Last updated: June 3, 2026

Transaxamic acid market performance is driven by (1) procedure volumes in surgery and obstetrics, (2) guideline adoption for bleeding control, (3) hospital formulary behavior and tender pricing, (4) generic penetration in multiple countries, and (5) re-bundling risk from originator-to-generic substitution and local tender dynamics. Across major markets, Tranexamic acid’s commercial trajectory is shaped less by brand differentiation and more by generic supply stability, price erosion after exclusivity/marketing authorizations expire, and uptake of specific evidence-based indications (notably perioperative bleeding and postpartum hemorrhage).

What is tranexamic acid used for, and how do indications drive market demand?

Tranexamic acid is an antifibrinolytic used to reduce bleeding by inhibiting plasminogen activation. Demand is segmented by setting and dosing form:

Which clinical settings account for the largest share of tranexamic acid sales?

- Hospital perioperative use (orthopedics, general surgery, cardiac surgery, trauma)

- Obstetrics (postpartum hemorrhage prophylaxis and treatment where adopted in clinical pathways)

- Trauma and emergency bleeding (protocolized use in emergency departments)

- Dental/ENT procedures (localized bleeding control in some markets via topical regimens)

- Ophthalmology (e.g., cataract-related bleeding protocols in some countries, depending on local approvals)

How do guideline and protocol changes affect adoption speed?

Adoption follows institutional bleeding protocols. Market impact typically comes in waves:

- New or updated protocols after clinical evidence cycles (hospital committee review periods)

- Tender cycles aligned with public procurement calendars

- Switch-to-generic decisions after originator pricing becomes noncompetitive

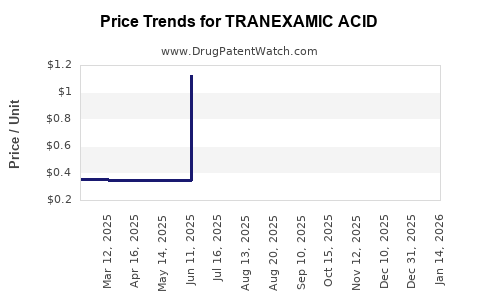

How fast has the tranexamic acid market been commoditizing under generic competition?

Tranexamic acid is widely available as generics and older branded products in many jurisdictions. This compresses margins and shifts revenue capture to:

- Supply reliability

- Low-cost manufacturing

- Contracting leverage in hospital procurement

What does commoditization look like in pricing and margin structure?

- Net price decline typically outpaces volume growth once generics become entrenched

- Distributor and tender price discovery drives end-market pricing

- Formulation differentiation (IV vs oral vs topical) matters less than availability and procurement economics

How does tender procurement change the competitive landscape?

- Local suppliers win via bid pricing and service-level commitments (supply continuity, delivery time, batch availability)

- Multi-supplier procurement can occur if formularies keep at least two sources

- Contract awards shift market share quickly when pricing and supply terms improve

What are the main formulation and route categories, and how do they perform financially?

Tranexamic acid commercial performance is mainly determined by route and setting:

IV tranexamic acid (hospital acute and perioperative use)

- Highest intensity of use in controlled protocols

- Revenue tends to be large in volume but margin-compressed due to generic availability

- Supply interruption risk is commercially material because hospitals prefer uninterrupted stock for elective and emergency workflows

Oral tranexamic acid (adjunct and off-protocol uses in some indications)

- Lower acute urgency reduces IV-like purchasing cycles

- Revenue can be steadier where chronic or procedure-adjacent regimens exist

- Generic substitution is common; differentiation is limited unless a specific branded regimen is tied to reimbursement or guideline pathways

Topical tranexamic acid (localized bleeding control)

- Uptake depends on procedure-specific evidence and payer acceptance

- Revenue growth can occur at the expense of systemic dosing when local protocols change

- Competitive pressure is high where topical products are easier to manufacture and distribute

When does tranexamic acid lose exclusivity in key markets, and what does that mean for revenue?

Tranexamic acid is not a single “originator-only” product across all markets; multiple early approvals and generic entries exist globally. The financial impact in most countries has already transitioned into a largely generic market structure in practical terms.

What drives the “post-exclusivity” revenue curve?

- Originator revenue declines are usually steep once generics become the default tender choice

- Recovery is possible only if volumes expand materially (protocol expansion, new indications) or if new regulated formulations gain adoption

- In mature markets, growth often comes from procedure volumes rather than price

What is the practical effect on financial trajectory by geography?

- Developed markets: fast price compression, then stabilization; share shifts between generics via tender pricing

- Emerging markets: volume growth can be higher, but price erosion and import or supply constraints can create volatility

- Public procurement-heavy systems: tender cycles create step-function market share changes

What patents protect tranexamic acid, and how does IP affect commercialization and pricing?

