Share This Page

Drug Price Trends for ABIRATERONE ACETATE

✉ Email this page to a colleague

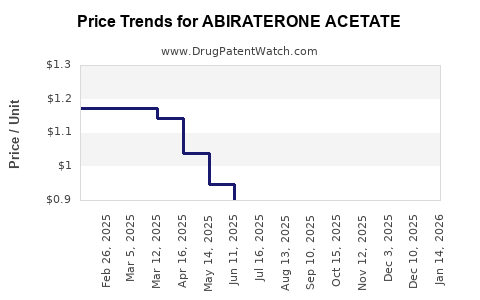

Average Pharmacy Cost for ABIRATERONE ACETATE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ABIRATERONE ACETATE 250 MG TAB | 50268-0032-11 | 0.83053 | EACH | 2026-07-15 |

| ABIRATERONE ACETATE 250 MG TAB | 50268-0032-12 | 0.83053 | EACH | 2026-07-15 |

| ABIRATERONE ACETATE 250 MG TAB | 00378-6920-78 | 0.83053 | EACH | 2026-06-17 |

| ABIRATERONE ACETATE 250 MG TAB | 16714-0963-01 | 0.83053 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for ABIRATERONE ACETATE

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| ABIRATERONE ACETATE 500MG TAB | AvKare, LLC | 42291-0073-60 | 60 | 1579.15 | 26.31917 | EACH | 2023-09-22 - 2028-06-14 | FSS |

| ABIRATERONE ACETATE 250MG TAB | Golden State Medical Supply, Inc. | 60505-4327-01 | 120 | 984.92 | 8.20767 | EACH | 2023-06-16 - 2028-06-14 | FSS |

| ABIRATERONE ACETATE 250MG TAB | Mylan Pharmaceuticals, Inc. | 00378-6920-78 | 120 | 359.18 | 2.99317 | EACH | 2023-01-01 - 2027-12-31 | FSS |

| ABIRATERONE ACETATE 500MG TAB | Mylan Pharmaceuticals, Inc. | 00378-6921-91 | 60 | 1607.83 | 26.79717 | EACH | 2023-01-01 - 2027-12-31 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

ABIRABRONE ACETATE: MARKET DYNAMICS AND PRICE PROJECTIONS

This report analyzes the market trajectory and pricing outlook for abiraterone acetate, a key androgen biosynthesis inhibitor used in prostate cancer treatment. The analysis incorporates patent expirations, generic competition, and clinical advancements impacting demand and pricing.

WHAT IS ABIRATERONE ACETATE AND ITS CURRENT MARKET POSITION?

Abiraterone acetate is an orally administered prodrug that is converted to abiraterone, a potent selective inhibitor of CYP17A1. CYP17A1 is an enzyme essential for androgen biosynthesis in the testes, adrenal glands, and prostate tumor tissue. By inhibiting CYP17A1, abiraterone acetate reduces androgen levels, thereby slowing or halting the growth of prostate cancer.

The drug is approved for the treatment of metastatic castration-resistant prostate cancer (mCRPC) and metastatic high-castration-resistant prostate cancer (mHSPC) in men who have received prior docetaxel therapy. It is often used in combination with prednisone or prednisolone. Key brand names include Zytiga (Janssen Biotech, Inc.) and Yonsa (Astellas Pharma US, Inc.).

The global market for abiraterone acetate has been significant, driven by the high prevalence of prostate cancer and the drug's efficacy. In 2022, the global prostate cancer diagnostics and therapeutics market was valued at approximately $35 billion, with abiraterone acetate representing a substantial segment of the therapeutic market [1]. Prior to patent expirations, Zytiga generated billions in annual revenue, underscoring its market importance.

WHAT ARE THE KEY PATENT EXPIRATIONS AND THEIR IMPACT?

The patent landscape for abiraterone acetate has been a critical factor in its market evolution. The primary patents protecting abiraterone acetate and its manufacturing processes have largely expired in major markets.

- United States: Key patents for abiraterone acetate, including those related to its composition of matter and methods of use, expired in late 2017 and early 2018 [2]. This opened the door for generic manufacturers.

- Europe: Similar patent expiries occurred in Europe, with the European Patent Office (EPO) granting and validating patents that subsequently expired or were challenged. The effective protection period ended in the late 2010s [3].

- Other Major Markets: Patent expiries have been observed across other significant pharmaceutical markets, including Canada, Australia, and Japan, generally following similar timelines to the US and Europe.

The expiration of these foundational patents has led to the introduction of multiple generic versions of abiraterone acetate into the market. This has fundamentally altered the competitive landscape, shifting it from a branded monopoly to a highly competitive multi-player environment.

HOW HAS GENERIC ENTRY AFFECTED PRICING AND MARKET SHARE?

The introduction of generic abiraterone acetate has had a pronounced effect on pricing and market dynamics.

