Last updated: February 19, 2026

Famotidine, a histamine H2 receptor antagonist, is used to treat and prevent stomach ulcers and gastroesophageal reflux disease (GERD). The global famotidine market is projected to reach $800 million by 2030, growing at a compound annual growth rate (CAGR) of 3.5% from 2023 to 2030. Key market drivers include the increasing prevalence of GERD and peptic ulcers, aging global population, and a growing awareness of digestive health.

What is the current market size and growth trajectory for famotidine?

The global famotidine market was valued at approximately $640 million in 2022. Projections indicate a steady expansion, with an estimated market size of $800 million by 2030. This growth represents a CAGR of 3.5% over the forecast period from 2023 to 2030.

The market is segmented by drug formulation, application, and distribution channel.

Market Segmentation by Drug Formulation:

- Tablets: This segment holds the largest market share, accounting for approximately 60% of the total market in 2022. Their convenience and ease of administration drive this dominance.

- Oral Suspensions: This formulation is particularly favored for pediatric patients and individuals with dysphagia, contributing about 25% of the market share.

- Injectables: Used in hospital settings for severe cases, injectables represent the remaining 15% of the market.

Market Segmentation by Application:

- Gastroesophageal Reflux Disease (GERD): GERD is the primary application, representing 55% of the market share. The increasing incidence of lifestyle-related GERD fuels this segment.

- Peptic Ulcers (Gastric and Duodenal): This segment accounts for 30% of the market. Factors like H. pylori infection and NSAID use contribute to its demand.

- Zollinger-Ellison Syndrome: This rare condition accounts for the remaining 15% of the market.

Market Segmentation by Distribution Channel:

- Hospital Pharmacies: These are significant contributors, representing 40% of the market, driven by inpatient prescriptions.

- Retail Pharmacies: This channel accounts for 35% of the market, reflecting over-the-counter (OTC) sales and prescriptions filled in community settings.

- Online Pharmacies: This segment is experiencing rapid growth, currently holding 25% of the market, attributed to the convenience of home delivery and accessibility.

What are the key factors driving demand for famotidine?

Several factors are contributing to the sustained demand for famotidine:

- Increasing Prevalence of GERD and Peptic Ulcers: Lifestyle changes, including dietary habits and stress, have led to a rise in acid-related gastrointestinal disorders. The World Gastroenterology Organisation reports that GERD affects 10-20% of the population in Western countries (1). This widespread condition directly translates to a consistent need for effective treatments like famotidine.

- Aging Global Population: The demographic shift towards an older population is a significant driver. Elderly individuals are more susceptible to gastrointestinal issues, including those requiring H2 antagonists. The United Nations projects that by 2050, one in six people worldwide will be over 65 years old (2).

- Growing Awareness of Digestive Health: Increased public awareness campaigns and readily available information on digestive health encourage individuals to seek medical advice and treatment for symptoms, boosting demand for OTC and prescription medications.

- Favorable Reimbursement Policies: In many regions, famotidine is a well-established and cost-effective treatment option, often covered by insurance and national health schemes, making it accessible to a broad patient base.

- Off-Patent Status and Generic Availability: Famotidine has been off-patent for many years, leading to a highly competitive generic market. This availability of affordable generic versions ensures broad accessibility and continued market penetration.

What is the competitive landscape for famotidine?

The famotidine market is characterized by a fragmented competitive landscape dominated by generic manufacturers. Key players include:

- Teva Pharmaceutical Industries Ltd.: A leading global generic drug manufacturer.

- Dr. Reddy's Laboratories Ltd.: An Indian multinational pharmaceutical company.

- Sun Pharmaceutical Industries Ltd.: Another major Indian pharmaceutical company with a strong global presence.

- Aurobindo Pharma Ltd.: A vertically integrated pharmaceutical company.

- Mylan N.V. (now part of Viatris Inc.): A significant player in the generics market.

- Perrigo Company plc: Known for its OTC and generic prescription drugs.

These companies compete on price, product availability, and distribution networks. The absence of patent exclusivity means that innovation in this space focuses on manufacturing efficiency and market penetration rather than novel drug development.

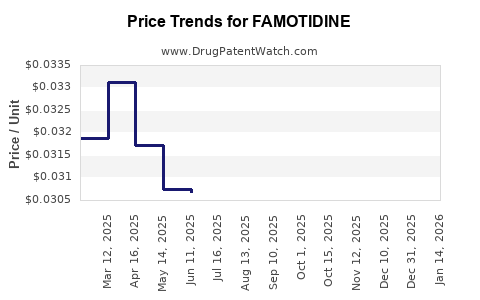

What are the price trends and projections for famotidine?

The pricing of famotidine is predominantly influenced by the generic nature of the drug.

- Current Pricing: The average retail price for a 30-count bottle of 20mg famotidine tablets typically ranges from $10 to $20. Pricing can vary based on the manufacturer, dosage strength, and quantity purchased. Bulk purchases by hospitals and pharmacies may result in lower per-unit costs.

- Price Projections: Given the established generic market and mature product lifecycle, significant price fluctuations are not anticipated. The market is expected to remain competitive, with prices likely to see a slight decrease or remain stable in the coming years, driven by ongoing competition among generic manufacturers. A minor increase of 1-2% annually might occur due to inflation or minor supply chain adjustments, but substantial price hikes are improbable. The average wholesale price (AWP) for famotidine is expected to stay within a range of $0.20-$0.50 per tablet for standard dosages.

Factors influencing price:

- Manufacturing Costs: Raw material costs, production scale, and regulatory compliance directly impact pricing.

