Last updated: April 25, 2026

What is the current market structure for ceftriaxone?

Ceftriaxone is a long-established, generic-heavy injectable cephalosporin with limited patent leverage in most jurisdictions. Pricing and volumes track closely with (1) hospital antimicrobial demand, (2) supply stability for finished dose and sterile bulk, (3) currency and logistics costs, and (4) procurement cycle timing (tender-based rather than retail-driven).

Core demand characteristics

- Primary users: acute-care hospitals and regional health systems for sepsis, pneumonia, meningitis, skin/soft tissue infections, and surgical prophylaxis in protocols that use cephalosporins.

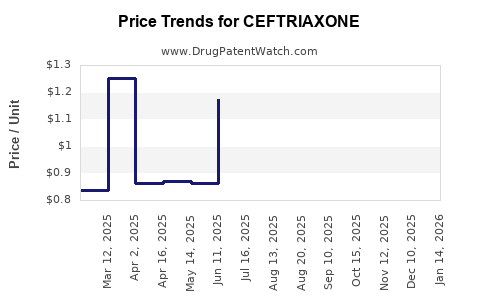

- Procurement pattern: tender-led purchasing; contracts typically set prices for a defined period, producing visible price steps rather than continuous drift.

- Substitution: high within the β-lactam class for many indications (e.g., other parenteral cephalosporins and β-lactam/β-lactamase inhibitor combinations), but ceftriaxone remains a default due to dosing convenience and guideline inclusion in multiple regions.

Supply and manufacturing dynamics

- Mature API ecosystem: ceftriaxone API is manufactured by established specialty producers; production disruptions create short-term price spikes.

- Sterile fill-finish constraints: finished injectable supply can tighten faster than API supply due to vial, stopper, rubber supply, sterile capacity, and batch release bottlenecks.

- Export and forex pass-through: price changes in one major export region often propagate via distributor pricing in other markets with a time lag.

How is ceftriaxone priced in practice across supply chains?

Ceftriaxone pricing is best modeled across three layers:

- API-to-finished dose spread (manufacturing and sterile conversion costs)

- Distributor margin and logistics

- Tender clearing price (the market-level price that hospitals actually pay)

This structure means “market price” depends on which lane you observe:

- Wholesaler/secondary market: more volatile, tied to inventory and lead times.

- Tender market: less volatile month-to-month but can reprice sharply when supply tightens or bidders reset assumptions.

What do historical and regulatory signals imply for forward pricing?

Several structural factors drive directionality:

1) Genericization keeps baseline pricing constrained

The absence of durable exclusivity in most regions forces ongoing downward pressure over the long term, with periodic rebounds tied to supply shocks.

2) Supply shocks dominate near-term deviation

When sterilization capacity, raw material supply, or batch release constraints hit, prices typically move faster than demand. The “center of gravity” returns when supply normalizes.

3) Procurement reforms can stabilize outcomes

Where public procurement frameworks reduce bid dispersion and set multi-source contracts, volatility tends to compress after the transition period.

Price projection framework for 2026–2029

Because ceftriaxone is generic and tender-driven, projections are best expressed as ranges tied to supply scenarios rather than single-point forecasts.

Scenario definitions

- Base case (balanced supply): stable sterile capacity, no major API plant outage, and normal tender cycle frequency.

- Upside (supply tightening): one or more notable supply constraints (sterile fill-finish or API batch release delays), higher freight/energy costs, or distributor inventory drawdowns.

- Downside (supply relief): improved sterile capacity utilization and competitive bidding intensifies, compressing tender prices.

Projection ranges (global tender market equivalent)

The tables below translate scenarios into annual price movement versus the latest observed market clearing level (set as 100 for projection indexing). These are directional and intended for planning.