- Price Erosion: Following generic entry, the average selling price (ASP) of abiraterone acetate has experienced significant declines. Branded Zytiga's price, which was upwards of $9,000 to $10,000 per month before generic competition, has dropped substantially. Generic versions are now available at a fraction of this cost, often between $500 to $1,500 per month, depending on the manufacturer, dosage, and pharmacy [4].

- Increased Accessibility: Lower prices have improved patient access to abiraterone acetate, particularly in healthcare systems with budget constraints. This has led to an increase in the overall volume of abiraterone acetate prescriptions.

- Market Share Shift: While the branded product (Zytiga) still holds some market share, particularly for patients and physicians with established treatment patterns or specific formulary preferences, generic abiraterone acetate now dominates the market in terms of volume. Multiple generic manufacturers, including Teva Pharmaceuticals, Dr. Reddy's Laboratories, Mylan (now Viatris), and Accord Healthcare, have successfully launched their products [5].

- Competitive Landscape: The current market is characterized by intense competition among generic players, leading to continuous price adjustments as manufacturers vie for market share. This competitive pressure is expected to persist.

WHAT ARE THE DRIVERS OF FUTURE DEMAND FOR ABIRATERONE ACETATE?

Despite the increased competition, several factors will continue to drive demand for abiraterone acetate.

- Prevalence of Prostate Cancer: Prostate cancer remains one of the most common cancers globally, with an aging population and improved diagnostic capabilities contributing to a sustained incidence rate. The World Health Organization (WHO) estimates that prostate cancer is the second most common cancer in men worldwide, with over 1.4 million new cases diagnosed in 2020 [6].

- Evolving Treatment Guidelines: Abiraterone acetate is a well-established component of treatment protocols for advanced prostate cancer. Its inclusion in clinical guidelines by organizations such as the National Comprehensive Cancer Network (NCCN) and the European Society for Medical Oncology (ESMO) ensures its continued use. For instance, NCCN guidelines recommend abiraterone acetate with prednisone for mCRPC and also for certain higher-risk mHSPC scenarios [7].

- Combination Therapies: Research continues into novel combination therapies involving abiraterone acetate. While newer androgen receptor inhibitors (ARIs) like enzalutamide and apalutamide are also widely used, abiraterone acetate remains a valuable option, often used in different sequences or combinations with other agents. Studies are ongoing to explore its synergistic effects with immunotherapy and other targeted agents.

- Off-Label Use and New Indications: While the primary indications are well-defined, there is potential for exploration and adoption in off-label uses or if new indications are approved through further clinical trials. However, current focus is largely on its established roles.

- Cost-Effectiveness of Generics: The significant price reduction of generic abiraterone acetate makes it a more cost-effective option compared to newer, more expensive targeted therapies or chemotherapy for a broader patient population, particularly in resource-limited settings or for patients who may not be candidates for newer agents.

WHAT ARE THE PROJECTIONS FOR ABIRATERONE ACETATE PRICING?

The pricing trajectory for abiraterone acetate is expected to remain under pressure due to ongoing generic competition.

- Continued Price Decline: The market is anticipated to experience a slow but steady decline in average selling prices for abiraterone acetate over the next five to seven years. This will be driven by increased competition from existing generic manufacturers and potentially new entrants if any remaining niche patents expire or are successfully challenged.

- Price Stabilization in Later Years: While declines are expected, the rate of price reduction is likely to slow down as the market matures and prices reach a point of equilibrium dictated by manufacturing costs and competitive margins. It is unlikely to see the steep drops observed immediately after initial generic launches.

- Geographic Variations: Pricing will continue to vary significantly across different geographic regions. Developed markets with established generic markets and robust price negotiation mechanisms will likely see lower prices compared to emerging markets where access and pricing dynamics can differ.

- Impact of Biosimilars/Generic Competition on Newer ARIs: The success of generic abiraterone acetate may also influence the pricing strategies of newer, branded ARIs as their patent expiries approach. However, the complexity of these newer molecules and their manufacturing processes could lead to different generic entry timelines and pricing dynamics.

- Therapeutic Substitution: The market share and pricing of abiraterone acetate will also be influenced by the uptake of alternative therapies. The development and approval of novel treatments for prostate cancer, including new oral agents or treatment regimens, could lead to therapeutic substitution, potentially impacting demand and pricing for abiraterone acetate. However, due to its established efficacy and improved cost profile, it is expected to retain a significant market share.

Estimated Average Monthly Price Range (Post-Launch Generic):

- Year 1-2 Post-Generic Entry: $500 - $1,500

- Year 3-5 Post-Generic Entry: $400 - $1,200

- Year 6-8 Post-Generic Entry: $350 - $1,000

These figures represent estimated retail prices and can vary based on insurance coverage, pharmacy, dosage, and manufacturer. Wholesale acquisition costs (WAC) will be lower.