- Competition: The number of generic manufacturers and their market share significantly influence price levels. A higher number of competitors generally leads to lower prices.

- Regulatory Environment: Pricing regulations and reimbursement policies in different countries can affect the final retail price.

- Supply Chain Dynamics: Disruptions in the supply chain, such as raw material shortages or transportation issues, can temporarily impact pricing, though this is less common for established generics.

What are the regulatory considerations and market access challenges for famotidine?

Famotidine is a well-established drug with long-standing regulatory approvals in major markets.

- Approvals: It has been approved by regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) for decades.

- Market Access: For generic manufacturers, market access primarily involves securing manufacturing licenses, adhering to Good Manufacturing Practices (GMP), and obtaining national drug registrations. The primary challenge for market access lies in demonstrating cost-effectiveness and securing favorable formulary placement within healthcare systems.

- Quality Standards: Manufacturers must consistently meet stringent quality control standards to maintain market access. Any deviation from GMP or product quality issues can lead to recalls or market withdrawal.

- Therapeutic Equivalence: Generic versions must demonstrate bioequivalence to the reference listed drug, a standard requirement for regulatory approval.

What are the potential risks and opportunities in the famotidine market?

Opportunities:

- Emerging Markets: Expansion into underdeveloped and developing countries where access to essential medicines is increasing presents an opportunity for generic manufacturers.

- Combination Therapies: Potential for exploring famotidine in combination with other agents for specific gastrointestinal conditions, although this is a less likely avenue for significant growth given its established role.

- Improved Formulations: Development of novel drug delivery systems or more convenient formulations (e.g., rapid-dissolve tablets) could offer a niche advantage.

Risks:

- Competition from Newer Drug Classes: While famotidine remains a mainstay, the development of newer classes of drugs for acid suppression, such as proton pump inhibitors (PPIs), and the ongoing research into novel therapies for GERD and related disorders, pose a long-term competitive threat. However, famotidine's lower cost and established safety profile continue to ensure its market presence.

- Regulatory Scrutiny: Increased regulatory oversight regarding drug manufacturing and quality can lead to compliance costs or market access disruptions if not managed effectively.

- Supply Chain Volatility: Global events can impact the availability and cost of active pharmaceutical ingredients (APIs) and excipients, potentially affecting production and pricing.

Key Takeaways

The famotidine market is stable and projected for modest growth, driven by the persistent prevalence of acid-related gastrointestinal diseases and demographic trends. The market is mature and highly competitive, characterized by generic manufacturers prioritizing cost-efficiency and broad distribution. Significant price increases are unlikely due to the drug's off-patent status and the presence of numerous generic alternatives. Opportunities lie in emerging markets and potentially in niche formulation improvements, while risks include competition from newer drug classes and potential supply chain disruptions.

FAQs

What are the main differences between famotidine and proton pump inhibitors (PPIs)?

Famotidine is a histamine H2 receptor antagonist that reduces stomach acid production. Proton pump inhibitors (PPIs) are a different class of drugs that block the final step of acid production more potently. PPIs generally offer more complete acid suppression and are often preferred for severe GERD or ulcer healing, though famotidine remains a cost-effective option for milder symptoms and maintenance therapy (3).

Is famotidine available over-the-counter (OTC)?

Yes, famotidine is widely available over-the-counter (OTC) in many countries, typically in lower dosages (e.g., 10mg and 20mg). Higher strengths and prescription formulations are available through a doctor's prescription.

What is the typical duration of famotidine treatment?

The duration of famotidine treatment varies depending on the condition being treated. For heartburn or indigestion, it may be used as needed or for short-term relief. For conditions like GERD or peptic ulcers, a doctor may prescribe it for several weeks or months. Long-term use should be monitored by a healthcare professional.

Are there any significant side effects associated with famotidine?

Famotidine is generally well-tolerated. Common side effects are usually mild and can include headache, dizziness, diarrhea, or constipation. Serious side effects are rare but can include confusion, hallucinations, or arrhythmias. Patients should consult their doctor or pharmacist for a complete list of potential side effects.

How does the pricing of generic famotidine compare to branded versions?

As famotidine is off-patent, branded versions are uncommon, and the market is dominated by generic manufacturers. Generic famotidine is significantly more affordable than any historical branded versions were, offering a cost-effective treatment option. Prices are highly competitive among generic producers, leading to low and stable per-unit costs.

What are the active pharmaceutical ingredients (APIs) and excipients commonly used in famotidine formulations?

The active pharmaceutical ingredient is famotidine. Excipients used in tablet formulations can include microcrystalline cellulose, starch, magnesium stearate, and coatings such as hypromellose. For oral suspensions, common excipients include sweeteners, thickeners, and flavoring agents. The exact composition varies by manufacturer.

What is the typical shelf life for famotidine tablets?

Famotidine tablets typically have a shelf life of 2 to 3 years from the date of manufacture, provided they are stored at room temperature away from moisture and light. The expiration date is printed on the packaging.

Citations

[1] World Gastroenterology Organisation. (2018). Global Guidelines: Gastro-oesophageal reflux disease. Retrieved from https://www.worldgastroenterology.org/guidelines/global-guidelines/gerd

[2] United Nations, Department of Economic and Social Affairs, Population Division. (2022). World Population Prospects 2022. Retrieved from https://population.un.org/wpp/

[3] National Institute of Diabetes and Digestive and Kidney Diseases. (2020). Acid Reflux (GER & GERD). National Institutes of Health. Retrieved from https://www.niddk.nih.gov/health-information/digestive-diseases/acid-reflux-ger-gerd