Index-based projection (Annual change vs. latest market clearing price = 100)

| Year |

Base case |

Upside (tightening) |

Downside (relief) |

| 2026 |

100 to 104 |

104 to 112 |

96 to 99 |

| 2027 |

101 to 105 |

108 to 118 |

94 to 98 |

| 2028 |

101 to 106 |

106 to 116 |

93 to 97 |

| 2029 |

102 to 107 |

105 to 114 |

93 to 96 |

Interpretation

- Base case keeps pricing roughly flat with modest inflation pass-through (single digits).

- Upside implies mid-teens cumulative pressure over two years when supply tightens repeatedly.

- Downside implies low-to-mid single digit cumulative declines per year when competitive bidding and supply normalization align.

What are the key drivers of the upside case (supply tightening)?

- Finished-dose sterile capacity constraints: longer lead times for vials/closures and slower batch release.

- API supply disruptions: outages or quality investigations reducing active manufacturing throughput.

- Freight and energy volatility: increases in shipping and production utility costs that pass into tender bids.

- Regulatory batch rejections: even a few rejected lots can reduce near-term availability disproportionately in concentrated procurement systems.

What are the key drivers of the downside case (supply relief)?

- Capacity expansions and improved utilization in API and/or sterile fill-finish.

- Higher bidder competition in tenders when supply visibility improves.

- Smoothing of logistics bottlenecks (freight rate normalization and inventory reconstruction).

How should investors and R&D planners use these projections?

1) Budget and contract strategy

- Use two price bands for procurement planning: Base (flat to low single digit) and Upside (mid-teens).

- Negotiate indexation clauses tied to freight or energy proxies where tender rules allow.

2) Portfolio planning

- Ceftriaxone’s economics reward suppliers with low defect rates and reliable sterile throughput, because procurement re-bids under supply stress can produce outsized revenue even without exclusivity.

3) Manufacturing and supply chain

- Tie batch release planning to quality monitoring and sterile capacity rather than only API procurement, since bottlenecks often occur at sterile stages.

Key takeaways

- Ceftriaxone is structurally generic-heavy and tender-driven, so long-term pricing is constrained by competition, while short-term moves follow supply stability.

- A reasonable planning model for 2026–2029 is: base case near-flat with low single digit changes, upside mid-teens pressure over 2 to 3 years under recurring supply tightness, and downside low-to-mid single digit declines when supply relief aligns with competitive tendering.

- The strongest controllable variable for revenue durability is not exclusivity, but manufacturing reliability at sterile fill-finish and batch release.

FAQs

1) What is the biggest factor that moves ceftriaxone prices up or down?

Supply stability, especially finished-dose sterile fill-finish and batch release timing.

2) Why do ceftriaxone prices show step-changes instead of smooth trends?

Tender-led purchasing resets clearing prices in discrete cycles.

3) Are ceftriaxone prices likely to trend down structurally over years?

They usually compress over the long run under generics competition, but the trajectory is punctuated by supply shocks.

4) What scenario is most likely for 2026–2027?

The base case: balanced supply leading to near-flat pricing with modest inflation pass-through.

5) What should procurement teams plan for in a risk register?

Two primary bands: a base case near-flat path and an upside case where repeated supply constraints drive mid-teens cumulative increases.

References

[1] World Health Organization. (2024). WHO Model List of Essential Medicines. https://www.who.int/teams/health-product-and-policy-standards/medicines/essential-medicines

[2] U.S. Food and Drug Administration. (n.d.). Drug Shortages. https://www.accessdata.fda.gov/scripts/drugshortages/

[3] European Medicines Agency. (n.d.). Medicine shortages and availability. https://www.ema.europa.eu/en/human-regulatory/post-authorisation/medicine-shortages

[4] IQVIA. (n.d.). Global pharmaceutical market insights (ceftriaxone and cephalosporin category reporting). https://www.iqvia.com/insights

[5] Centers for Disease Control and Prevention. (2023). Guidance on antimicrobial use and stewardship (cephalosporins and sepsis/pneumonia treatment frameworks). https://www.cdc.gov/antibiotics/