Last updated: May 20, 2026

Mupirocin Market Dynamics and Financial Trajectory: Sales Trends, Competitive Threats, and Outlook

Mupirocin is a topical antibiotic used for localized skin infections, most prominently impetigo and infected eczema, and for nasal decolonization in MRSA prevention protocols. The market is structurally mature, dominated by off-patent generic formulations, with value concentrated in guideline-driven indications, retail prescribing patterns, and institutional formulary access. Financial trajectory is shaped more by volume stability, substitution at the pharmacy counter, and hospital procurement than by payer step edits or late-stage innovation.

Why does mupirocin’s sales performance remain stable even as generics dominate?

The sales base for mupirocin largely behaves like other established topical anti-infectives: steady demand for common skin infections and recurring infection-control workflows. Since many mupirocin products are off patent and compete primarily on price and contracting, growth is limited, but declines are moderated by persistent clinical use.

Core drivers

- Indication durability: Impetigo and infected dermatitis remain frequent outpatient dermatology/infectious disease problems.

- Institutional protocols: Nasal decolonization is used in many MRSA prevention programs, creating recurring demand outside peak retail seasonality.

- Low prescriber switching costs: Therapeutic class competition is limited for first-line topical antibiotic use; substitution usually stays within mupirocin.

- Formulation-specific preference: Ointment vs cream selection, tube size, and application convenience affect retention with formularies.

Core constraints

- Generic interchangeability: Price competition compresses margins and slows revenue growth.

- Stewardship sensitivity: Infection prevention programs can reduce unnecessary use to limit resistance pressures.

- Activity spectrum considerations: Mupirocin resistance concerns can shift volume within institutional decolonization programs, impacting procurement.

Ointment vs cream: what matters for commercial outcomes?

Mupirocin’s market is typically segmented by dosage form and strength (commonly 2%). Market dynamics often tilt toward whichever form is more compatible with local prescribing habits, patient tolerability, and stocking patterns.

Where do sales usually concentrate: retail or hospital?

- Retail: outpatient impetigo/infected lesions; substitution favors lowest net price under rebate and contract structures.

- Hospital/institution: decolonization protocols; distribution depends on GPO and ID committee decisions.

What is the patent and exclusivity position of mupirocin products affecting revenue?

For business planning, mupirocin’s key point is not a single “drug patent,” but the overall effect of mature exclusivity: most marketed topical mupirocin products have long since transitioned to generic competition. That results in a revenue profile that behaves like a commoditized branded-to-generic life cycle.

What typically shapes the IP landscape

- Formulation and packaging: Many later-expiring patents, if any, tend to cover specific formulations, delivery vehicles, or manufacturing processes rather than new molecular entity exclusivity.

- Method-of-use: Some coverage can exist around decolonization protocols, but enforcement is usually narrow and less likely to block generics broadly.

Commercial implication

- Licensing or settlement activity is generally less central for mupirocin than for novel therapeutics; the market’s dominant determinant is pricing and procurement rather than exclusivity-driven supply protection.

How many products and competitors usually compete in mupirocin?

Market structure is typically highly fragmented with multiple ANDA generics and pharmacy store brands depending on region and supply. Competitive density reduces brand pricing power and drives margin compression.

When does mupirocin face generic entry risk that could disrupt market share?

Generic entry risk remains low at the class level because the product is broadly established and usually already generic. The risk window is more about incremental supply (new manufacturers, new package sizes) and contracting events (GPO rebids, wholesaler switches) than about sudden “first generic” displacement.

Where entry can still cause commercial disruption

- Contract re-tendering: institutional buyers may re-rank bidders based on net price and availability.

- Shortage normalization: temporary supply constraints can lift prices temporarily and then reverse when supply returns.

- State and PBM preferred product swaps: pharmacy benefit dynamics can shift net pricing quickly even when the molecule is unchanged.

What generic launch scenarios typically change revenues?

- Lowest net price wins: a new bidder undercuts within a major contract lane.

- Switch in package size: tube or unit changes affect pharmacy stocking and may reallocate share.

- Formulary preference shift: ointment-to-cream preference can move volume even if total mupirocin prescriptions remain stable.

