intensity. Significant price drops are unlikely, barring major shifts in manufacturing or raw material costs. Prices are projected to range from \$50 to \$150 per year per patient, depending on the region and supplier.

- Tenders and Bulk Purchasing: Prices in large-scale tenders may fall below \$50 per year per patient in highly competitive markets.

- Geographic Variations: Significant price disparities will persist between high-income countries with more robust reimbursement systems and low- to middle-income countries relying on donor funding and public health initiatives.

Factors Influencing Future Pricing:

- Competition Intensity: The number of generic manufacturers and their production capacities will remain a primary determinant of price.

- Manufacturing Costs: Fluctuations in the cost of raw materials, labor, and energy can have a marginal impact.

- Regulatory Policies: Changes in pricing regulations or reimbursement policies in key markets can influence pricing strategies.

- Emergence of New Therapies: The development and adoption of newer HIV treatment regimens could eventually impact the demand and pricing of older fixed-dose combinations like FTC/TDF, though this is expected to be a gradual process.

What are the future treatment guidelines and their impact on FTC/TDF demand?

Evolving HIV treatment guidelines and the introduction of novel antiretroviral therapies (ARTs) are key factors that will shape the future demand for FTC/TDF.

Guideline Evolution:

- Shift Towards Integrase Inhibitors: Major treatment guidelines, including those from the U.S. Department of Health and Human Services (DHHS) and the European AIDS Clinical Society (EACS), increasingly recommend integrase strand transfer inhibitors (INSTIs) as preferred first-line agents, often in combination with other drugs. INSTI-based regimens generally offer high efficacy, rapid viral suppression, and favorable tolerability profiles. [3]

- Long-Acting Injectables: The emergence of long-acting injectable ARTs, such as cabotegravir and rilpivirine (e.g., Cabenuva), represents a significant paradigm shift. These regimens offer the convenience of less frequent dosing (e.g., monthly or every two months) and are gaining traction for selected patient populations, potentially reducing reliance on daily oral pills.

- Single-Tablet Regimens (STRs) with Newer Agents: Newer STRs featuring INSTIs, nucleoside reverse transcriptase inhibitors (NRTIs), or non-nucleoside reverse transcriptase inhibitors (NNRTIs) with improved resistance profiles and tolerability are becoming the standard of care in many settings.

- Tenofovir Alafenamide (TAF) vs. TDF: Within the NRTI class, Tenofovir Alafenamide (TAF) has largely superseded Tenofovir Disoproxil Fumarate (TDF) in many newer combination regimens due to a more favorable kidney and bone safety profile. While FTC/TDF remains relevant, especially in resource-limited settings, the use of TAF-based combinations is growing in developed markets. [4]

Impact on FTC/TDF Demand:

- Declining First-Line Use in Developed Markets: In high-income countries, the recommendation of INSTI-based regimens and TAF-based combinations will likely lead to a gradual decline in the use of FTC/TDF as a first-line treatment.

- Sustained Relevance in Resource-Limited Settings: FTC/TDF is expected to remain a critical and widely used first-line ART in many low- and middle-income countries due to its established efficacy, low cost, and extensive procurement mechanisms through global health initiatives. Its affordability and proven track record make it a pragmatic choice where newer, more expensive agents are not yet accessible.

- Continued Use in Second-Line or Switch Strategies: FTC/TDF may continue to be used in second-line regimens or as part of switch strategies in patients who are stable on therapy and for whom cost is a primary consideration.

- PrEP Market: Demand for FTC/TDF in PrEP is likely to persist, though newer combinations with potentially better adherence profiles or reduced side effects could emerge as alternatives.

The overall demand for FTC/TDF will thus be bifurcated, with a projected decline in first-line use in developed nations but continued strong demand and relevance in resource-constrained regions and for specific patient populations.

What are the competitive advantages and disadvantages of FTC/TDF compared to newer HIV therapies?

FTC/TDF possesses distinct advantages and disadvantages when compared to the latest generation of HIV medications.

Competitive Advantages:

- Cost-Effectiveness: This is the most significant advantage. Generic FTC/TDF is among the most affordable ART options available globally, making it indispensable for public health programs and patients in low-resource settings. [5]

- Proven Efficacy and Long-Term Safety Data: Decades of clinical use have established FTC/TDF's robust efficacy in viral suppression and its long-term safety profile, albeit with known risks for renal and bone health with TDF.

- Established Procurement Channels: Extensive global supply chains and procurement mechanisms are in place for FTC/TDF, ensuring its consistent availability.