Tranexamic acid is an established active ingredient. IP and exclusivity effects tend to be:

- limited for the base molecule (old chemistry)

- more relevant for specific formulations, delivery devices, therapeutic regimens, or combination products depending on jurisdiction and product-specific approvals

How does formulation-level IP alter the competitive set?

- If a product is protected by formulation or method-of-use claims, it can remain preferred on formularies longer

- Once those barriers expire, tenders typically move rapidly to lowest-cost compliant supply

What is the FDA and Orange Book status of tranexamic acid products?

Tranexamic acid has multiple approved products across dosage forms and manufacturers. In the US, the Orange Book listing governs patent and exclusivity associations for specific NDA/ANDA products rather than for the active ingredient broadly.

How does Orange Book coverage influence generic entry risk in the US?

- If a specific branded product lists formulation/combination or method-of-use patents, ANDA filers may face Paragraph IV challenges

- For many mature tranexamic acid products, practical risk is lower because the market is already generic-dominated

What Paragraph IV and patent litigation risks matter for tranexamic acid generics?

For tranexamic acid, litigation and Paragraph IV dynamics are most relevant at the product level, not the core active ingredient. Commercial risk tends to be:

- delays in specific ANDA launches where Orange Book patents are enforced

- settlement agreements that can defer generic availability temporarily

Which launch blockers are commercially important?

- Listed patents tied to IV solution/formulation, packaging, or specific therapeutic labeling

- Method-of-use or regimen claims tied to indications that align with reimbursement

How do originators and major generics compete in tranexamic acid tenders?

In many markets, competitive advantage is procedural rather than scientific:

- guaranteed supply

- compliance and inspection track record

- contracting terms with wholesalers and group purchasing organizations

What commercial levers determine winner-take-most share?

- Tender pricing and rebate structures

- Forecast accuracy and production flexibility

- Shelf-life and packaging formats matching hospital procurement preferences

- Delivery reliability for elective and emergency stock needs

How does tranexamic acid financial performance compare with other hemostatics?

Tranexamic acid competes within the broader hemostasis and bleeding control ecosystem, including agents and technologies such as:

- other antifibrinolytics

- topical hemostats and sealants

- systemic and local coagulation pathway modulators (market structure varies by country)

Where does tranexamic acid typically win?

- Standardization in perioperative and obstetric bleeding protocols

- Cost-effective profile versus many device- or biologic-adjacent approaches

- Ease of procurement for hospitals already stocked with IV products

Where does it face substitution pressure?

- Where topical hemostats are preferred by surgeons or where evidence supports local regimens

- Where different anticoagulant reversal strategies dominate in specific bleeding contexts

What commercial growth drivers can still expand tranexamic acid revenue despite price erosion?

Despite generic pricing pressure, revenue can grow through:

- increased procedure volumes (surgery and trauma incidence trends)

- broader adherence to evidence-based bleeding protocols

- expansion in obstetric care pathways

- adoption of topical or route-specific regimens where they reduce systemic exposure

What is the most realistic revenue trajectory shape?

- Mature base: modest volume growth with continuing price pressure

- Select expansions: short-lived premium for newly adopted route/formulation

- Most markets: revenue becomes highly sensitive to tender pricing and supply continuity rather than brand marketing

Key market dynamics that affect earnings: supply chain, shortages, and manufacturing scale

Tranexamic acid manufacturing is scaleable, but supply stability can still swing procurement behavior.

How do supply constraints impact pricing and revenue?

- In shortage periods, prices can spike and hospitals increase spend to maintain stock

- Post-shortage normalization returns prices toward tender floors

- Companies with proven production continuity often retain share through procurement trust

What manufacturing and compliance factors matter commercially?

- Batch release reliability and regulatory inspection outcomes

- Ability to meet procurement schedule and emergency demand

- Packaging formats meeting hospital safety and inventory rules

Key Takeaways

- Tranexamic acid market growth is predominantly volume-driven and protocol-driven, not brand-driven.

- Generic competition compresses prices; revenue stability depends on tender wins and supply reliability.

- Route and formulation adoption (IV perioperative, obstetric protocols, and topical regimens where accepted) can create pockets of incremental growth.

- IP effects are mostly product-specific (formulation, regimen, packaging) rather than active-ingredient exclusivity, so generic entry risk is tied to Orange Book coverage at the product level.

- Financial trajectory in mature markets typically follows: post-generic penetration price decline, then stabilization with share shifts driven by procurement economics.

FAQs

- How do hospital tender cycles impact tranexamic acid net pricing in the US and EU?

- Which tranexamic acid dosage forms are most exposed to generic substitution in each major market?

- What are the main clinical indications driving tranexamic acid volume growth in obstetrics and surgery?

- How do supply shortages or batch-release delays change tranexamic acid procurement behavior?

- What formulation-level IP or Orange Book listings most commonly delay generic entry for hemostatics like tranexamic acid?

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- World Health Organization. Clinical guidance and recommendations on tranexamic acid for bleeding indications. World Health Organization.