How do price, reimbursement, and procurement trends shape mupirocin revenue and margin?

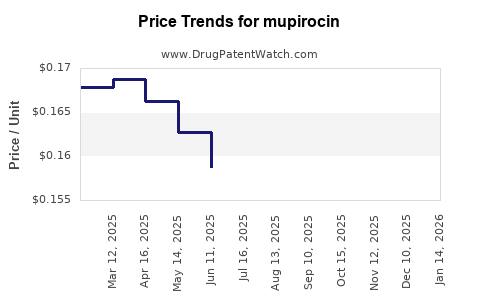

Mupirocin revenue often follows a predictable pattern for commoditized topical antibiotics: modest unit demand growth or stability, offset by declining net price due to generic competition. Margin performance is heavily tied to net realized price after rebates and contracting.

Key commercial levers

- WAC vs net: branded WAC comparisons can mislead; net price after rebates is what determines revenue trajectory.

- Contracting: hospital and ID committee decisions can lock in a preferred product.

- PBM behavior: preferred tiers can shift demand toward the lowest-cost NDCs.

- Supply reliability: availability impacts fill rates and can temporarily distort demand toward available SKUs.

What investors typically see

- Revenue stability, not value growth: volumes can hold, but absolute revenue does not trend strongly upward absent a meaningful access shift.

- Margin compression: persistent price pressure from multiple generics limits profitability.

Which companies are the primary competitors for mupirocin in the US and what is the competitive landscape?

The competitive set for mupirocin is usually dominated by multiple generic manufacturers across major wholesalers and pharmacy distribution channels. The brand-to-generic transition has made the competitive landscape largely procurement-driven.

Typical competitor behavior

- Volume capture through contracting: bidders win preferred status by offering low net pricing and reliable supply.

- SKU expansion: competitors increase presence through multiple package sizes and NDC variants.

- Channel focus: some suppliers prioritize hospital supply, others retail.

Business impact

- Market share is less about differentiation and more about availability plus net pricing across specific formularies and PBM lists.

How does mupirocin compare with other topical antibiotics for commercial momentum?

Mupirocin faces competitive pressure from other topical antibacterials used for skin infections and decolonization-adjacent use cases. Commercially, the key comparison is not efficacy alone but prescribing habits, formulary positions, and patient tolerance for base formulation.

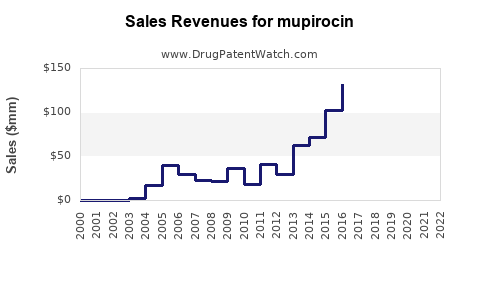

What does the financial trajectory look like across a typical product life cycle for mupirocin?

A “mature commodity” financial trajectory usually has three phases:

- Brand peak or stabilization: pricing holds longer with limited generic competition.

- Generic displacement: revenue declines as multiple ANDA competitors enter.

- Stabilization with net-price erosion: unit volume stabilizes, and revenue tracks pricing over time.

For mupirocin, the market is typically in phase 3 for most relevant product SKUs: revenue is primarily a function of usage persistence and continued access under payer and institutional purchasing.

Revenue drivers that can still move the needle

- Guideline adherence cycles in hospitals and community infection prevention programs.

- MRSA prevalence trends: changes in MRSA burden can influence decolonization protocol intensity.

- Payer policy changes: step therapy and prior authorization are possible for certain topical antibiotics, though generic substitution usually limits payer leverage.

What factors influence mupirocin adoption trends for MRSA decolonization programs?

Decolonization programs are a major commercial engine for mupirocin ointment applied intranasally. Adoption depends on local evidence interpretation, infection-control strategy, and compliance.

Drivers

- Hospital MRSA rates and outbreak history: higher urgency can increase usage.

- Bundle structure: mupirocin effectiveness is often evaluated as part of broader MRSA bundles (screening, environmental cleaning, chlorhexidine where used).