- Broad Resistance Barrier: While resistance can develop, FTC/TDF has a relatively high barrier to resistance when used as prescribed.

- Combination Therapy Simplicity: As a single tablet regimen (STR), it simplifies adherence compared to multiple pills.

Competitive Disadvantages:

- Toxicity Profile (TDF Component): Tenofovir disoproxil fumarate (TDF) is associated with a higher risk of renal toxicity and decreased bone mineral density compared to Tenofovir Alafenamide (TAF) and some newer NRTIs. This is a primary driver for the shift to TAF-based regimens in certain patient populations. [4]

- Dosing Frequency: FTC/TDF requires daily dosing, which can be a challenge for adherence compared to emerging long-acting injectable therapies.

- Drug Interactions: While generally well-tolerated, FTC/TDF can have drug interactions, though typically less complex than some newer agents.

- Emergence of Resistance: As with all ART, resistance to FTC/TDF can occur, especially with suboptimal adherence.

- Competition from Newer Regimens: INSTI-based regimens and long-acting injectables offer improved efficacy, tolerability, and convenience, which are becoming the preferred options for many patients and clinicians in developed markets.

The continued dominance of FTC/TDF will depend on its ability to maintain its cost-effectiveness advantage, particularly in regions where newer, more expensive therapies are not viable.

Key Takeaways

- The FTC/TDF market is projected to grow at a CAGR of 3.5% to reach approximately \$6.8 billion in 2022, with continued demand driven by the global HIV burden and its status as a first-line ART.

- Primary patent expiries have led to substantial generic competition, resulting in significant price erosion and increased accessibility, particularly in resource-limited settings.

- Generic FTC/TDF prices are expected to remain stable at low levels, ranging from \$50 to \$150 per year per patient, with branded product prices continuing to decline.

- Future demand for FTC/TDF will be bifurcated: declining in developed markets due to the preference for newer INSTI- and TAF-based regimens and long-acting injectables, but remaining critically important in low- and middle-income countries due to its cost-effectiveness.

- FTC/TDF's key advantage is its affordability and proven efficacy, while its primary disadvantage is the TDF component's associated renal and bone toxicity.

FAQs

-

When did the primary patents for emtricitabine and tenofovir disoproxil fumarate expire in major markets? Primary patents for the APIs emtricitabine and tenofovir disoproxil fumarate expired in the early 2020s in major markets such as the United States and Europe.

-

What is the projected annual cost of generic FTC/TDF for a patient in resource-limited settings? In resource-limited settings and through large tenders, generic FTC/TDF can cost between \$50 and \$150 per year per patient, with some competitive bids potentially falling below \$50 annually.

-

Which class of HIV drugs is increasingly replacing FTC/TDF as a first-line therapy in developed countries? Integrase strand transfer inhibitors (INSTIs) are increasingly recommended as preferred first-line agents in developed countries, often in combination with other drugs, leading to a decline in FTC/TDF's first-line use in these regions.

-

What is the main health concern associated with the TDF component of FTC/TDF? The main health concern associated with the tenofovir disoproxil fumarate (TDF) component is its potential for renal toxicity and decreased bone mineral density.

-

Will FTC/TDF continue to be used for HIV prevention (PrEP)? Yes, FTC/TDF is expected to remain a significant option for HIV pre-exposure prophylaxis (PrEP), although newer combinations may emerge as alternatives with potentially improved adherence or safety profiles.

Citations

[1] World Health Organization. (2022). Global HIV, Hepatitis and STIs Programmes: Global progress report. [2] U.S. Food & Drug Administration. (n.d.). Drugs@FDA. Retrieved from https://www.accessdata.fda.gov/scripts/cder/daf/ (Accessed specific patent expiry information through drug databases and regulatory filings.) [3] U.S. Department of Health and Human Services. (2023). Clinical Practice Guidelines for the Treatment of HIV Infection. [4] Sax, P. E., Wohl, D., Yin, M. T., Post, F., DeJesus, E., Saag, M., ... & Lathouwers, T. (2015). Tenofovir alafenamide versus tenofovir disoproxil fumarate, coformulated with elvitegravir, cobicistat, and emtricitabine, for initial treatment of HIV-1 infection: two randomized, double-blind, phase 3, non-inferiority trials. The Lancet, 385(9987), 2606-2615. [5] Global Fund to Fight AIDS, Tuberculosis and Malaria. (n.d.). HIV Treatment. Retrieved from https://www.theglobalfund.org/en/hiv/treatment/ (Accessed information on procurement and pricing strategies for essential medicines.)

More… ↓