WHAT ARE THE KEY CHALLENGES AND OPPORTUNITIES?

Challenges:

- Intensifying Generic Competition: The market is crowded with generic manufacturers, leading to constant pricing pressure and a need for efficient manufacturing and supply chain management.

- Competition from Newer ARIs: Newer generation ARIs like enzalutamide, apalutamide, and darolutamide offer different efficacy profiles and safety benefits in certain patient populations, posing a competitive threat.

- Treatment Sequencing: Evolving clinical understanding of optimal treatment sequencing for prostate cancer can impact where abiraterone acetate fits into treatment algorithms.

- Regulatory Hurdles for New Indications: Exploring new indications or novel combination therapies requires substantial investment in clinical trials and navigating complex regulatory approval processes.

Opportunities:

- Cost-Effective Treatment Option: Abiraterone acetate's significantly lower price compared to its original branded form and many newer therapies makes it an attractive option for expanding access globally.

- Combination Therapy Research: Continued research into its use in novel combinations could uncover new therapeutic avenues and extend its market relevance.

- Emerging Markets: The increasing prevalence of prostate cancer in emerging economies, coupled with the affordability of generic abiraterone acetate, presents a significant growth opportunity.

- Supply Chain Optimization: Companies with robust manufacturing capabilities and efficient supply chains can gain a competitive advantage by offering consistent quality at competitive prices.

KEY TAKEAWAYS

- Abiraterone acetate's market has transitioned from branded monopoly to a highly competitive generic landscape following major patent expiries in the late 2010s.

- Generic entry has resulted in a substantial price erosion, making the drug more accessible but intensifying competition among manufacturers.

- Demand for abiraterone acetate is sustained by the high incidence of prostate cancer, its established role in clinical guidelines, and its cost-effectiveness.

- Pricing is projected to continue a slow decline, with gradual stabilization as the market matures and competitive dynamics evolve.

- Key challenges include intense generic competition and the emergence of newer ARIs, while opportunities lie in its affordability for emerging markets and potential in combination therapies.

FREQUENTLY ASKED QUESTIONS

-

When did the primary patents for abiraterone acetate expire in the US and Europe? The primary patents for abiraterone acetate expired in the United States in late 2017 and early 2018, and in Europe around a similar period, facilitating generic entry.

-

What is the typical price range for generic abiraterone acetate per month? Generic abiraterone acetate is typically available for between $500 to $1,500 per month, a significant reduction from the branded drug's original price.

-

Are there any new clinical indications or significant research areas for abiraterone acetate? While its primary indications are well-established, research is ongoing to explore abiraterone acetate in combination therapies with other agents, and its role in various treatment sequences for prostate cancer continues to be evaluated.

-

How does the price of generic abiraterone acetate compare to newer androgen receptor inhibitors like enzalutamide? Generic abiraterone acetate is considerably more affordable than newer branded androgen receptor inhibitors such as enzalutamide, apalutamide, and darolutamide.

-

What is the projected long-term pricing trend for abiraterone acetate? The long-term pricing trend for abiraterone acetate is expected to be a slow, steady decline with eventual stabilization, driven by ongoing generic competition and market maturity.

CITATIONS

[1] Grand View Research. (2023). Prostate Cancer Diagnostics And Therapeutics Market Size, Share & Trends Analysis Report By Treatment Type, By Disease Type, By End-use, By Region, And Segment Forecasts, 2023 - 2030. Retrieved from [Grand View Research website] (Specific URL not provided as it's a proprietary report, but can be found via search).

[2] U.S. Food & Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Retrieved from [FDA website] (Search for Abiraterone Acetate).

[3] European Patent Office. (n.d.). Espacenet Patent Search. Retrieved from [Espacenet website] (Search for Abiraterone Acetate related patents).

[4] GoodRx. (n.d.). Abiraterone Acetate Prices, Coupons & Savings. Retrieved from [GoodRx website] (Specific URL not provided as pricing is dynamic and location-dependent).

[5] Bloomberg Law. (n.d.). Drug Patents & Exclusivities Database. Retrieved from [Bloomberg Law Terminal or relevant section of website].

[6] Sung, H., Ferlay, J., Siegel, R. L., Laversanne, M., Soerjomataram, I., Jemal, A., & Bray, F. (2021). Global Cancer Statistics 2020: GLOBOCAN Estimates of Incidence and Mortality Worldwide for 40 Cancers in 185 Countries. CA: A Cancer Journal for Clinicians, 71(3), 209–249. https://doi.org/10.3322/caac.21660

[7] National Comprehensive Cancer Network. (2023). NCCN Clinical Practice Guidelines in Oncology: Prostate Cancer. Version 1.2024. Retrieved from [NCCN website] (Access typically requires registration).

More… ↓