- Operational feasibility: staff compliance and patient throughput matter.

Constraints

- Resistance surveillance: high rates of mupirocin resistance can trigger protocol revisions and reduced use.

- Targeting strategy changes: moving from universal to targeted decolonization reduces total exposure.

What manufacturing and supply-chain risks can affect mupirocin pricing and revenue?

Because mupirocin is generic and widely manufactured, supply issues are less structural than for single-source specialty drugs, but episodic disruptions can still move prices.

Risk factors

- Batch-level quality events: deviations can trigger temporary suspension.

- Capacity reallocation: shared manufacturing lines may be repurposed.

- Regulatory actions: warning letters or import alerts can remove supply from the market quickly.

Commercial effect

- Short-term price spikes can lift revenue even if long-term demand remains flat.

What is the US regulatory status and Orange Book status for mupirocin?

Mupirocin is generally represented on the FDA landscape as an ANDA/generic commodity with multiple listed products, with Orange Book entries typically reflecting the underlying patents (when any remain) plus listed exclusivities. The regulatory status in practice usually means generic availability is broad and continuous across dosage forms.

Practical business read-through

- When products are widely available, exclusivity is not usually a gating factor for new competition; pricing and contracting dominate.

What litigation and settlement dynamics matter for mupirocin?

For a mature topical antibiotic with broad generic coverage, mupirocin litigation is not usually a primary market-shaping event. Where litigation exists, it tends to resolve into generic entry schedules and settlement-driven transitions rather than long-term exclusivity protection.

Market impact paths

- Paragraph IV suits: can accelerate entry if the challenged patent is invalid or not infringed.

- Settlement agreements: can delay or structure generic entry windows on specific NDCs or dosage strengths.

What revenue exposure does a market entrant face if it targets mupirocin?

A new entrant’s revenue potential is constrained by:

- rapid pricing convergence across generics,

- dependence on winning preferred status in PBM and institutional contracts,

- susceptibility to NDC-level competition from existing suppliers.

Where growth can still exist

- New SKUs (package size, alternate dosage form) that win contract preferences.

- Underpenetrated institutional accounts where supply reliability and contract economics can drive switch.

- Geographic/regional distribution strengths that reduce stockouts and enable higher fill rates.

Key Takeaways

- Mupirocin’s financial trajectory is typical of a mature, off-patent topical antibiotic: revenue is driven by stable usage volumes and procurement access, while net price erosion limits growth.

- Competitive dynamics are dominated by generic interchangeability, with major swings linked to PBM preferences, hospital contract re-tenders, and episodic supply disruptions rather than patent expiry.

- MRSA decolonization programs are a key utilization engine, but adoption intensity can shift based on resistance surveillance and targeting strategy.

- Commercial upside for new entrants is mainly execution-driven (availability, contracting, SKU fit), not exclusivity-driven.

FAQs

1) How do mupirocin ointment and cream differ commercially?

They compete on patient preference, tolerability, and formulary selection; ointment often captures more decolonization-adjacent use while cream is used for broader dermatologic presentations.

2) Does mupirocin market growth depend on MRSA prevalence?

Partly. MRSA burden and infection-control intensity influence decolonization protocol volume, but stewardship targeting can counterbalance increases.

3) What drives net pricing for generic mupirocin in the US?

Preferred drug lists, PBM rebates, and hospital contracting determine realized pricing more than WAC.

4) Can mupirocin resistance reduce demand?

Yes. Rising resistance can lead to protocol changes or reduced use, particularly in institutional decolonization workflows.

5) What supply-chain events most affect mupirocin revenue?

Quality-related suspensions, manufacturing disruptions, and import/recall events that temporarily reduce available supply can shift pricing and fill rates quickly.

References (APA)

- FDA Orange Book. (n.d.). Approved Drug Products with Therapeutapeutic Equivalence Evaluations (Orange Book). U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA. (n.d.). Drugs@FDA. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- Centers for Disease Control and Prevention (CDC). (n.d.). Guidance and resources on MRSA prevention and decolonization. https://www.cdc.gov/mrsa/